Tagged: Hedge Funds

Global macro is dead, long live global micro

After Louis Bacon closed Moore Capital this past week, both the FT and the Economist had interesting articles on the future of global macro investing. They struck almost opposite tones, each making good points about the current and future reality. Global macro will return, but likely in an unexpected form.

Stability destabilises a generation of macro hedge fund stars

A league of their own: Do not write off the macro hedge-fund manager just yet

Stability killed the macro star

The glory days of global macro as we know it started when the Bretton Woods system collapsed in 1971, ending fixed exchange rates. Broadly speaking, there were two different groups of investors who entered this environment and profited immensely. The first was people with long/short equity experience in global markets and included George Soros, Jim Rogers, and Michael Steinhardt. The second group included people with a physical commodities and futures background. The Commodities Corporation trading firm trained and/or funded many macro investors including Bruce Kovner, Paul Tudo Jones, Louis Bacon, Michael Marcus, etc.

The dramatic changes in the institutional architecture of international trade and finance created a volatile playground for these investors. Exchanges developed new derivatives instruments for trading newly volatile currencies and increasingly global commodities markets in a high inflation environment. Global trade started to open up dramatically, and global supply chains spidered out in response to changes in policy and technology. Many investors made or lost fortunes betting on big equity moves like the 1987 stock market crash(shortly after Greenspan became head of the Fed), or the breaking of fixed currency regimes such as the sterling crisis of 1992, the Asia crisis of 1997, Russia in 1998, etc. There was also the emerging market debt crisis in the 1980s and the surprise interest rate hike in 1994.

After the 2009 global financial crisis, interest rates and inflation have been abnormally low. The euro crisis notwithstanding, markets have lacked volatility. With no volatility its hard for the traditional global macro style to work. Moore and his proteges have all closed down recently. The decline of the legacy macro investors is just one part of the broader decline of active management. Its been a long torturous capitulation.

Yet stability leads to instability. Long periods of calm tend to be followed by extreme volatility.

The future is global micro

Is there any future for global macro? That depends on what your definition of “global macro is” Making bold systemic predictions about surface level data is unlikely to lead to profits. Yet global macro’s main benefit is its flexibility to take long or short positions in any asset class anywhere in the world. Although trades in large liquid markets get the most attention, the analytical techniques of global macro can also uncover insights leading to lucrative opportunities less liquid frontier, emerging, and alternative markets.

The future of global macro will involving finding bottom up industry and company specific insights that fit with top down shifts: global micro. Steven Drobny mentioned this evolution in Inside the House of Money . Indeed most quantitative techniques of the original macro greats are commoditized. Analysts need to look beyond headline numbers numbers for less obvious global micro trends and second order impacts on tradeable assets.

Capital flows and valuations have a funny historical tendency to overshoot in both directions. Many investors build up leveraged positions based on stale fundamental inputs, and when they wake up to a new narrative taking over the market, they must rush to a crowded exit. What will be the next gestalt shift in which a new narrative takes over markets?

The next gestalt shifts

Don’t try to play the game better, try to figure out when the game has changed

Over coached football players do not respond well when a game takes an unexpected turn. Investors schooled in calmer markets may similarly struggle with renewed volatility.

Many of the classic macro bets(and blowups) involved major breaks in fixed currency regimes. Sometimes the big trade(or blowup) involved direct currency exposure. Other times it involved investments impacted by second order effects. Its possible that the big macro trades of the future will be more subtle, and play out over many years away from headlines before becoming obvious.

For the past few decades, global trade was getting generally more open. That is starting to reverse. The WTO dispute settlement mechanism will completely shut down next month because the Trump administration is blocking new appointments to the appellate body. Trump’s attitude is just an extreme manifestation of a global trend towards populism and trade conflict. At best, there will be a spaghetti bowl of bilateral agreements, instead of a large open multilateral trading system. Companies will need to dedicate more resources to supply chain strategy.

At the same time, emerging markets are starting to trade more with each other than with the developed world. Africa might become the world’s largest free trade area. China is attempting to facilitate more commodities trading without using the dollar. As China develops its own bond markets, it will invest less in US dollar based debt markets. As the world shifts to cleaner energy, oil producers will have fewer dollars to recycle into US capital markets. The relative importance of the US dollar and of major US companies is likely to decline.

Often policy changes have second order impacts on individual businesses because they alter competitive forces in their industries. Indeed its difficult to find an example of businesses that are completely immune to change in international trade policy.

Reality and narratives change at different paces. Narrative changes alter capital flows ultimately impacting valuations.

Here are some other speculations on what shocks or regime shifts might occur:

- I don’t have a strong view on inflation, but do find it concerning how few S&P 500 companies will do well if we encounter high inflation. Its commonly accepted wisdom that low inflation will continue. Yet most analysts are only considered demand driven inflation, and ignoring possible supply side shocks. There has been little investment in new production capacity for many key over the past decade. Note the conspicuous absence of resource companies in the top holdings of any indices. More insidiously, if certain prominent venture funded startups shifted from growth mode to harvest mode, and suddenly needed to make money, they would be forced to raise prices, impacting consumers directly (See: Cheap Stuff and Cheap Capital) . Alternatively, if we face deflation, then debt burdens on over leveraged companies and consumers will be a much greater drag on growth.

- If negative interest rates continue, they’ll force banks and insurance companies to find new business models, or slowly perish. If negative interest rates reverse, it will be a shock to a lot of overleveraged companies

- Pension funds are a looming disaster in many western countries. The government will overreact somehow when it becomes a social issue.

- Many investors, including pension funds, have rushed into illiquid alternatives such as private equity in search of higher returns. It is likely that those investments will fail to deliver the expected returns, and worse yet, they might be illiquid for longer than expected.

- ETFs have grown from obscure backwater to the default investment option for both institutional and retail. Many ETFS are invested in illiquid assets- creating the potential for a unique type of death spiral. The SEC recently made some changes to its filing requirements which might make it easier to preemptively find which ETFs are most vulnerable.

See also:

Highlights From Recent Hedge Fund Letters: 2019Q3

I love reading investment fund letters. This business requires a rare combination of variant insight and brutal intellectual honesty, which the best managers express in their writing. My highlights from the best letters I read this quarter are below, in no particular order. In this piece I mostly avoid quoting on specific stocks, and focused on broad investing and psychology themes. You can find plenty of investment ideas by following the links to the letters. This quarter several funds discussed the value/growth divide, the underappreciated risk of inflation(or deflation), business impact of negative interest rates, and mental model challenges in investing.

Thanks to the generous curators that make this possible. Mine Safety Disclosures is probably the best single source for hedge fund letters. They’ve sought out and organized many off the beaten path managers that I wasn’t reading before. The investment letter page on Reddit is another great source. I found several of these letters on twitter as well.

Vltava Fund

Vtltava Fund had one of my favorite letters this quarter. Here is their perspective on hyperbolic discounting :

I always say that one can learn a lot just by looking around oneself, seeing how the world works as well as how people perceive it. The way people perceive the world is then reflected in how investors (a subset of people) perceive the events on the capital markets (a subset of the world). The aforementioned tendency to overestimate short-term events and underestimate the importance of longterm trends is very strongly demonstrated in both cases. (Finance theory even has a name for this: hyperbolic discounting.)

On long term vs short term:

If we as investors were to profit from shortterm events, we would have to be able to recognize the truly fundamental ones in real time as they are happening. This is practically impossible, and even the effort to do so might bring very negative results, because in most cases it will transpire that one has overreacted to something that in the end will have been of no practical importance. We find it is much better to take the approach of betting on long-term expected developments in society.

One of the most cogent defenses of the valuable role that the finance sector can play in society:

For the capital market to work well and efficiently and for it to allocate capital at low costs, there must exist a sizeable number of entities of various types. Vltava Fund is one of those entities. Our role in the overall system is twofold: we act as intermediaries and analysts. We collect free capital from investors who want to invest and then analyse the individual investment opportunities to determine those into which we invest the collected capital. Even though we are just a tiny cog in the gigantic global markets machine, I am very proud of the work we do and how all of us associated with investing in Vltava Fund contribute collectively to the general progress, growth of wealth, and betterment of society.

Tollymore

Tollymore on epistemic humility and the Gell-Mann effect:

Serious media publications invent stories to explain outcomes, without the resources or inclination to determine causality. This often manifests itself in major descriptive U-turns as the outcome changes with the wind. The matters about which financial and political journalists opine are complex. This limits the mechanism to scrutinise these stories and hold their authors to account. And there is value to their readers and listeners, who can paraphrase talking heads’ memorable soundbites at cocktail parties rather than acknowledging ignorance or retrieving the relevant facts from their addled brains. Authority bias plays a role: media appearance confers credibility, the belief in which is counter to independent thought and self-awareness. Unsubstantiated conjecture is rife. As Mr. Crichton puts it: “one problem with speculation is that it piggybacks on the Gell-Mann effect of unwarranted credibility, making the speculation look more useful than it is”.

The goal of epistemic humility is consistent with maintaining a careful distance from today’s media. To exercise good judgement, we should shield ourselves from the Gell-Mann effect. Financial markets, political and economic systems, unlike meteorology, are reflexive; participants are second guessing one another and the bases on which decisions are made are altered by the decisions themselves. Speculation thrives because it is cheap and speculators are not held to account, but forecasting is foolish when nobody knows the future.

Epistemic humility is a key concept I try to apply in my approach to life.

Greenhaven Road

Greenhaven Road discussed how they subdivide investments in high quality companies into those that are bets on the status quo continuing, vs those that are bets on the status quo changing.

They are also SPAC curious. They rarely do SPACs, but interesting what he goes through when he does they go to extreme lengths to compete due diligence, which they discuss in a case study.

Also, they have decided to make an investment in South Africa, which is a bit unusual for them. Here is some of their reasoning:

Why Bother with South Africa? For me, there are two parts to the answer. The first is a desire to hold some non-U.S. companies. While it is true that the world catches a cold when the United States sneezes, South Africa is in the interesting position of having not meaningfully participated in the last decade’s equity market growth due to poor political leadership, poor policy choices, and corruption. I believe that new leadership and positive reforms are likely to place South African equity markets in a position to be less correlated to developed equity markets yet produce positive returns, albeit more volatile. This is intended to be rational diversification.

The second and more important reason to venture to South Africa is the potential for returns. With a bit of continued growth, operating leverage, and anything approaching a fair multiple, I believe that the price of the shares we are acquiring could very realistically go up 5X. A hundred things can prevent that type of return from being realized, but given how absolutely beaten down South Africa is from a valuation perspective, any return to normalcy could produce abnormally positive returns.

They have some great points. We’ve also found opportunity in Africa.

Alta Fox Capital

Alta Fox on the concept of zooming in and zooming out:

The concept of “zooming in and out” is an important one for my investment process, both from a single idea and a portfolio construction perspective.

For any individual idea, it is important to “zoom in” to understand the unit economics of a business, appreciate the finer nuances of the financial model, and to develop a sound valuation technique. However, it is equally important to “zoom out” and to understand at a higher-level what could go wrong, develop intuition for risk and uncertainties that transcend a few valuation scenarios, and know when to ride winners or when to fold losers. For a broader portfolio management perspective, it is also important to zoom in and out. It is important to track performance relative to indices over time as that is ultimately the measuring stick, and if the market is disagreeing with you, it is important to know why. However, one has to zoom out and focus on the process because too much focus on short-term performance is absolutely detrimental to day by day decision-making.

The abilities to zoom in and out are different skills. This is one of the primary distinctions between a good analyst and a good portfolio manager. They have complementary, but different, skill-sets. An analyst is most often tasked with “zooming in,” which normally involves ripping a business apart and understanding the filings at a very rigorous level. A portfolio manager, on the other hand, must have an overarching philosophy on how to allocate scarce research time to specific ideas, passing on others, how to size positions, etc. The best investors are capable of simultaneously zooming in and out.

Firebird Management

Firebird on negative interest rates:

In theory, companies trade at the present value of all future earnings. There are two key inputs to this: earnings and the discount rate. Companies that are growing earnings faster should be valued higher than companies with a slower growth rate, but how much more depends on the discount rate.

Consider a simple thought experiment at different interest rates: Company A is growing earnings at 2% per annum while Company B is growing at 15%. At a 7% blended discount rate, Company A is worth 17x this year’s earnings, while company B is worth 107x! Company B is value higher but has a much higher sensitivity to interest rates. A mere 1% change in the blended discount rate leads to 35% drop in value of Company B, while Company A valuation drops by only 15%

Note we also wrote up an extensive Negative Interest Rates Thought Experiment here. The implications across the economy are startling.

Of course, so are the implications of reversing negative interest rates, as Firebird points out:

In the U.S. market, growth companies have been outperforming value dramatically since the beginning of 2015, when we first started seeing corporate debt trading in negative territory. We believe that this outperformance is in large part due to repricing the cost of capital in light of the likelihood that low rates could persist for longer than originally anticipated. With the negative impact of low rates becoming more apparent every day, it is not surprising that the market reacted to the possibility that the policy of low negative interest rates may be in question.

Third Point

According to Third Point, the markets aggregate results have masked a “tumultuous factor rotation” taking place underneath the surface.

In August, equity portfolios tied to momentum or the near inverse – “laggards” – outperformed, as markets inflated assets reflecting economic weakening in a low inflation/low growth world. These momentum asset biases – favoring large cap over small cap stocks, growth versus value, or “min vol” strategies – became increasingly correlated, crowded, and sometimes expensive. The equation extended itself more acutely in secular growth names and similarly punished unloved shorts.

Third Point has increased its emphasis on activism. Currently activist names account for 40% of their assets, the highest percentage in history.

Askeladden Capital

Askeladden Capital’s letter this quarter reflected a maturing process. They discuss the limitations of primary research, and how their approach to risk has changed:

In certain circumstances (such as levered companies), we have become far more conservative, and less willing to underwrite certain outcomes with any confidence whatsoever. In other circumstances (such as recurring revenue businesses), we have become far less conservative, and far more willing to underwrite certain outcomes with a high degree of confidence. We have become more aggressive in underwriting knowable factors which we can understand better through thorough research and become far more conservative in underwriting unknowable factors which we generally believe cannot be elucidated by research to a degree helpful for the investing process. When we aren’t sure if something is knowable or unknowable, we like to default to ´unknowable for conservatism -overconfidence is killer in our business.

Nuances like these are what drive outperformance …

The letter was also full of links to articles on mental models. Separate letter for clients that includes specific positions. I won’t disclose any specific positions , but I will say as a client that performance has been solid, and there are several intriguing investments currently in the portfolio.

Comus Investments

Comus Investment’s letter had some intriguing criticism of dividend investing:

Firstly the term dividend- investor makes no sense at all to me, and it makes even less sense than the fabricated demarcation between supposed growth and value investors. Dividend- investing often implies that one is investing with the goal to receive a currently yield at the expense of long term capital appreciation as if the two sources of returns are distinct(they aren’t)

Also, notable discussion on absurdities in the valuation in SAAS companies

Any tech investors reading this will likely roll their eyes given how often they are mentioned but I have to bring up the SAAS basket of stocks. I believe it is lower now, but last I saw the entire group of public SAAS-related stocks was valued above 10x sales. This is similar to 100 fishermen at a single lake estimating they can each catch a fish a day with only 10 fish in the lake- for the fishermen to be right the fish will have to reproduce extremely quickly. The entire industry is valued as if every investor will do extraordinarily well and each business is valued as if it will experience organic ROE’s of 20%+ for decades.

Theye also had an interesting point about how accounting changes (ASU 2014- 09B) will influence SAAS accounting

Punch & Associates

In their latest letter, Punch & Associates frames a fascinating discussion around the parallels between the Screwtape Letters (great book) and the emotional and psychological challenges investors face. Screwtape Letters are fictional letters from Screwtape, to his nephew Wormwood, part of an underworld organization charged with taking souls from people trying to live a righteous life.

parallels exist between the forces (temptations, distractions, habits) acting on the Patient and the forces impacting the hearts and minds of individual investors. While these forces may not be described as demonic (some may be), and while the fate of one’s soul may not hang in the balance, the fact that these forces exist and that we are all vulnerable at times does indeed matter. The world is not perfectly architected so that you can get rich, beat the S&P 500, or even reach your financial goals. Quite the opposite.

People’s lives go through peaks and troughs, and this impacts thaeir ability to live a good life. Similarly, peaks and troughs in the market impact people’s ability to make rational decisions.

Closely related, there are great lessons for dealing with temptation of noise:

Noise is something that we all deal with in investing and in our lives. Like Wormwood’s whisperings, it’s constant. Noise can enter into your life and cloud both your judgement and priorities. People are subject to it one moment, and then they are not. The effect of noise, therefore, undulates. It’s not enough, however, to occasionally ignore noise, because mistakes are made in moments. Wormwood’s efforts are like the noise we encounter today, constantly whispering in our ears.

Pangolin Investment Management

Pangolin Investment Management is focused on Asia, and their August letter made some interesting points about tax policy in Southeast Asian countries . Also they have some commentary on a challenging history/geopolitics situation in Indonesia. In their October letter Pangolin discussed car racing in Malaysia, and the broader meaning implications for emerging markets.

Lifestyles are changing quickly in Asia. Motor racing with all its glamour is a million miles away from Lombok’s subsistence padi farming of 20 years ago. Here, income growth lifts people from being poor farmers to basic consumers, and then on to becoming middle class discretionary spenders.

It’s not just about a GDP growth, but the massive change in people’s lifestyles that accompanies it.

Ensemble Capital

Ensemble Capital on the three types of traps they avoid:

We’ve identified three traps we want to avoid. First, the commoditization trap. This is when there’s strong management in place and an easy-to-understand business, but either a non-existent or narrowing moat. Much of a company’s intrinsic value is driven by its so-called “terminal value” – the value the business will create over the very, very long term. As such, if we’re not confident that a company can maintain or widen its economic moat beyond 5 or 10 years, estimating terminal value becomes increasingly difficult. In this circumstance, long-term returns on invested capital and growth – the two pillars of our valuation model – can decline faster than might otherwise be expected. Some investors are comfortable making a bet on a company decline being slower than market expectations – and that’s another way to make money – but we think that’s a dangerous game and one we intentionally avoid.

The second trap is a stewardship trap. This is when there’s evidence of a durable moat and an easy-to-understand business, but we lack confidence in management. We live in a hyper-competitive economy where cheap and abundant capital and new advertising platforms have made it easier than ever for challengers – whether that’s a startup or Amazon – to take on lazy incumbents and chip away at their business. Because of this, we require our companies to be managed by what we consider to be good business stewards. Our management teams need to understand how to create sustainable value and thoughtfully allocate capital.

The final trap is the complexity trap. This is when we like management and think there’s a durable moat, but we just can’t get comfortable understanding the business. Sometimes the reason is that we lack requisite domain knowledge in a specialized field. Other times, the financials are opaque, or the business operates in multiple competitive arenas and we struggle to grasp unit economics. Before investing in any company, we want to appreciate the known risks and the so-called “known unknowns” about the business, and a lack of understanding prevents us from achieving this.

Artko Capital

Artko Capital’s latest letter included discussion on investment business challenges of focusing on microcaps. Although returns in the space are lucrative, structural reasons that opportunities are left for smaller funds. Also includes a great case study on handling portfolio responsibilities as a portfolio manager when investing in turn around type situations.

Andaz Private Investment

Andaz Private Investment’s latest letter includes some provocative commentary on the real meaning of inflation statistics:

There is a prevailing argument out there that inflation is nowhere to be seen, and that deflationary forces are at play e.g. technology replacing workers, offsetting the effects of money printing. In our view, this is naive. The metric used to measure inflation (CPI) is misleading and we would argue, deceptive. In fairness, the Australian Bureau of Statistics makes no attempt to hide this and has the following disclaimer:

“In practice, no statistical agencies compile true cost of living or purchasing power measures as it is too difficult to do.”

Other bodies are not so forthcoming. Central banks have decided that this garbage-in, garbage-out statistical measure is their sacred metric, that 2.0% is their precise target, and will print money until that figure is very close to 2.0% but not over it.

….

The most crucial criteria for investment over the foreseeable future will be to hold assets and securities which can outrun inflation (e.g. businesses which can raise prices or use levers to increase profits/earnings on a per share – again undiluted – basis).

East 72

The East 72 Quarterly letter had some interesting macro discussion on company earnings trends.

Additionally, they also discussed a bunch of super cheap, esoteric investment/asset holding company investments. Listed investment companies in Australia seem like an especially interesting hunting ground these days.

It has been noteworthy that the mania surrounding Australian LIC’s, rather than subsiding, has turned to near derision in some cases. This is leading to a number of corporate actions and activist behaviour designed to close up value gaps or force liquidation against hefty fee imposts for “me-too” investment strategies. …

We have always held the belief that having permanent capital available means that a far more esoteric/illiquid investment strategy can be pursued (in essence, that’s the basis of East 72 itself). However, in these situations, care needs to be taken to retain liquidity to ensure discounts to NAV do not blow out.

Saber Capital

Great discussion on the different types of edge in the Saber Capital letter. This comment on time horizon edge is key for long term investors:

….the deterioration of the info edge has actually increased the size of the “time horizon” edge.

GMO

GMO recently released a letter called Shades of 2000:

..many investors made the case in 2000 that long-term averages were not meaningful anymore and the future would be far different from the past. From the standpoint of the world from 200-2010, those investors proved to be wrong as asset prices

Value investing is way out of favor these days, but GMO believes the current environment that value investors have had in 20 years.

Horizon Kinetics

Horizon Kinetics 2019Q3 letter summarizes their current investment positining this way:

The composition of our equity portfolios is intended to avoid making their performance dependent on the continuation of the status quo.

They discuss what type of companies might do well under different scenarios, and include this handy diagram:

Horizon Kinetics’ points out that most investors are all invested in the same group of stocks, and are not prepared for any inflation. Enroute they point out some of the absurdities of ETF land, such as the fact that the same stocks are classified as both growth, value, low vol, high dividend in different indexes.

A couple of interesting statistics, since this discussion is all about diversification. This year through September, the daily price correlation of the following indexes with the S&P 500 were all between 0.86 and 0.98, meaning that their price behavior varied almost identically with the S&P 500: S&P 500 Growth ETF, the S&P 500 Value ETF, the Russell 2000 ETF of small-cap stocks, and the All Country World Index Ex-U.S. The greatest variance, among the major equity classifications was from the Emerging Markets ETF, and that fund mirrored the S&P 500 77% of the time.

People think they are diversified, but they aren’t.

Focused Compounding

Focused Compounding discusses different types of price risks in their investments. They explains why they look for a combination of low share turnover , and low beta in order to identify underfollowed stocks. It contained this gem of a quote :

In investing: beta is like syphilis. If art, cash, gold, or bonds are inherently lousy, low returning assets (barren islands) – then, institutions and individual investors can simply switch into inherently more productive assets like stocks, farmland, timberland, real estate, etc. (fertile islands) and collectively lower the risk they won’t achieve their long-term financial goals.

They use a couple case studies to discuss why their experience has led them to personally prefer “compounders” to asset plays as well.

Silver Ring Value Partners

Silver Ring Value Partners mostly follows a bottom up stock picking strategy. However, they have decided to put on a Minsky style tail hedge, which they discuss in detail in the letter. They looked for for companies that have high debt levels and will need to refinance soon. These companies are most likely to decline severely in a panic. Its a great example of combining micro and macro- of a bottom up investor, productively worrying from the top down.

See also: Thinking and Applying Minsky

Templeton & Phillips Capital Management

Tempelton & Phillips latest letter has interesting commentary on how the value and growth divide is blurring when you look carefully. (see also: Why All Great Investors Are Intellectual Cross Dressers)

Excellent analysis of how intangible assets influence modern balance sheet analysis:

…the assets driving economic gains today are more closely related to Mickey Mouse in nature, than they are to the tangible assets that statistical measures, accounting methods, and valuation methods were designed around in the last century. This reality has created significant challenges for today’s economists and accountants, who still struggle to account for intangible assets that defy being touched, seen, measured, valued, and in some cases even fully understood. Rather than tackle the anomalous values of Mickey Mouse, or the formula for Coke,

economists and accountants today are tasked with collecting, interpreting and recording data representing a widely expanded realm of intangible assets including: in-house proprietary software, customer databases, customer network effects, business processes, and organizational structures. So, while the assets listed above are very real to shareholders, and tend to be more durable than not, the business activities used to create them flow through the income statement as expenses, rather than get recorded on the balance sheet as an investment. In sum, the financial parties that collect and report data to the markets are failing to capture an increasing amount of economic activity tied to today’s growth in intangible assets.

….

One final note here is that we believe in order for a Ben Graham style asset-based valuation approach to be successful today—such as the widely used price to book ratio—the analysis would need to make an estimate regarding the value of intangible assets (not fully reported in financials) in order to calculate a reasonably accurate ratio. Since many intangible assets are not counted in traditional book value, the price to book value without any adjustment appears inflated (and expensive). Similarly, a low price to book ratio without any adjustments implies to us the possible need for asset write-downs or a firm’s reliance on underperforming tangible assets. Since low price to book ratios are a key focus for the “value” indices, we believe

these measures have a bias towards selecting firms with less productive assets. To the extent this is true, this collection of assets are very likely to underperform the overall market, much less the growth stocks where earnings estimates are growing even faster (but may not be sustainable).

White Crane

White Crane discusses the bifurcation of the credit markets between companies that can raise tons of easy money on easy terms, and those unable to raise any at all.

Such bifurcation of credit markets is often witnessed in the latter stages of credit cycles, as the availability of capital erodes. With credit availability becoming finite, lenders allocate only towardsselect borrowers, while others are either forced to pay exorbitant rates or seek other forms of Capital.

In order to take advantage of this market bifurcation, and a potential transition into a broader credit downturn, the Fund has built short positions in a basket of corporate credit securities.

These short positions can be grouped into two categories:

1) Investment grade credits that currently have access to unlimited amounts of low-costcredit; and

2) High yield credits that, in our opinion, do not have access to capital markets – yet are being priced as if they are investment grade credits with unlimited access to inexpensive

The common theme between all the credits in our short basket is that the all-in negative carry is low and they each have specific catalysts that we believe will result in a re-rating of the securities. Through this basket, we have created inexpensive capital structure put options where our downside is limited (i.e. essentially the negative carry) and our potential upside is substantial should our identified catalysts unfold. We expect to continue adding to this basket of credit shortsas the credit cycle becomes increasingly elongated and additional opportunities emerge.

Saga Partners

Saga Partners latest letter on investing in a time of heightened uncertainty

… when is there not a heightened sense of uncertainty in the markets? And when markets do inevitably panic again, as they did in the fourth quarter of last year, will investors then overcome their fears and say now is the right time to invest? Or will they wait until things calm down and become less uncertain?

We are certain that another recession will happen sometime in the future, but we do not know when it will happen, how long it will last, or how extreme it will be. We do not even know how the market will react going into and coming out of it. We do know during 2008 following the Lehman Brothers bankruptcy and subsequent financial meltdown, the outlook at the market lows was far from certain. We prefer to keep our heads down, ignore the noise, and simply look for the best opportunities we can find given the information we have today. As we’ve noted before, more money has been lost waiting for corrections or trying to anticipate them than has been lost in the corrections themselves.

On value vs growth:

A company is neither cheap nor expensive because of where it sells relative to recent fundamentals. These classifications of value or growth are just a convenient box ticking, quantitative oriented practice used by consultants which can distort the investing process. While different styles, genres, or investing factors may go in and out of favor at times, at the end of the day, the value of a stock is all the cash that can be taken out of a company going forward.

They also had a detailed discussion on how fee structure impacts ultimate returns to investors.

Forager Funds

In contrast with Horizon Kinetics, Forager Funds argues that it might actually be deflation for which investors are most egregiously underprepared.

Many investors assume that “what goes down must go up”. Many of our clients lived through the inflation of the 70s and 80s and seee its return around every corner. But what if that period was the anomoly rather than the rule. We all thought that the stimulus andgrowth in money supply after the financial crisis was certain to kick start an inflationary spiral. It hasn’t. In fact, inflation has been worryingly low. Best prepare, I would suggest, for a sustained period of zero rates.

More importantly, what do these zero rates imply about the future of the economy? What if, rather than rates going up, we are headed for a long period of low growth and deflation?

Low nominal rates are not necessarily a panacea for borrowers. It feels like it because the interest payments today are so low. But if we are headed for a deflationary world, its repayments later in life that you need to worry about.

The world might be “turning Japanese. Forager’s research into ASX listed Japanese property trusts leads to some startling conclusion of what that might be like. They were initially intrigued by how the companies were, but then realized that with wages, and rents falling in 18 out of 20 years, they might think they were earning a good return only to one day find the property was worth less than the debt.

Today’s low rates are sending a very important signal. The world is turning more and more Japanese.

If that is the world we are headed for, be very wary of debt.

In addition to this macro commentary, the letter includes a lot of intriguing off the beaten stock ideas in Asia.

What great managers did I leave out? Send me your favorite hedge fund letters.

Renaissance Technologies Buying Microcaps

Those of us that invest in microcaps are accustomed to high volatility on low trading volume. Sometimes the company will report major news, and nothing happens to the price until a year later. Other days there are 20% swings when somebody places a 100 share market order.

When there is a surge in volume lasting more than a couple days and a definitive trend in price, it’s not uncommon to see Renaissance Technologies file a 13G, indicating a 5%(or higher) position.

What would such a large systematic trading firm be doing in this part of the market? Aren’t microcaps usually owned by fundamental focused investors? Funny thing is sometimes there is sufficient volume and a definitive trend, causing systematic traders to get interested. The market switches from value dominated to momentum activated, even in microcaps.

This is part of a broader phenomenon explained well in Market force, ecology and evolution:

If a substantial mispricing develops by chance, value investors become active. Their trading shrinks the mispricing, with a corresponding change in price. This causes trend followers to become active; first the short term trend followers enter, and then successively longer term trend followers enter, sustaining the trend and causing the mispricing to cross through zero. This continues until the mispricing becomes large, but with the opposite sign, and the process repeats itself. As a result the oscillations in the mispricing are faster than they would be without the trend followers.

In real life, prices are almost never at their equilibrium.

The Paradox of Alternative Data

“My God, they’re purple and green. Do fish really take these lures?” And he said, “Mister, I don’t sell to fish.

Informational edge can drive fantastic alpha while it lasts. This explains the increasing investment industry focus on non-traditional data sources, aka alternative data. If you are the first to acquire a new alternative data set, you might be able to develop insights no one has.

Yet once a lot of people are using it, it is less likely to drive alpha. It might be table stakes to not get screwed, or it might be already be instantaneously reflected in the price of assets.

Furthermore, most opportunities really hinge on a couple factors- more info isn’t always useful. That won’t stop the alternative data industry from doubling to $400 million by 2021, as a widely cited Tabb Group report predicts This is worth considering while one is caught up in an alternative data arms race.

Yet some data sets genuinely will provide an edge.

Perhaps a data set that no one else is looking at provides the edge you need. If a data set isn’t established as useful, the provider of that data will probably offer it cheaper in the early days of their business. There are so many alternative data providers out there, that marketing strategy is important for startups.

Ironically, the provider can charge higher price once word about its value gets out among investors.. So later adopters might pay more for an edge that is already gone.

Of course eventually someone will put all the data online for free and meta data of how investors use that alternative data can also be useful.

Now can I interest you in an alternative data feed that will make all your dreams come true?

See also: https://ockhamsnotebook.wordpress.com/2016/09/18/the-hard-thing-about-finding-easy-things/

The ecological consequences of hedge fund extinction

Investing goes through fads. Investing strategies and fund structures(1) go in and out of style. Nowadays long/short hedge funds are out and infrastructure funds are in. Within the public equity markets, value is out, growth/momentum is in. Each time this happens, people forget how the cycle repeats.

In fact, one CIO contended that if he brought a hedge fund that paid him to invest to his board, the board would dismiss it without consideration — simply because it’s called a hedge fund, and hedge funds are bad.

Institutional Investor

Hedge funds may have to do a name change if they want to raise capital.

Remember last time?

And yet people forget:

Allocators woke up craving the next rising hedge fund star and couldn’t invest enough at high and increasing management fees after the widespread success of long-short funds in the weak equity markets of 2000-2002. Board rooms back then castigated CIOs for not having long-short equity hedge funds in their portfolios.

This isn’t the first time:

People forget that 40 years ago, officials such as Paul Volcker of the Federal reserve wanted an active hedge fund industry to absorb the risk that was not well managed by state-insured banks.

Financial Times

Each investment strategy picks up a certain type of risk(and potentially earns a profit in doing so)- if a strategy disappears that particular risk can become a systemic issue. Fortunately, around this time it also becomes more lucrative to bear the risk others are unwilling to bear. Eventually the risk reward tradeoff starts to make sense again.

Different, different, yet same

In the 1960’s Warren Buffett put up ridiculous returns, and Alfred Winslow Jones proteges profitably exploited anomalies in markets. By the mid 1970’s of there were many articles about hedge funds shutting down though. Industry AUM declined ~70% peak to trough. Nifty fifty boom and bust followed by the long nasty bear market. But as the institutional architecture of international trade and currency shifted we entered glory years of global macro/commodities traders. Then the 80’s were great for Graham deep value and Icahn style activist investing after the 70’s bear market left a huge portion of the market selling below liquidation value.

Likewise late 90’s again saw the death of hedge funds as day traders in pajamas earned easy returns from the latest dot-com- until the crash. Yet out of the rubble of the tech bubble rose a new generation of great hedge fund managers. There was rich pickings for surviving value hunters- and those with the guts and skills to execute became household names a few years later. Many value managers that nearly went out of business during the tech bubble put up ridiculous numbers 2000-2002 and through the next financial crisis. (See: The arb remains the same)

The greatly exaggerated death of a style gives rise to an environment where there is a plethora of opportunities for something similar to that style to work. Each time the narrative in the greater investment community favors some type of uniform strategy, and LPs give less capital to other strategies- causing them to nearly die off. But then the lack of people pursuing the out of fashion strategy makes its return potential more lucrative. Eventually someone finds a new method to pick up those dollar bills on the ground that shouldn’t exist.

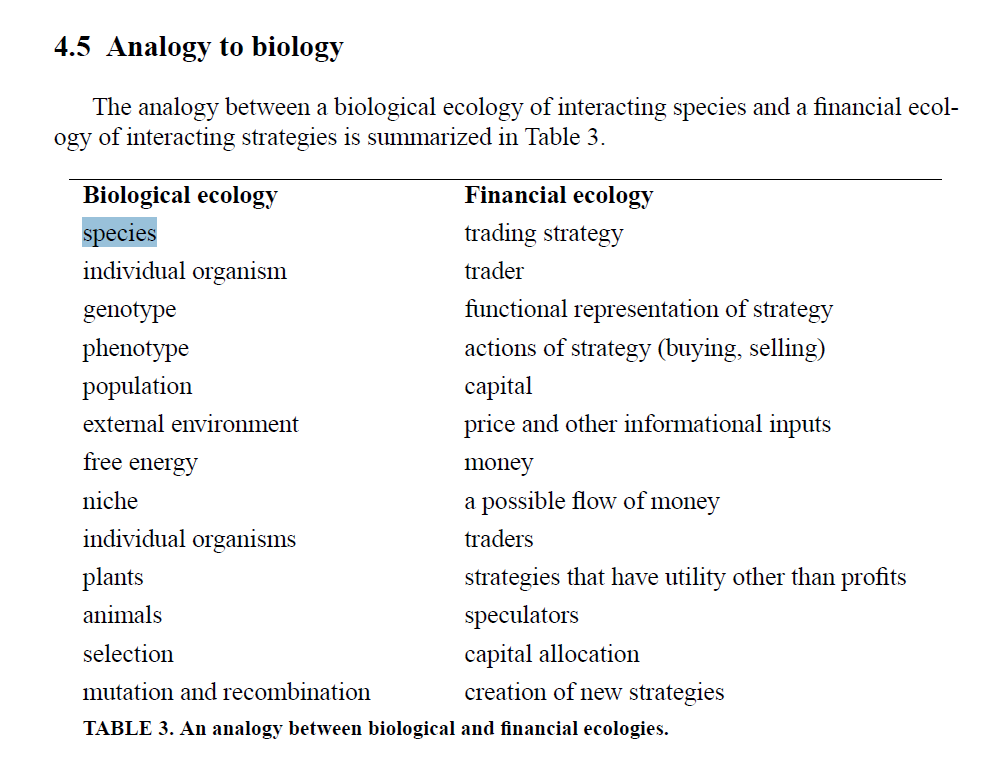

Economics emphasizes rational actors and equilibrium. Yet the messy reality is far more complicated. Ecology is a far more useful mental model.

A giant self over-correcting ecosystem

There is in ecological function to speculative capital and over time there should be some excess returns to those willing to take mark-to-market losses

Financial Times

Like biological species, financial strategies can have competitive, symbiotic, or predator-prey relationships. The tendency of a market to become more efficient can be understood in terms of an evolutionary progression toward a richer and more complex set of financial strategies.

Market force, ecology and evolution

Ecology emphasizes interrrelationships between different individuals and groups within a changing environment, and indentifies second order impacts.

Thinking like a biologist

One can develop a useful framework by replacing species with strategy, population with capital, etc

Flows and valuation interact, self correct, and overshoot.

….capital varies as profits are reinvested, strategies change in popularity,and new strategies are discovered. Adjustments in capital alter the financial ecology and change its dynamics, causing the market to evolve. At any point in time there is a finite set of strategies that have positive capital; innovation occurs when new strategies acquire positive capital and enter this set. Market evolution is driven by capital allocation.

Market evolution occurs on a longer timescale than day-to-day price changes. There is feedback between the two timescales: The day-to-day dynamics determine profits, which affect capital allocations, which in turn alter the day-to-day dynamics. As the market evolves under static conditions it becomes more efficient. Strategies exploit profit-making opportunities and accumulate capital, which increases market impact and diminishes returns. The market learns to be more efficient.

Evolution

When an ecoystem is overpopulated with a certain species, it eventually overshoots and results in mass starvation. Populations fluctuate wildly across decades, and sometimes species go extinct or evolve into something that seems new.

New conditions give rise to new dominant species.

See also:

George Soros on disequilibrium analysis

The arb remains the same

Book:

Investing: The Last Liberal Art

Hedgehogging

More Money than God

(1) Although I am frequently pedantic about the differences between structure, strategy, and sector, many in the media seem to use these interchangeably when discussing reversion to mean situations. Fortunately they all exhibit the same boom/bust phenomenon, so I am using them interchangeably here.

The arb remains the same

Imagine if Warren Buffett of 1960 puts down the deadtree 10-K he got in the mail and time travels forward to 2019. Then he looks over the shoulder of an analyst at present day O’Shaughnessy Asset Management. He would find the scene unrecognizable.

Or, if the original Jesse Livermore time traveled from the 1920s stock exchange to the present day trading floor of DE Shaw or Renaissance. Again, completely unrecognizable.

Back in the day people went to the SEC office in the Washington DC to access annual reports faster. That was how one got a fundamental edge. Now people scrape filings the minute they come out. Or use satellites and credit card data to get an edge on information before it hits regulatory filings. People used to gauge momentum by looking at the facial expressions of other traders, now they use complex computer models. People mine market and fundamental data around the globe looking for a bit of an edge. New techniques, same thing.

Over time there is the change in the physical activities, and words we use to describe the process of identifying and exploiting market inefficiencies. Nonetheless the ecological function is the same. Investors are just looking for mispriced risk, and exploiting it till its no longer mispriced.

Around the world there are unfair coins waiting for someone to flip them. Arbitrageurs will need to use weirder and weirder methods to find and exploit them. Methods change, but the arb remains the same.

See also:

The hard thing about finding easy things

Riches among the ruins

Thinking and Applying Minsky

Hyman Minsky developed a framework for understanding how debt impacts the behavior of the financial system, causing periods of stability to alternate with periods of instability. Stability inevitably leads to instability. Minsky identified three types of financing: Hedge financing, speculative financing, and ponzi financing. It seems some people only remember Minsky every so often when there is a financial crisis, but the framework is useful in all seasons.

Hedge Financing

An asset generates enough cash flow to fulfill all contractual payment obligations. For example, a conservatively leveraged rental property that generates enough rent to pay down the entire mortgage over time, regardless of the change in quoted property prices. Or a company that issues some bonds, then pays them back using cash flow from the business Generally hedge financing units have a lot of equity down. Even a market crash, will not cause an investor to suffer permanent capital impairment if they only use hedge financing. The equity holder who uses hedge financing will never depend on the capital markets.

Speculative Financing

An asset generates enough cash flow to fulfill all debt payments, but not the full principal amount. In this case debt must be rolled over, or the asset must be sold, in order to pay back the full amount. For example, a rental property financed with some sort of balloon payment structure that generates enough cash flow to pay off mortgage payments up until the balloon payment at the end. When the balloon payment comes due, the investor must roll over the debt or sell the asset. An investor ttat uses speculative financing is dependent on capital markets. If there is a delay or a problem in refinancing, they could lose their investment.

Ponzi Financing

This is basically “greater fool” investing. Ponzi financing means there is so much leverage n an asset, that the investment must be refinanced, or sold at a higher price quickly, otherwise the entire investment is lost. Sometimes property purchases will be financed with shorter term bridge loan. If the bridge loan can’t be refinanced with longer term mortgage, the investor is out of luck. Towards the end of the market cycle, many companies will be issuing bank loans or bonds that can only be repaid by refinancing. If their unable to refinance, they go bankrupt.

Use of ponzi financing means the investor is highly dependent on capital markets. The slightest disruption in capital markets or change in interest rates/inflation results in a large capital loss.

Junk bonds are not inherently bad. A higher interest rate can in many cases compensate for greater risk, especially across a portfolio of non correlated investments. Howeve, duringthe junk bond era, many companies

Similarly securitization is not inherently bad. It can allow capital to flow more effeiciently. But often banks would end up aggressively securitizing, with the need to sell the loans they made quickly. But if they weren’t able to resell they couldn’t hold the loans. This happened to Nomura during the Asian financial crisis, as vividly told in this Ethan Penner interview.

Ponzi in this case is not illegal activity, just extremely risky. Of course those investors who finance their activities ponzi style often end up feeling the need to commit illegal acts. The Minsky Kindleberger model is useful here.

The cycle repeats

During a recession is very difficult to get any debt financing that is not “hedge financing”. Lenders are scarred from the last cycle, and there is a paucity of available risk capital. But a price rise, and investors get more comfortable, more and more financing becomes ponzi units In fact. Lenders may lower their standards and become more accepting of ponzi units.

Throughout the market cycle, more and more financing is ponzi units. Eventually there is no greater fool to sell to. When many ponzi units are forced to sell at once, it eventually leads to a collapse in values. This is how stability inevitably leads to stability. The cycle repeats.

How to apply this?

To protect my capital, I look try to mainly expose myself to hedge financing, with a small amount of speculative financing. I position my portfolio so that I don’t need to refinance anything or sell anything in a rush. When I invest in leveraged companies with speculative or ponzi financing, I make it small position(always in some sort of limited liability structure), and generally won’t average down much if at all. Additionally, when I notice an increase in ponzi financing in the markets, I become more cautious.

Leverage, like liquor , must be consumed carefully if at all.

See also:

The next level of shareholder activism

…shareholder activism can be put to good use and bad. It challenges inefficient corporations that waste valuable assets, but it can also foster destructive and destabilizing short-term strategic decisions. The key issue in an activist campaign often boils down to who will do a better job running the company—a professional management team and board with little accountability, or a financial investor looking out for his or her own interests.

–Dear Chairman: Boardroom Battles and the Rise of Shareholder Activism

Elliott Management is a prominent hedge hedge fund with a succesful 4 decade track record, perhaps most infamous for seizing a ship from Argentina’s Navy during a debt dispute back in 2012. Elliott has become a most widely known as an activist investor in recent years. Its impact has also been important because it has shaken up large companies previously thought immune to activists. Furthermore, Elliott has been a successful activist in Europe and Asia, where conventional wisdom once held that activism didn’t really work.

Elliott’s tactics are extreme, and controversial, but they work. Although sometimes there are unintended consequences- Elliott has indirectly affected regime change in two different sovereign nations. Fortune’s latest issue has an in depth profile of Elliott Management that is well worth reading.

For more on the history of corporate activism, and its impact on the history of capitalism, Dear Chairman is a definitive guide.

Business history teaches us that the pursuit of profit brings out an extreme and obsessive side of people. When we harness it well, we get Wal-Mart, Les Schwab Tires, Southwest Airlines, and Apple. When we don’t, we get salad oil swindles, junk bond manipulations, and Steak ’n Shake funneling its cash to its CEO’s hedge fund. The publicly owned corporation has been a remarkable engine engine for progress and economic gowth because it can place large amounts of capital in the hands of the right people with the right ideas. Without proper oversight, however, public companies can squander unimaginable amounts o money and inflict great harm on everything around them. The emergence of the shareholder as the dominant force in corporate governance has bestowed a tremendous amount of power and responsibility on investors….