Goodhart’s law and the fall of Nick Schorsch: The infamous mousepad

The House of Cards that Nick Schorsch built was destined to collapse for a variety of reasons. But what started the demise was then-CFO of ARCP Brian Block just making up some numbers in a spreadsheet. This led to ARCP revealing a $23 million accounting misstatement. After that it became nearly impossible for the non-traded programs to raise new capital, and a whole slew bad behavior and examples of egregious mismanagement soon came to light(I’ve highlighted examples of their questionable corporate governance before). ARCP changed its name to Vereit, but the whole American Realty Capital complex of affiliated entities that depended on new fundraising would never recover.

ARCP’s culture was obsessively focused on achieving financial projections, especially for adjusted funds from operations(AFFO), a preferred Wall Street metric for REITs . According to Investment News:

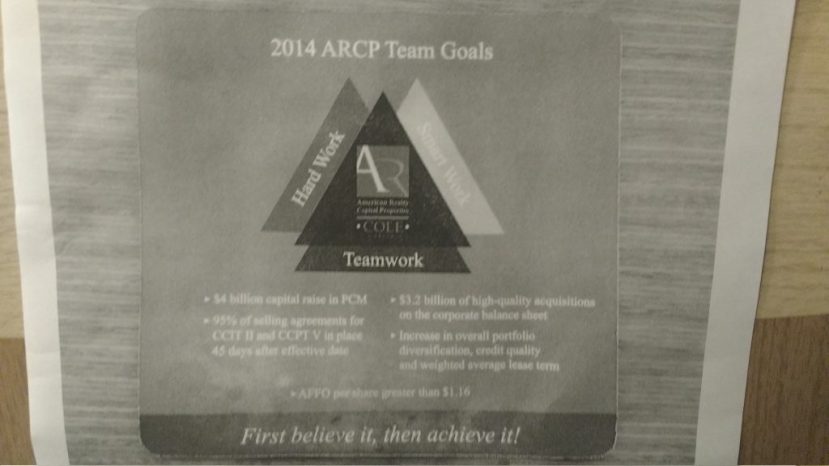

In fact, the company gave employees computer mouse pads with 2014 AFFO guidance on them. “AFFO per share greater than $1.16,” the computer mousepad declared. “First believe it, then achieve it.”

I was able to independently verify the existence of this infamous mousepad. Here is a (deliberately obscured) photo:

This mousepad is a manifestation of “Goodhart’s Law” in action. Named after economist Charles Goodhart, this states that

When a measure becomes a target, it ceases to be reliable.

Goodhart’s law is very similar to “Campbell’s Law” named after social scientist Donald Campbell. Campbell’s law states:

The more any quantitative social indicator is used for social decision-making, the more subject it will be to corruption pressures and the more apt it will be to distort and corrupt the social processes it is intended to monitor.

When people are incentivized to achieve one metric above all else, there behavior will result in the number ceasing to be have its orignal meaning. Goodhart’s law was originally used to describe how monetary policy targets led to distortion. Recent examples of this phenomenon on include reclassification of crimes to reduce crime statistics, and abuse of academic citations. In Capital Returns: Investing Through the Capital Cycle , Edward Chancellor highlighted the Goodhart’s law as the reason conducting investment analysis based exclusively on the single metric of earnings per share growth. The ARCP incident certainly wasn’t the first time that Goodhart’s law led people to fudge the accounting numbers.

Goodhart’s law inevitably leads to waste of resources. One example from the Soviet Union nail factories illustrates this in a big way:

The goal of central planners was to measure performance of the factories, so factory operators were given targets around the number of nails produced. To meet and exceed the targets, factory operators produced millions of tiny, useless nails. When targets were switched to the total weight of nails produced, operators instead produced several enormous, heavy and useless nails.

Beyond just reclassifying or forging numbers, and producing useless nails, incentives distorted by the emphasis of single metrics can have even scarier effects:

During British colonial rule of India, the government began to worry about the number of venomous cobras in Delhi, and so instituted a reward for every dead snake brought to officials. Indian citizens dutifully complied and began breeding venomous snakes to kill and bring to the British. By the time the experiment was over, the snake problem was worse than when it began. The Raj government had gotten exactly what it asked for.

To avoid the trap of Goodhart’s law or Campbell’s law managers (and investment analysts) need to take think deeply about what is measured, and take multiple factors into consideration, never relying too much on any individual metric. Failing to consider Goodhart’s law can be fatal for investments.

One comment