Big dam frontier market bond offerings, low dam yields

Credit markets are crazy, from US buyouts, to frontier market bond offerings.

Buffett released the annual Berkshire letter this past weekend, and it contained a number of gems as usual, although it was shorter than the typical letter.

Petition’s excellent distressed credit focused newsletter last week pointed out that Buffett’s concerns about high M&A prices were:

affirmation of a number of macro themes that ought to portend well for distressed players in a few years: (i) excess capital supply, (ii) resultant inflated asset values, (iii) lack of discipline, and (iv) over-leverage.

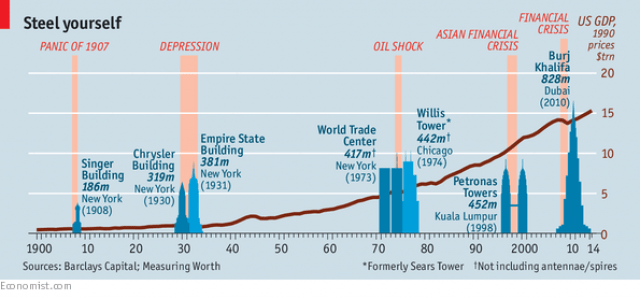

The big dam indicator

The loose credit has spread to frontier market bond offerings as well. Tajikistan, a country with $7 billion in annual GDP in September raised $500 million of debt at 7.125% for 10 years. Tajikistan had no problem raising this capital. In fact funds put in $4 billion in bids for the $500 million in paper. Tajikistan will use this capital used for the Rogun barrage project, which involves building the world’s largest hydroelectic dams. Building large buildings tends to correlate with hubris, and bubbles(although the empirical evidence around causality is loose), as many have noted:

More frontier market fun

Tajikistan’s big dam bond offering is just one example of aggressive lending in emerging and frontier markets. Nigeria raised $2.5 billion Kenya raised $2 billion, and Belaraus 600m. EM borrowers raised over $150 billion in syndicated bond sales in January 2018. This is 15% higher than the previous annual record for January.

One deal banker cited in the article says:

One deal banker cited in the article says:

People will buy anything so long as it offers them yield and diversification. They get bored of only being able to buy the same names, and have also hit their limits for some of the more frequent names.

Credit clearly isn’t the smart money any more.

Some of these frontier markets are undertaking genuine structural reforms: improving political and regulatory stability, etc. However in many cases, the tail is excess liquidity tail is wagging the valuation dog. Bankers are aggressively pushing deals.

From the article:

If the main guy [eg finance minister] doesn’t do much talking and its all being done by the banker and a slightly spivvy investor relations guy, we know what’s going on here. They may give you a whole load of information at the launch, but that could be the last time you hear from them.

If these countries need to refinance a few years later when interest rates are higher, things could get quite messy. This is going to be a fascinating opportunity set when it all blows up.

See also: https://www.reuters.com/article/tajikistan-eurobonds/corrected-investors-explore-risky-frontier-with-tajikistans-debut-bond-idUSL8N1LL38Z