Tagged: Credit Cycle

A Negative Interest Rates Thought Experiment

Toto, I have a feeling we’re not in Kansas anymore

Dorothy in Wizard of Oz

With a negative yielding investment, the price you pay exceeds the sum that you will get back at maturity plus the income you receive in the interim. If you buy a negative yielding bond you are guaranteed to lose money. If the rate you receive on bank deposits is negative, you are guaranteed to lose money.

Negative interest rates are becoming kind of a big deal:

Most negative yielding debt is government debt, which is ironically considered “safe”, at least in first world countries. With government debt, you know what cash flows you will receive during the holding period, and what face value amount of principal you will receive upon maturity. With everything else, cash flow is uncertain and principal is always at risk. Indeed the yield on government debt functions as a proxy for the “risk free rate” , which is a critical input in financial models investors use to make strategic decisions throughout financial markets.

Conservative investors generally prefer to hold a lot of government debt in order to meet future needs. Pensions, banks, and insurance companies are required to hold a minimum percentage of their assets in government debt so they can safely meet obligations to their stakeholders.

Negative interest rates cause a lot of surprising second order impacts throughout the world impacting how people do business.

Options Pricing

The Black Scholes model is one of the pillars of modern finance. It uses the risk free rate as an input but it cannot compute when the risk free rate is negative. It requires users to calculate a logarithm. Yet the logarithm of a negative number is undefined/meaningless. Here is a paper that explored the implications in more detail. Maybe people can use the old Brownian motion models, but there isn’t going to be universal agreement right away on what to use.

Any switchover will create unintended consequences throughout the investment world . Lots of funds hold over the counter options or swaps which must be valued using models in the time between their initiation and expiration or exercise. This valuation impacts the number that appears on the statement of investors. To the extent that investors have asset allocation targets around what percent of the entity’s assets can be invested in what, this will have secondary impacts in other markets. A lot of large firms have to totally change their valuation policies which is never easy to do because valuation departments are plenty busy with their jobs as it is. Markets aren’t going to close just so they can rewrite their valuation policies.

Also, in cases where a swap or OTC option contract requires collateral to be posted as the pricing changes throughout the life of a contract, both sides of the contract need to agree on valuation methods. When interest rates are positive, Black Scholes is a noncontroversial options I doubt contractual language was written in a way that accommodate for a world where Black Scholes would completely stop working.

Currently, more banks are trading a wide number of options without a reliable price. Each bank could handle this problem by performing its own solution, but the lack of a shared approach could lead to serious legal issues.

Source

This stuff is all theoretical but it has real cash impact throughout the world. What types of risks can be hedged will impact how capital can be allocated. How capital is allocated directly impacts what ideas get funded.

Now lets consider the real world impact on different groups of investors.

Stimulating TINA

In theory, negative rates should stimulate the economy. If investors only invest in safe assets, nothing else will get funded. Retirees need income from investments to live, foundations need to earn enough to safely withdraw funds, etc etc. If the bank charges them to hold their cash, they will invest more in real estate, high yield debt, and venture capital etc. They will have to take no more risk because “there is no alternative”(TINA).

However, when you look at how negative rates will impact pensions, banks and insurance companies, its hard to escape the conclusion that they might have a destructive, rather than stimulative impact on financial markets.

Pensions

People live longer than they can work. To prevent a social catastrophe, countries have different ways of providing for old people. Pensions are a big part of the financial markets According to CFA society: Willis Towers Watson’s 2017 Global Pension Assets Study covers 22 major pension markets, which total USD 36.4 trillion in pension assets and account for 62.0% of the GDP of these economies.

In the US people pay into Social Security, which provides a bare minimum standard of living to old people. The Social Security Fund is only allowed to invest in US Treasury Securities. If Treasuries yielded negative, the Social Security Fund will erode over time, meaning it won’t be able to meet its bare minimum obligations to retirees.

Social Security by itself barely provides enough to live on. A lot of people in the US and around the world also have pensions through their jobs as well. The impacts of negative rates get more nuanced and even weirder when you consider how these work.

First of all, extremely low interest rates worsen pension deficits. Future obligations must be discounted backwards. Lower discount rate leads to higher obligations in the present day. On the other side of their balance sheet, they must make an actuarial assumption about future returns on their investments. From what I’ve seen they often make aggressive return assumptions. To try to justify higher return assumptions, they put what they can into riskier investments. To this extent pension funds are partially in the TINA Crowd.

Pensions are generally also obligated to put a certain amount of assets into “safe assets” which are the first thing to start yielding a negative rate. As a result, this negative rate will create a destructive feedback loop.

Gavekal had this story of a Dutch Pension as an example:

One day he was called by a pension regulator at the central bank and reminded of a rule that says funds should not hold too much cash because it’s risky; they should instead buy more long-dated bonds. His retort was that most eurozone long bonds had negative yields and so he was sure to lose money. “It doesn’t matter,” came the regulator’s reply: “A rule is a rule, and you must apply it.”

Thus, to “reduce” risk the manager had to buy assets that were 100% sure to lose the pensioners money.

Pension funds get caught in a feedback loop that will erode their capital base. For example say they buy a 5 year zero coupon bond at €103:

The €3 loss will reduce the market value of assets by €3. Holland also has a rule that pension funds must buy more government bonds the closer they get to being underfunded. Yet buying such negative-yielding bonds and keeping them to maturity ensures losses, making it more likely the fund will be underfunded, and so forced to buy more loss-making bonds (spot the feedback loop). Soon the fund will be distributing returns from capital, rather than returns on capital. Hence,it is not inflation that will destroy pension funds, but the mix of negative rates and rules that stop managers from deploying capital as they see fit. These protect governments, not pensioners who are forced to buy bad paper.

So negative rates will exacerbate the global retirement crisis. Oops.

Banks

What about banks? Negative rates also destroy their capital base, and leave them with less money to actually lend out in the economy. This hits at the heart of how fractional reserve banking works.

According to Jim Bianco at Bloomberg:

For every dollar that goes into a bank, some set amount (usually about 10%) must go into a reserve account to be overseen by the central bank. The rest is either lent out or used to buy securities.

In other words, the fractional reserve banking system is leveraged to interest rates. This works when rates are positive. Loans are made and securities bought because they will generate income for the bank. In a negative rate environment, the bank must pay to hold loans and securities. In other words, banks would be punished for providing credit, which is the lifeblood of an economy.

Gavekal explains how this leads to an eroding capital base (using the same 5 year zero coupon bond as the pension example above):

As a leveraged player, let’s assume it lends a fairly standard 12 times its capital. This capital has to be invested in “riskless” assets that are always liquid. In the old days, this would have been gold or central bank paper exchangeable into gold. Today, the government bond market plays the role of “riskless” (you have to laugh) asset, which has no reserve requirement. As a result, banks are loaded up with bonds issued by the local state. Now let us assume that a bank has just lost €3 on the zerocoupon bond mentioned above. The bank’s capital base will be reduced by €3. Based on the 12x banking multiplier, the bank will have to reduce its loans by a whopping €36 to keep its leverage ratio at 12. Hence, the effect of managing negative rates while also respecting bank capital adequacy rules means that the capital base can only shrink.

Insurance Companies

One of the main ways that insurance companies make money is by collecting premiums in advance of paying out any claims. Hey are able to invest these premiums, collecting a float premium. Of course they are limited in how much risk they can take with the money they are holding to pay out any possible claims. Regulators generally require them to put a certain amount in a “risk free “ asset like government debt, and the rest in riskier assets. If government debt is negative yielding, we again get to a destructive feedback loop that has major second order impacts.

From the Gavekal note:

The insurance company could raise its premium by the amount of the expected loss from holding the bond (not very commercial), or it could just underwrite less business. Either way, it will have less money to invest in equities and real estate. Simply put, either the insurance company’s clients will pay the negative rates, or the company itself will do so by increasing its risks without raising returns. This means that either the client pays more for insurance, and so becomes less profitable, or the insurance company takes a hit to its bottom line.

People will have to pay more premiums for less insurance coverage.

Long term, negative rates will exacerbate the retirement crisis and basically destroy the business models of banks and insurance companies as we know them. This doesn’t automatically mean negative interest rates can’t persist. Perhaps there are other ways to provide for old people (ie higher taxes on a shrinking economy?) Banks and insurance companies can find other ways to make money. Regulators might respond, by changing rules or creating various incentive programs.

In this post I only covered only a few of the second order impacts of negative interest rates. Negative interest rates make the capital asset pricing model give nonsensical infinite results. I think CAPM is mostly bullshit anyways, but enough people use it that it has a reflexive impact on asset pricing. Unwinding it won’t be easy. I didn’t even touch on how negative rates can screw up the plumbing of financial markets: repo markets, securities settlement , escrow etc. Not enough people have really thought this all through. Many of the assumptions that have historically driven investor behavior will no longer hold if negative rates persist.

Maybe interest rates will normalize again. It will wipe out a few of the most overleveraged players, but the financial system will recover quickly. On the other hand, if negative rate do persist, get ready for a slew of unintended consequences in places you didn’t expect.

See also:

Mysterious by Howard Marks at Oaktree

Cheap stuff and cheap capital

Two main factors drive an upsurge in entrepreneurship: cheap stuff and cheap capital. Cheap stuff is primarily a long run secular trend. Cheap capital is cyclical.

By cheap stuff I mean the inputs to a business, mainly technology. This has gone consistently down over time. One can build a website or an app for a few thousand dollars that is better than what they could have done for millions of dollars a decade ago.

Even if capital becomes scarce, cheap stuff will still be a positive factor driving entrepreneurship.

By cheap capital I mean the flood of venture capital. This is primarily cyclical. Consider this quote:

“There’s so much money chasing these deals that venture capitalists are in competition with each other. They spend their energies marketing themselves instead of screening the deals. It’s gotten silly”

Think it applies today? Or maybe to the late 1990s tech boom? This quote is from the WSJ in 1981, and referenced in this excellent article about 1980s venture capital.

During a boom its easy for most ideas to raise capital, regardless of business viability(as long as they fit with theme of the times). Indeed they can keep raising rounds in hopes of a profit decades in the future. After a bust its hard to raise capital, even for a great idea. Entrepreneurs need to bootstrap and get revenue a soon as possible.

Right now it seems there is a ton of venture capital financing companies that are losing money.

Cheap stuff and cheap capital are partly entangled. You might be reading this from within a WeWork. If they couldn’t keep raising cheap capital you think your rent is going to stay the same? Or maybe you are building a business on top of a money losing social media platform, or somehow benefiting from a thriving open source ecosystem. On the other hand, its harder to source talent when there is a flood of capital, and certain commodity based goods can have their own production cycle. Yet you can run your business from a garage and the new inventions of the latest venture boom aren’t going away.

Which is most important- cheap stuff or cheap capital ? I don’t know, but we’ll get to find out when this cycle turns. Creative entrepreneurs will still take advantage of technological improvements to bootstrap groundbreaking ideas, even if they can’t raise venture capital. Sometimes they do it out of choice, other times they do it out of necessity.

Once this cycle turns, we’ll go through a few years where most new businesses have no choice but to bootstrap.

This idea generally applies across all industries, not just venture funded. However in commodity based industries the cyclicality functions differently. Cheap capital often leads to inflation in hard assets. See also: Capital Returns: Investing Through the Capital Cycle

Thinking and Applying Minsky

Hyman Minsky developed a framework for understanding how debt impacts the behavior of the financial system, causing periods of stability to alternate with periods of instability. Stability inevitably leads to instability. Minsky identified three types of financing: Hedge financing, speculative financing, and ponzi financing. It seems some people only remember Minsky every so often when there is a financial crisis, but the framework is useful in all seasons.

Hedge Financing

An asset generates enough cash flow to fulfill all contractual payment obligations. For example, a conservatively leveraged rental property that generates enough rent to pay down the entire mortgage over time, regardless of the change in quoted property prices. Or a company that issues some bonds, then pays them back using cash flow from the business Generally hedge financing units have a lot of equity down. Even a market crash, will not cause an investor to suffer permanent capital impairment if they only use hedge financing. The equity holder who uses hedge financing will never depend on the capital markets.

Speculative Financing

An asset generates enough cash flow to fulfill all debt payments, but not the full principal amount. In this case debt must be rolled over, or the asset must be sold, in order to pay back the full amount. For example, a rental property financed with some sort of balloon payment structure that generates enough cash flow to pay off mortgage payments up until the balloon payment at the end. When the balloon payment comes due, the investor must roll over the debt or sell the asset. An investor ttat uses speculative financing is dependent on capital markets. If there is a delay or a problem in refinancing, they could lose their investment.

Ponzi Financing

This is basically “greater fool” investing. Ponzi financing means there is so much leverage n an asset, that the investment must be refinanced, or sold at a higher price quickly, otherwise the entire investment is lost. Sometimes property purchases will be financed with shorter term bridge loan. If the bridge loan can’t be refinanced with longer term mortgage, the investor is out of luck. Towards the end of the market cycle, many companies will be issuing bank loans or bonds that can only be repaid by refinancing. If their unable to refinance, they go bankrupt.

Use of ponzi financing means the investor is highly dependent on capital markets. The slightest disruption in capital markets or change in interest rates/inflation results in a large capital loss.

Junk bonds are not inherently bad. A higher interest rate can in many cases compensate for greater risk, especially across a portfolio of non correlated investments. Howeve, duringthe junk bond era, many companies

Similarly securitization is not inherently bad. It can allow capital to flow more effeiciently. But often banks would end up aggressively securitizing, with the need to sell the loans they made quickly. But if they weren’t able to resell they couldn’t hold the loans. This happened to Nomura during the Asian financial crisis, as vividly told in this Ethan Penner interview.

Ponzi in this case is not illegal activity, just extremely risky. Of course those investors who finance their activities ponzi style often end up feeling the need to commit illegal acts. The Minsky Kindleberger model is useful here.

The cycle repeats

During a recession is very difficult to get any debt financing that is not “hedge financing”. Lenders are scarred from the last cycle, and there is a paucity of available risk capital. But a price rise, and investors get more comfortable, more and more financing becomes ponzi units In fact. Lenders may lower their standards and become more accepting of ponzi units.

Throughout the market cycle, more and more financing is ponzi units. Eventually there is no greater fool to sell to. When many ponzi units are forced to sell at once, it eventually leads to a collapse in values. This is how stability inevitably leads to stability. The cycle repeats.

How to apply this?

To protect my capital, I look try to mainly expose myself to hedge financing, with a small amount of speculative financing. I position my portfolio so that I don’t need to refinance anything or sell anything in a rush. When I invest in leveraged companies with speculative or ponzi financing, I make it small position(always in some sort of limited liability structure), and generally won’t average down much if at all. Additionally, when I notice an increase in ponzi financing in the markets, I become more cautious.

Leverage, like liquor , must be consumed carefully if at all.

See also:

Beyond headline numbers

Everybody has access to Bloomberg and Google. Every global macro investor closely follows macro data out of every country. To gain an an edge, one must look beyond headline numbers, and find underutilized datasets.

This applies when finding countries, industries, and individual companies in which to invest. Any time you want to combine top down and bottom up insights, you need to get creative with finding the right data.

Schumpeter and Perez

Joseph Schumpeter pointed out that aggregate figures “conceal more than they reveal”.

Relations between aggregates are

“entirely inadequate to teach us anything about the nature of the processes which shape their variations, aggregative theories of the business cycle must be inadequate too…”

In Technological Revolutions and Financial Capital, ( Carlota Perez emphasizes that new technological paradigms can only be analyzed by looking closely at inner workings of an economy. Within the same country, or industry some subsectors will grow at astonishingly high rates, while others decline. Perez’s framework is valuable to analyzing times of great technological change, which is basically anytime. Examples she uses include the first British Industrial Revolution( the age of Steam and Railways, the Age of steel, electricity, and heavy engineering, age of oil, automobile and mass production.

Top line numbers such as GDP or earnings could deceive an analyst, especially when looking at a new market.

Valuation and pricing

“People living through the period of paradigm transition experience real uncertainty as to the ‘right’ price of things(including that of stocks, of course).”

Extreme jumps in productivity change relative price structures in the economy. “The change in relative price structure is radical and centrifugal. Money buying electronics and telecommunications today does not have the same value as money buying furniture or automobiles.” Therefore, looking at inflation or deflation in aggregate is deceptive. Many years after Perez’ book, this now exacerbated by the Amazon effect. To some effect this may impact valuation in some industries.

Research methods

Long term aggregate data, spanning multiple periods of technological change are senseless. This goes for GDP, corporate earnings etc. Yet disaggregated stats are rarely available(except during more stable phases), as Perez points out.

The internet has provided more opportunities to find disaggregated, unique, underutilized datasets. Often this means poking around on weird regulatory websites, and following up on footnotes to academic papers.

This process might be about to get a lot easier.

Google launched a new dataset search engine. I’m excited to see how its impact snowballs as more datasets are added. Although intended for journalists, it is likely to be a valuable tool for investors seeking differentiated alpha.

Of course that means today’s edge, will be tomorrow’s table stakes.

See also: The hard thing about finding easy things

History Repeats: The Serpent on the Rock

“History Repeats. The first time as a tragedy, the second time as a farce.”

– Karl Marx(1)

There are amusing parallels between the rise and fall of the real estate private partnership market in the 1980s, the pre financial crisis tenant in common(TIC) syndication market, and the post financial crisis non-traded REIT market driven by Nick Schorsch and his AR Global empire.

Each episode involved high fee investment products designed to fulfill investor desires for yield, tax efficiency and perceived stability, while creating disproportionate benefits for intermediaries. Each episode ended badly. And the cycle repeats, again and again.

First of all, the charts tell parallel stories:

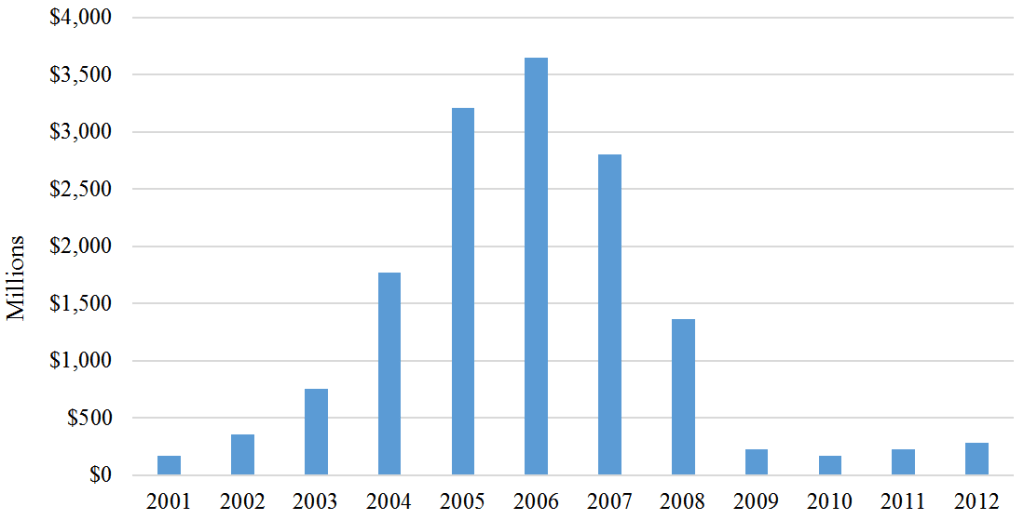

Real Estate Limited Partnerships 1970-1991

TIC Equity raised 2001-2012:

Source: Securities Litigation and Consulting Group

Non-traded REIT Equity Raise 2000-2016:

Source: Stanger Report, author’s calculations based on SEC filings.

Note that the 2015-2016 dropoff would be much sharper if you excluded Blackstone’s REIT, which entered the wirehouse channel in late 2016, and accounted for 50% of total annual NT REIT sales within a few months. Sales to the independent broker dealer(IBD) channel, which Blackstone largely bypasses, were completely decimated, and the dropoff has accelerated in 2017. (2)

May Day

High fee products are sold, not bought. The commissions on illiquid real estate products have always been higher than other investments available to retail investors.

In Serpent on the Rock Eichenwald traces the original real estate partnership craze back to the May 1, 1975 abandonment of fixed commissions on sale of stocks and bonds. Yes it is viciously ironic that commissions were fixed before 1975. The financial services industry was apparently afraid of capitalist competition and all the wonderful creative destruction it brings. Once they lost large commissions on simple security trades, they went looking through more complex higher fee product.

After May Day:

No longer could brokerage firms subsidize their bloated through fat commissions on securities trades. Firms unable to adjust collapsed by the dozens. The industry had to either dramatically cut back expenses or find new products with higher commissions that could be pumped through the sales force. Suddenly tax shelters, which sold for higher commissions than stocks and bonds didn’t look so unappealing.

The impact of May Day has continued to drive down commissions decades later. This makes sense. After all, transactional costs should approach zero over the long run, because with computers the marginal cost of doing a trade in all but the most illiquid complex markets is effectively zero. Significant scale and technological investment is necessary to run a brokerage business focused on liquid markets.

Consequently, the current IBD ecosystem is highly dependent on non-traded REITs and other high fee direct private placement programs. This is complicated by the fact that IBDs payout a high proportion of commissions to the financial advisers(like 90% in many cases). Many financial advisers built their business on 1031 exchanges, non-traded REITs or other private placements. TICs typically charged 20-30% commissions. Commissions eat up a large portion of offering proceeds for non-traded REITs. Additionally, non-traded REIT sponsors pay out a due diligence kickback to broker dealer home offices. Many smaller IBDs depend on these kickbacks for survival.

Of course, the commissions were much more egregious the first time around. Old timers fondly remember 20%+ loads on product. up front sales loads have now declined to high single digits and low double digits. Inland has driven down commissions on 1031 exchange product. Plus state securities regulators put out NASAA guidelines to limit loads on registered products. Nonetheless in an age where interactive Brokers charges $1 per side on a trade regardless of size, and few modern brokerages charge more than $7 per trade, even high single digit sales loads on non-traded retail product are absurd.

In Backstage Wall Street Josh Brown outlines his “Iron law of product compensation”:

The higher the commission or selling concession a broker is paid to sell a product, the worse that product will be for his or her clients.

This was the thread that connects the 1980s private partnership craze, with the pre financial crisis TIC explosion and the post financial crisis non-traded REIT market.

Yield Pig Exploitation and the Illusion of Safety

Just like private partnerships in the 1970s and 1980s, brokers sold TICs and Non-traded REITs to unsophisticated yield hungry retirees as safe, stable investments.

Here is one description of the private partnership market:

Many of the public offerings were promoted as a way for the small investor to participate in real estate, widely believed to be an inflation hedge, offering greater return and moderate risk as compared to stocks. The ability for an individual of modest net worth or income to invest in securitized real estate was viewed as a real benefit of public syndications.

The limited partners were sold their investments on the assumption that real estate was a safe, growing investment. Often these investors were unsophisticated in investment matters, and were more often swayed by aggressive brokerage salesmanship. The importance of liquidity became apparent to the investors only after substantial investment had already occurred. Liquidity was never promised for limited partnership securities and the partnership structure itself was designed to constrain liquidity.

In Serpent on the Rock Eichenwald meticulously tracked the juxtaposition between sales materials promising safety and the ultimate collapse in values.Non-traded REITs and TICs are also sold as safe investments that do not have the volatility of the stock market. Of course the stability is an illusion, and investors are still highly dependent on the real estate performance.

Due diligence

Eichenwald describes due diligence at Prudentialduring the peak of the private partnership craze:

The due diligence team was not just overwhelmed from the number new deals they had to approve- they also had to keep tabs on the old deals that had already been sold. Darr had negotiated for Bache to be paid a monitoring fee from some tax shelters it sold in exchange for reviewing their financial performance. Supposedly, this was designed to make sure that the general partners managing the deals did things right and took care of their investors. It was a key selling point for Bache brokers: In sales pitches, they painted a picture of top Bache financiers in green eyeshades peering over the shoulders of the General partners, watching everything that was done, The image of financial professionals crunching numbers late into the night to make sure investors were protected was a persuasive marketing tool.

But asset monitoring paid only a small fraction of the fees that Bache received from selling new deals. So the job of keeping an eye on the performance of old shelters quickly became viewed as simply a headache. It was an obligation that slowed down the whole process of churning out deals., without enough juice from fees to make up for the effort. The monitoring assignment became a hot potato, passed from executive to subordinates, and from then on down the line.

Many similar scenes in the book are shockingly familiar to anyone who has worked in the alternative investments space.

In subsequent years, third party due diligence firms serving broker dealers helped drive improvements in deal quality, but there are still many serious gaps. Since IBDs depend on the revenue from commissions and due diligence kickbacks, they are under pressure to find product to approve. This bias leads to cognitive dissonance. As non fiduciary middlemen, they often sell things that they wouldn’t invest in themselves, especially with a full sales load.

In the wake of the bankruptcy of TIC Sponsor DBSI, and the collapse of several tax driven energy deals, Reuters investigated due diligence in the independent broker dealer space. It highlighted a too cozy relationship between sponsors and third party due diligence firms.

Perhaps of even greater concern is the disconnect between due diligence process and the needs of end investors.

Potentially alarming findings are often obscured in multiple pages of recondite language, with no definitive conclusions. “They’re these long-winded things that bury things that might be important inside boilerplate disclosures,” said Jennifer Johnson, a professor at Lewis & Clark Law School in Portland, Oregon, who has written extensively about the private-placement business.

Due diligence firms say their reports aren’t designed to be read or understood by investors. Rather, they are meant to help brokers decide whether to recommend private placements to their customers.

Same Same, But Different

Although the distorted incentives,exploitation of unsophisticated yield pigs,were almost identical in each of the three historical examples in this post, there are several key differences. Broker dealers primarily sold private partnerships in the 1980s as a way of reducing taxes. An investor can use a TIC structure as part of a 1031 exchange to delay taxes when selling a property. REITS are a unique IRS creation but the reason for investing in a REIT is mainly income(Excluding situations where someone exchanges via an UPREIT transaction)

The private partnership market collapsed because the tax reform act of 1986 destroyed their entire structure, and basically collapsed the national real estate market. (see: this FDIC report )

The TIC market collapsed when the financial crisis hit the entire real estate market, exposing the problematic underwriting of the TIC Sponsors. However, regulatory issues weren’t the main driver of the collapse. Like the private partnership craze in the 1980s, the modern Non-traded REIT market also collapsed due to regulatory change although the . Finra 15-02, which increased the transparency on client statements, made it harder for advisors to get away with charging the massive sales loads. The fiduciary standard required broker-dealers to act in the best interest of clients, also led many broker-dealers to suspend or slow down the sales of high commission products.

The farce of AR Global’s collapse

Although private partnerships and TIC sponsors generally overpaid for properties they purchased, the collapse of their structures happened during a time of across the board real estate declines in the US

In contrast, investors in post financial crisis vintage non-traded REITs have suffered, in spite of a buoyant real estate market. ARC Hospitality(Now Hospitality Investors Trust) offered shares at $25.00 a share from 2013-2015, and a client statement never would have shown a value below $22.00 until this summer. It revalued at $13.20. A PE fund recently offered $5.53 for the shares. Likewise ARC Healthcare Trust III sold shares $25.00, and recently marked its value down to $17.64, and is now subject to an affiliated transaction with no liquidity event in site.

Private partnerships and TICs were tragedies, AR Global was a farce.

To be continued….

(1) This is from The Eighteenth Brumaire of Louis Napolean.

The full translated quote is :Hegel remarks somewhere that all great world-historic facts and personages appear, so to speak, twice. He forgot to add: the first time as tragedy, the second time as farce.

(2) Wirehouses generally did not sell non-traded REITs until Blackstone entered the market in 2016 Anyone who carefully read The Serpent on the Rock will note how incredibly ironic it is that wirehouses have started to sell non-traded real estate securities again. More on his in a future post.

Big dam frontier market bond offerings, low dam yields

Credit markets are crazy, from US buyouts, to frontier market bond offerings.

Buffett released the annual Berkshire letter this past weekend, and it contained a number of gems as usual, although it was shorter than the typical letter.

Petition’s excellent distressed credit focused newsletter last week pointed out that Buffett’s concerns about high M&A prices were:

affirmation of a number of macro themes that ought to portend well for distressed players in a few years: (i) excess capital supply, (ii) resultant inflated asset values, (iii) lack of discipline, and (iv) over-leverage.

The big dam indicator

The loose credit has spread to frontier market bond offerings as well. Tajikistan, a country with $7 billion in annual GDP in September raised $500 million of debt at 7.125% for 10 years. Tajikistan had no problem raising this capital. In fact funds put in $4 billion in bids for the $500 million in paper. Tajikistan will use this capital used for the Rogun barrage project, which involves building the world’s largest hydroelectic dams. Building large buildings tends to correlate with hubris, and bubbles(although the empirical evidence around causality is loose), as many have noted:

More frontier market fun

FOMO is a hell of a drug

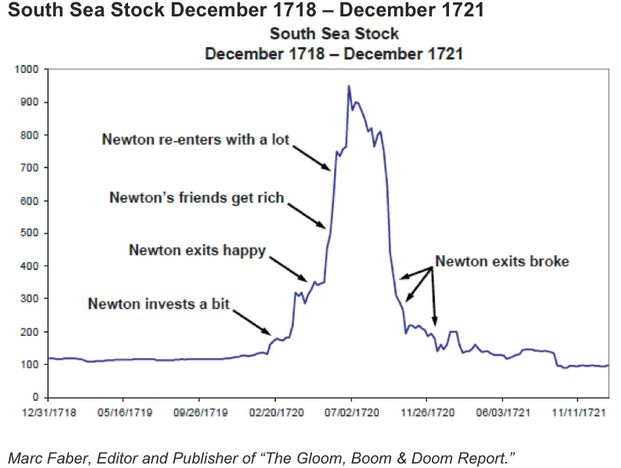

The most dangerous feeling in finance is “fear of missing out”(FOMO). FOMO causes people to make hasty emotional decisions, generally near to the top of a speculative mania. FOMO is the force behind ponzi schemes, stock promotions, and simple legit bubbles. The Stanford Business School has even looked into this

The danger of FOMO impacts people regardless of socieoeconomic status or education. It even impacted Isaac Newton:

Source: the Vantage, (which has some excellent personal finance tips on avoiding the dangers of FOMO)

Last week things got a bit volatile. Markets corrected all the way to… (wait for it) the price level of a couple months ago. This was the result of a sudden sharp reversal of record retail inflows. Although it wasn’t really an abnormal reversal, the media made it sounded like the beginning of another financial crisis.

Warren Buffett, Aesop’s Fables, and the Dot-Com Bubble

I recently went back and re-read the Berkshire Hathaway letters from during the dot-com bubble. Buffett and Charlie Munger mostly sat out the mania, then used Aesop’s Fables to explain it all when it was done. Investors can learn from their ability to maintain equanimity amidst the madness of crowds. However its also important to note that they made errors of omission as technology altered industries. Investors do themselves a disservice if they automatically reject tech investments, just because those are not areas that Berkshire Hathaway invested. Buffett’s letters to investors are a pretty good vantage point from which to understand repeating historical patterns.

1997: Maintain discipline in the mania

As the dotcom bubble started gathering momentum, Warren Buffett reaffirmed commitment to discipline:

Though we are delighted with what we own, we are not pleased with our prospects for committing incoming funds. Prices are high for both businesses and stocks. That does not mean that the prices of either will fall — we have absolutely no view on that matter — but it does mean that we get relatively little in prospective earnings when we commit fresh money.

Under these circumstances, we try to exert a Ted Williams kind of discipline. In his book The Science of Hitting, Ted explains that he carved the strike zone into 77 cells, each the size of a baseball. Swinging only at balls in his “best” cell, he knew, would allow him to bat .400; reaching for balls in his “worst” spot, the low outside corner of the strike zone, would reduce him to .230. In other words, waiting for the fat pitch would mean a trip to the Hall of Fame; swinging indiscriminately would mean a ticket to the minors.

If they are in the strike zone at all, the business “pitches” we now see are just catching the lower outside corner. If we swing, we will be locked into low returns. But if we let all of today’s balls go by, there can be no assurance that the next ones we see will be more to our liking. Perhaps the attractive prices of the past were the aberrations, not the full prices of today. Unlike Ted, we can’t be called out if we resist three pitches that are barely in the strike zone; nevertheless, just standing there, day after day, with my bat on my shoulder is not my idea of fun.

Although way too early, he started lamenting high prices:

In the summer of 1979, when equities looked cheap to me, I wrote a Forbes article entitled “You pay a very high price in the stock market for a cheery consensus.” At that time skepticism and disappointment prevailed, and my point was that investors should be glad of the fact, since pessimism drives down prices to truly attractive levels. Now, however, we have a very cheery consensus. That does not necessarily mean this is the wrong time to buy stocks: Corporate America is now earning far more money than it was just a few years ago, and in the presence of lower interest rates, every dollar of earnings becomes more valuable. Today’s price levels, though, have materially eroded the “margin of safety” that Ben Graham identified as the cornerstone of intelligent investing.

Notable Actions in 1997:

Net sales of 5% of the stock portfolio

increasing emphasis on “unconventional commitments”, including oil derivatives, and direct investments in silver.

1998: Trimming positions too early

Is credit really the smart money?

Conventional wisdom holds that credit markets are “smart institutional money” that sees problems faster than equity markets that are full of less sophisticated retail investors. I question whether that is still empirically true. Retail investors now own large portions of the credit market, including high yield. Credit markets appear to be distorted by a combination of indexation and a reach for yield. Its possible that bonds trading at par can be a false comfort signal for an equity investor looking at a highly leveraged company, because in many recent cases equity markets have been faster to react to bad news.

Retail ownership of credit markets.

However you slice and dice the data, there is clearly a lot more retail money in credit than there was a decade ago. The media mostly reports on noisy weekly or monthly flows, even though there has been a clear long term change.

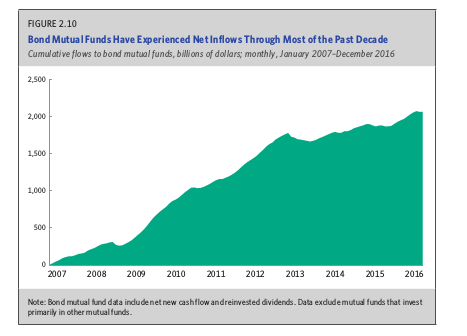

Bond funds in general have experienced dramatic inflows over the past decade:

Source: ICI Fact Book 2017

The issues becomes more serious when you look just at the high yield part of the market. Boaz Weinstein of Saba Capital estimated that between ½ or ⅓ of junk bonds are owned by retail investors in the current market. The WSJ cited Lipper data that says mutual fund ownership of high yield bonds/loans is $97 billion today vs $18 billion a decade ago. ICI slices the data differently, and comes up with a much nosier data set for just floating rate unds, indicating large outflows in 2014 and 2015. However it shows net assets in high yield bond funds up 3x compared to 2007, and the total number of funds up over 2x during that time.

Source: ICI Fact Book 2017

Its not just mutual funds either- there are now more closed end type fund structures that market towards retail investors. BDCs experienced a fundraising renaissance through 2014, and are now active in all parts of the high yield credit markets- from large syndicated loans to lower middle market. Closely related, before the last financial crisis, ago there was minimal retail ownership of CLO equity tranches, but now there are a few specialist funds, and a lot of BDCs have big chunks of it as well. Oxford Lane and Eagle Point were sort of pioneers in marketing CLO investments to retail investors but many others have followed. Interval funds are a tiny niche, but over half the funds in registration are focused on credit. It seems just about every asset manager is cooking up a direct lending strategy. The illiquid parts of the credit market are harder to quantify, but there has been a clear uptick in retail investor exposure since before the financial crisis. The marginal buyer impacting pricing is increasingly likely to be a retail investor rather than an institution.

Retail investors to exhibit more extreme herding behavior. According to Ellington Management Group:

This feedback loop between asset returns and asset flows has magnified the growth of the high yield bubble.

Capital Distortions

Its pretty easy to make a loan, its much harder to get paid back.

Minsky and the Junk Bond Era

King of Capital: The Remarkable Rise, Fall, and Rise Again of Steve Schwarzman and Blackstone discusses the early days of the leveraged buyouts(LBOs) and junk bonds from the vantage point of Blackstone’s founders.

In 1978, KKR did an LBO of an industrial pumps make (Houdaille Industries). There had been many small LBOS of private businesses, but no one had gone that big, done a public company. A young investment banker named Steve Schwartzman heard about the deal and realized he had to get his hands on that prospectus. “He sensed something new was afoot — a way to make fantastic profits and a new outlet for his talents, a new calling.

“I read that prospectus, looked at the capital structure, and realized the returns that could be achieved.” he recalled years later. “I said to myself, ‘This is a gold mine.’ It was like a Rosetta stone for how to do leveraged buyouts. “

Speculative Bridge Financing

It quickly became apparent how lucrative leveraged buyouts could be.

LBOs were financed with Junk Bonds. The process of issuing junk bonds was messy and cumbersome. It took most banks an extremely long time to issue bonds. Drexel was so adept at hawking junks, that companies and other banks in a deal would go forward on an LBO based solely on Drexel’s assurance that it was “highly confident” it could issue bonds. Other banks that couldn’t do that would offer short term financing, aka bridge loans, so a buyer could close a deal quickly, and then issue bonds later to repay bridge loans This alowed DLK, Merril Lynch, and First Boston to compete with Drexel in the LBO financing space.

But what if the bonds couldn’t issued? How would the bridge loan be paid for?

… bridge lending was risky for banks because they could end up stuck with inventories of large and wobbly loans if the market changed direction or the company stumbled between the time the deal was signed up and the marketing of the bonds. The peril was magnified because bridge loans bre high, junk bond-like interest rates, which ratcheted up to punishing levels if borrowers failed to retire the loans on schedule. The ratchets were meant to prod bridge borrowers to refinance quickly with junk, and up until the fall of 1989, every bridge loan issued by a major investment bank had been paid. But the ratchets began to work against the banks when the credit markets turned that fall. The rates shot so high that the borrowers couldn’t afford them, an the banks found themselves stuck with loans that were headed towards default.

In the late 80s/early 90s. several junk bond deals fell through with disastrous consequences. The $6.8 billion United airlines buyout turned out poorly. Several stores ended up going bankrupt due to a failed junk bond deal: Federated Department stores , the parent of Bloomingdale’s, Abraham & Strauss, Filene’s and Lazarus, etc. etc. First Boston nearly failed due to its exposure to junk bond deals. Blackstone mostly sidestepped the worst problems of the era, but fought hard to get refinancing in some cases, and had a couple deals jeopardized.

The Minsky view of junk bonds and LBOs

The collapse of the bridge financing market in the junk bond era illustrates a key idea in Hyman Minsky’s Financial Instability Hypothesis: the idea of three types of leverage.