Category: Global Macro

Global macro is dead, long live global micro

After Louis Bacon closed Moore Capital this past week, both the FT and the Economist had interesting articles on the future of global macro investing. They struck almost opposite tones, each making good points about the current and future reality. Global macro will return, but likely in an unexpected form.

Stability destabilises a generation of macro hedge fund stars

A league of their own: Do not write off the macro hedge-fund manager just yet

Stability killed the macro star

The glory days of global macro as we know it started when the Bretton Woods system collapsed in 1971, ending fixed exchange rates. Broadly speaking, there were two different groups of investors who entered this environment and profited immensely. The first was people with long/short equity experience in global markets and included George Soros, Jim Rogers, and Michael Steinhardt. The second group included people with a physical commodities and futures background. The Commodities Corporation trading firm trained and/or funded many macro investors including Bruce Kovner, Paul Tudo Jones, Louis Bacon, Michael Marcus, etc.

The dramatic changes in the institutional architecture of international trade and finance created a volatile playground for these investors. Exchanges developed new derivatives instruments for trading newly volatile currencies and increasingly global commodities markets in a high inflation environment. Global trade started to open up dramatically, and global supply chains spidered out in response to changes in policy and technology. Many investors made or lost fortunes betting on big equity moves like the 1987 stock market crash(shortly after Greenspan became head of the Fed), or the breaking of fixed currency regimes such as the sterling crisis of 1992, the Asia crisis of 1997, Russia in 1998, etc. There was also the emerging market debt crisis in the 1980s and the surprise interest rate hike in 1994.

After the 2009 global financial crisis, interest rates and inflation have been abnormally low. The euro crisis notwithstanding, markets have lacked volatility. With no volatility its hard for the traditional global macro style to work. Moore and his proteges have all closed down recently. The decline of the legacy macro investors is just one part of the broader decline of active management. Its been a long torturous capitulation.

Yet stability leads to instability. Long periods of calm tend to be followed by extreme volatility.

The future is global micro

Is there any future for global macro? That depends on what your definition of “global macro is” Making bold systemic predictions about surface level data is unlikely to lead to profits. Yet global macro’s main benefit is its flexibility to take long or short positions in any asset class anywhere in the world. Although trades in large liquid markets get the most attention, the analytical techniques of global macro can also uncover insights leading to lucrative opportunities less liquid frontier, emerging, and alternative markets.

The future of global macro will involving finding bottom up industry and company specific insights that fit with top down shifts: global micro. Steven Drobny mentioned this evolution in Inside the House of Money . Indeed most quantitative techniques of the original macro greats are commoditized. Analysts need to look beyond headline numbers numbers for less obvious global micro trends and second order impacts on tradeable assets.

Capital flows and valuations have a funny historical tendency to overshoot in both directions. Many investors build up leveraged positions based on stale fundamental inputs, and when they wake up to a new narrative taking over the market, they must rush to a crowded exit. What will be the next gestalt shift in which a new narrative takes over markets?

The next gestalt shifts

Don’t try to play the game better, try to figure out when the game has changed

Over coached football players do not respond well when a game takes an unexpected turn. Investors schooled in calmer markets may similarly struggle with renewed volatility.

Many of the classic macro bets(and blowups) involved major breaks in fixed currency regimes. Sometimes the big trade(or blowup) involved direct currency exposure. Other times it involved investments impacted by second order effects. Its possible that the big macro trades of the future will be more subtle, and play out over many years away from headlines before becoming obvious.

For the past few decades, global trade was getting generally more open. That is starting to reverse. The WTO dispute settlement mechanism will completely shut down next month because the Trump administration is blocking new appointments to the appellate body. Trump’s attitude is just an extreme manifestation of a global trend towards populism and trade conflict. At best, there will be a spaghetti bowl of bilateral agreements, instead of a large open multilateral trading system. Companies will need to dedicate more resources to supply chain strategy.

At the same time, emerging markets are starting to trade more with each other than with the developed world. Africa might become the world’s largest free trade area. China is attempting to facilitate more commodities trading without using the dollar. As China develops its own bond markets, it will invest less in US dollar based debt markets. As the world shifts to cleaner energy, oil producers will have fewer dollars to recycle into US capital markets. The relative importance of the US dollar and of major US companies is likely to decline.

Often policy changes have second order impacts on individual businesses because they alter competitive forces in their industries. Indeed its difficult to find an example of businesses that are completely immune to change in international trade policy.

Reality and narratives change at different paces. Narrative changes alter capital flows ultimately impacting valuations.

Here are some other speculations on what shocks or regime shifts might occur:

- I don’t have a strong view on inflation, but do find it concerning how few S&P 500 companies will do well if we encounter high inflation. Its commonly accepted wisdom that low inflation will continue. Yet most analysts are only considered demand driven inflation, and ignoring possible supply side shocks. There has been little investment in new production capacity for many key over the past decade. Note the conspicuous absence of resource companies in the top holdings of any indices. More insidiously, if certain prominent venture funded startups shifted from growth mode to harvest mode, and suddenly needed to make money, they would be forced to raise prices, impacting consumers directly (See: Cheap Stuff and Cheap Capital) . Alternatively, if we face deflation, then debt burdens on over leveraged companies and consumers will be a much greater drag on growth.

- If negative interest rates continue, they’ll force banks and insurance companies to find new business models, or slowly perish. If negative interest rates reverse, it will be a shock to a lot of overleveraged companies

- Pension funds are a looming disaster in many western countries. The government will overreact somehow when it becomes a social issue.

- Many investors, including pension funds, have rushed into illiquid alternatives such as private equity in search of higher returns. It is likely that those investments will fail to deliver the expected returns, and worse yet, they might be illiquid for longer than expected.

- ETFs have grown from obscure backwater to the default investment option for both institutional and retail. Many ETFS are invested in illiquid assets- creating the potential for a unique type of death spiral. The SEC recently made some changes to its filing requirements which might make it easier to preemptively find which ETFs are most vulnerable.

See also:

The Strange Case Of Benin Rice Imports

Benin rice imports more than doubled between 2015 and 2017. Its a tiny country, slightly smaller than Pennsylvania, with a population of 11 million. Yet it is now the world’s largest importer of Thai rice. Why?

Turns out the answer has little to do with cuisine, and a lot to do with incentives. Benin shares a border with Nigeria, a much larger country that put strict tariffs on rice in 2014. Smuggling rice from Benin into Nigeria became big business. (see here, here, and here)

Unintended consequences of trade policy permeate Nigerian life. One of the richest people is a cement manufacturer. It just so happens that cement has a 60% tariff. Oh, and Nigeria doesn’t exactly have great infrastructure. Basically the only businesses of any size that can survive depend on some sort of favorable policy. The textile industry can’t really compete with cheap foreign imports, for example.

Favored importers get access to USD at a favorable rate. Petroleum importers, and the politically connected get an even better rate. Everyone else has to pay nearly twice as much of the local currency (naira) to access USD on the black market. I’m not sure if there is a secondary market in whatever documents importers can use to access cheaper USD, but if there is, these documents could be quite valuable.

Department of Unintended Consequences

Tariffs and exchange controls are not necessarily bad. One can hardly blame Nigerian policy makers. Powerful political constituencies depend on favorable policy. Nigeria has had a rough few decades, and opening up to foreign competition can create disruption. But trying to understand an economy requires looking beyond immediate impact, and finding second order impacts that are the unintended consequences of intervention. Even in neighboring countries. Never underestimate the power of incentives.

Perhaps Nigeria also needs a Department of Unintended Consequences.

See also:

The ecological consequences of hedge fund extinction

Investing goes through fads. Investing strategies and fund structures(1) go in and out of style. Nowadays long/short hedge funds are out and infrastructure funds are in. Within the public equity markets, value is out, growth/momentum is in. Each time this happens, people forget how the cycle repeats.

In fact, one CIO contended that if he brought a hedge fund that paid him to invest to his board, the board would dismiss it without consideration — simply because it’s called a hedge fund, and hedge funds are bad.

Institutional Investor

Hedge funds may have to do a name change if they want to raise capital.

Remember last time?

And yet people forget:

Allocators woke up craving the next rising hedge fund star and couldn’t invest enough at high and increasing management fees after the widespread success of long-short funds in the weak equity markets of 2000-2002. Board rooms back then castigated CIOs for not having long-short equity hedge funds in their portfolios.

This isn’t the first time:

People forget that 40 years ago, officials such as Paul Volcker of the Federal reserve wanted an active hedge fund industry to absorb the risk that was not well managed by state-insured banks.

Financial Times

Each investment strategy picks up a certain type of risk(and potentially earns a profit in doing so)- if a strategy disappears that particular risk can become a systemic issue. Fortunately, around this time it also becomes more lucrative to bear the risk others are unwilling to bear. Eventually the risk reward tradeoff starts to make sense again.

Different, different, yet same

In the 1960’s Warren Buffett put up ridiculous returns, and Alfred Winslow Jones proteges profitably exploited anomalies in markets. By the mid 1970’s of there were many articles about hedge funds shutting down though. Industry AUM declined ~70% peak to trough. Nifty fifty boom and bust followed by the long nasty bear market. But as the institutional architecture of international trade and currency shifted we entered glory years of global macro/commodities traders. Then the 80’s were great for Graham deep value and Icahn style activist investing after the 70’s bear market left a huge portion of the market selling below liquidation value.

Likewise late 90’s again saw the death of hedge funds as day traders in pajamas earned easy returns from the latest dot-com- until the crash. Yet out of the rubble of the tech bubble rose a new generation of great hedge fund managers. There was rich pickings for surviving value hunters- and those with the guts and skills to execute became household names a few years later. Many value managers that nearly went out of business during the tech bubble put up ridiculous numbers 2000-2002 and through the next financial crisis. (See: The arb remains the same)

The greatly exaggerated death of a style gives rise to an environment where there is a plethora of opportunities for something similar to that style to work. Each time the narrative in the greater investment community favors some type of uniform strategy, and LPs give less capital to other strategies- causing them to nearly die off. But then the lack of people pursuing the out of fashion strategy makes its return potential more lucrative. Eventually someone finds a new method to pick up those dollar bills on the ground that shouldn’t exist.

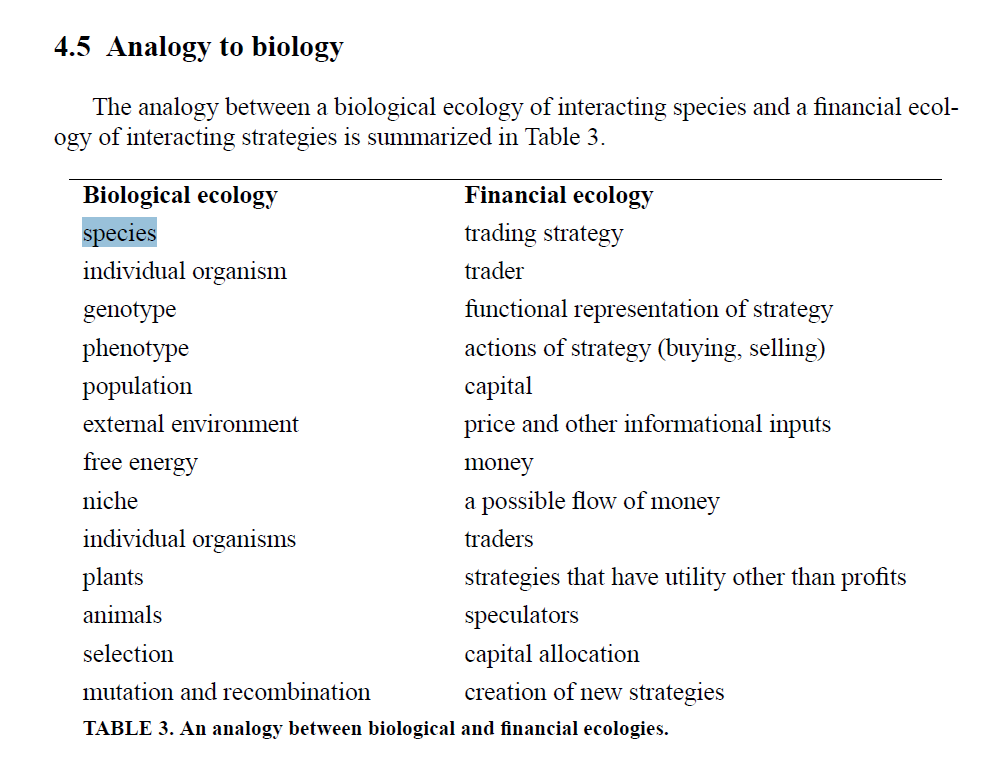

Economics emphasizes rational actors and equilibrium. Yet the messy reality is far more complicated. Ecology is a far more useful mental model.

A giant self over-correcting ecosystem

There is in ecological function to speculative capital and over time there should be some excess returns to those willing to take mark-to-market losses

Financial Times

Like biological species, financial strategies can have competitive, symbiotic, or predator-prey relationships. The tendency of a market to become more efficient can be understood in terms of an evolutionary progression toward a richer and more complex set of financial strategies.

Market force, ecology and evolution

Ecology emphasizes interrrelationships between different individuals and groups within a changing environment, and indentifies second order impacts.

Thinking like a biologist

One can develop a useful framework by replacing species with strategy, population with capital, etc

Flows and valuation interact, self correct, and overshoot.

….capital varies as profits are reinvested, strategies change in popularity,and new strategies are discovered. Adjustments in capital alter the financial ecology and change its dynamics, causing the market to evolve. At any point in time there is a finite set of strategies that have positive capital; innovation occurs when new strategies acquire positive capital and enter this set. Market evolution is driven by capital allocation.

Market evolution occurs on a longer timescale than day-to-day price changes. There is feedback between the two timescales: The day-to-day dynamics determine profits, which affect capital allocations, which in turn alter the day-to-day dynamics. As the market evolves under static conditions it becomes more efficient. Strategies exploit profit-making opportunities and accumulate capital, which increases market impact and diminishes returns. The market learns to be more efficient.

Evolution

When an ecoystem is overpopulated with a certain species, it eventually overshoots and results in mass starvation. Populations fluctuate wildly across decades, and sometimes species go extinct or evolve into something that seems new.

New conditions give rise to new dominant species.

See also:

George Soros on disequilibrium analysis

The arb remains the same

Book:

Investing: The Last Liberal Art

Hedgehogging

More Money than God

(1) Although I am frequently pedantic about the differences between structure, strategy, and sector, many in the media seem to use these interchangeably when discussing reversion to mean situations. Fortunately they all exhibit the same boom/bust phenomenon, so I am using them interchangeably here.

Thinking and Applying Minsky

Hyman Minsky developed a framework for understanding how debt impacts the behavior of the financial system, causing periods of stability to alternate with periods of instability. Stability inevitably leads to instability. Minsky identified three types of financing: Hedge financing, speculative financing, and ponzi financing. It seems some people only remember Minsky every so often when there is a financial crisis, but the framework is useful in all seasons.

Hedge Financing

An asset generates enough cash flow to fulfill all contractual payment obligations. For example, a conservatively leveraged rental property that generates enough rent to pay down the entire mortgage over time, regardless of the change in quoted property prices. Or a company that issues some bonds, then pays them back using cash flow from the business Generally hedge financing units have a lot of equity down. Even a market crash, will not cause an investor to suffer permanent capital impairment if they only use hedge financing. The equity holder who uses hedge financing will never depend on the capital markets.

Speculative Financing

An asset generates enough cash flow to fulfill all debt payments, but not the full principal amount. In this case debt must be rolled over, or the asset must be sold, in order to pay back the full amount. For example, a rental property financed with some sort of balloon payment structure that generates enough cash flow to pay off mortgage payments up until the balloon payment at the end. When the balloon payment comes due, the investor must roll over the debt or sell the asset. An investor ttat uses speculative financing is dependent on capital markets. If there is a delay or a problem in refinancing, they could lose their investment.

Ponzi Financing

This is basically “greater fool” investing. Ponzi financing means there is so much leverage n an asset, that the investment must be refinanced, or sold at a higher price quickly, otherwise the entire investment is lost. Sometimes property purchases will be financed with shorter term bridge loan. If the bridge loan can’t be refinanced with longer term mortgage, the investor is out of luck. Towards the end of the market cycle, many companies will be issuing bank loans or bonds that can only be repaid by refinancing. If their unable to refinance, they go bankrupt.

Use of ponzi financing means the investor is highly dependent on capital markets. The slightest disruption in capital markets or change in interest rates/inflation results in a large capital loss.

Junk bonds are not inherently bad. A higher interest rate can in many cases compensate for greater risk, especially across a portfolio of non correlated investments. Howeve, duringthe junk bond era, many companies

Similarly securitization is not inherently bad. It can allow capital to flow more effeiciently. But often banks would end up aggressively securitizing, with the need to sell the loans they made quickly. But if they weren’t able to resell they couldn’t hold the loans. This happened to Nomura during the Asian financial crisis, as vividly told in this Ethan Penner interview.

Ponzi in this case is not illegal activity, just extremely risky. Of course those investors who finance their activities ponzi style often end up feeling the need to commit illegal acts. The Minsky Kindleberger model is useful here.

The cycle repeats

During a recession is very difficult to get any debt financing that is not “hedge financing”. Lenders are scarred from the last cycle, and there is a paucity of available risk capital. But a price rise, and investors get more comfortable, more and more financing becomes ponzi units In fact. Lenders may lower their standards and become more accepting of ponzi units.

Throughout the market cycle, more and more financing is ponzi units. Eventually there is no greater fool to sell to. When many ponzi units are forced to sell at once, it eventually leads to a collapse in values. This is how stability inevitably leads to stability. The cycle repeats.

How to apply this?

To protect my capital, I look try to mainly expose myself to hedge financing, with a small amount of speculative financing. I position my portfolio so that I don’t need to refinance anything or sell anything in a rush. When I invest in leveraged companies with speculative or ponzi financing, I make it small position(always in some sort of limited liability structure), and generally won’t average down much if at all. Additionally, when I notice an increase in ponzi financing in the markets, I become more cautious.

Leverage, like liquor , must be consumed carefully if at all.

See also:

Sam Zell: Poet laureate of contrarians and dumpster divers

Sam Zell is the patron saint of contrarians and poet laureate of dumpster divers. He has one of the best track records of any real estate or distressed asset investor, and helped pioneer the use of REITs, NOLs, and other key strategies and structures. His excellent autobiography is a valuable lens from which to understand the last 50 years of economic history.

Although he built up his reputation in off the beaten path markets, his sense of macro timing is also surreal. He loaded up on multifamily properties at the bottom of the market in the 1970s. He sold out of a large portion of his holdings near the top of the market in 2007(although that story was a bit more nuanced than I realized prior to reading the book).

Here are my notes and highlights from the book:

A full throttle opportunist

This isn’t a dress rehearsal. I try to live full throttle. I believe I was put on this earth to make a difference, and to do that I have to test my limits. I look for ways to do that every day. After all, I think it was Confucius who said, “The definition of a schmuck is someone who’s reached his goals.” It’s up to me to keep moving the end zone, and go for greatness.

….At some point the guy I was sitting next to turned to me and asked, “So what do you do?” I replied, “I’m a professional opportunist.” And that has been my response to that question ever since.

History

Zell’s Jewish parents were on one of the last trains out of Poland, just hours before the Nazi’s bombed the train tracks and took over. Many of his ancestors perished in concentration camps. His parents reminded him of this, and it appears to have had a significant impact on his world view

Did you ever wonder how the Jews allowed the Nazis to come into Poland without taking action? I asked my father that when I was little, and I’ll never forget what he said. The Jewish community in Poland at the time was extraordinarily myopic—it had little idea what was going on in the world. And it cost most of them the ultimate price. In contrast, my father’s macro understanding of world events and the conviction to act saved the lives of my family. I apply the same strategy on a much less life-and-death scale. I rely on a macro perspective to identify opportunities and make better decisions, both in my investment activity and in leading my portfolio companies. I am always questioning, always calculating the implications of broader events. How will worldwide depressed currencies affect capital flows and world trade? Does it create opportunity for international expansion among multinational companies? What real estate needs will they have? How can we get a first-mover advantage into new markets? And on and on.

Avoiding the crowd

Zell was clearly unafraid of career risk. Several times in his career he safely sat out major bubbles, and pounced later when it all burst.

The industry has a long history of overbuilding when there’s easy money, without regard for who will occupy those spaces once they’re built. At the same time that construction cranes were dotting the horizon of every major city, the country was just starting to tip into a recession. Supply was going up and prospects for demand were not good. I was certain that we were headed toward a massive oversupply and a crash was coming. That’s when I just said, “Stop.” I was done. I stopped buying assets, started accumulating capital, and got ready for what I was sure would be the greatest buying opportunity of my career thus far. My thesis was that over the next five years, we would have the opportunity to make a fortune by acquiring distressed real estate. So I established a property management firm, First Property Management Company (FPM), to focus on distressed assets. Everyone thought I was nuts. After all, occupancies were still over 90 percent. Absorption was high. Companies were hiring. It was one of many times I would hear people tell me that I just didn’t understand.

I didn’t listen. I just stepped aside while the music was still playing. It was the biggest risk I had taken to date in my career. After all, I had a stable of investors by then. What would they think if I bowed out and the end didn’t come? That would mean I was forgoing a lot of upside for them. It was a true test of my conviction. But I had to follow the logic of supply and demand. Turns out I was right. Less than one year later, in 1974, the market crashed. Hard.

Overnight, we were buying assets at 50 cents on the dollar. At the time, financial institutions did not have to mark to market. In other words, they didn’t have to adjust the book value of their assets to the current market value those assets could actually sell for. If you were an insurance company, instead of marking to market, you could avoid taking a hit

Avoiding competition

By being contrarian, Zell avoided competition.

In 1980, Bob and I sat down and listed the reasons we didn’t like where the real estate market was headed. First, the key to our prior success had been an inefficient market. The real estate industry had always been fragmented, with valuations and projections that often varied widely. That started changing rapidly with the debut of Hewlett-Packard’s financial calculator. All of a sudden, any owner could hire an MBA with an HP-12C to run ten years of cash flows, none of which considered recessions or rent dips, and make an elaborate and sophisticated case for investment—and a bunch of eager investors would show up to check out the property.

That was not an arena we wanted to compete in. Second, up until then, lenders made long-term, fixed-rate, nonrecourse loans. But as a result of inflation in the 1970s, they got scared and switched to short-term, floating-rate loans. We believed the real money in real estate came from borrowing long-term, fixed-rate debt in an inflationary scenario that ultimately depreciated the value of the loan and increased the position of the borrower. Finally, we had always looked at the tax benefits of real estate as what you got for the lack of liquidity. All of a sudden, sellers were including a value for tax benefits in their asset pricing. So we said, “If we’ve been as successful in real estate as we have been, aren’t we really just good businessmen? And if we’re good businessmen, then why wouldn’t the same principles that apply to buying real estate apply to buying anything else?” We checked the boxes—supply and demand, barriers to entry, tax considerations—all of the criteria that governed our decisions in real estate, and didn’t see any differences. So we set a goal that we would diversify our investment portfolio to be 50 percent real estate and 50 percent non–real estate by 1990.

We narrowed our universe by targeting good asset-intensive companies with bad balance sheets, a thesis similar to real estate. We liked asset-intensive investments because if the world ended, there would be something to liquidate. The low-tech manufacturing and agricultural chemical industries were perfect fits for us—the former driven by Bob with his expertise in engineering and passion for anything mechanical.

…….

I’ve spent my career trying to avoid its destructive consequences. Competition skews people’s assessments; as buyers get competitive, the demand for assets inflates pricing, often beyond reason. I jokingly tell people that competition is great—for you. Me, I’d rather have a natural monopoly, and if I can’t get that, I’ll take an oligopoly. Not long after we got involved with GAMI,

Micro Opportunities in Macro Events

As an investor, Zell has a unique way of combining macro insights with bottom up research.Several examples in the book highlight this. He was “all about seeing micro opportunities in macro events. For example:

In this case, the macro event was legislation similar to the impact of the Economic Recovery Tax Act of 1981 on NOLs. But I find implications for opportunity everywhere—in world events, economic news, and conversations. I’ve always been on the lookout for big-picture influencers and anomalies that will direct the course of industries and companies. But first-mover advantage requires conviction. While the rest of the radio industry was deliberating about what the telecom bill meant and how it would be implemented and whether it was a good change or a bad change, we moved and bought up

Zell’s abiliy to see the big picture gave him an edge in international investing. He was the first gringo in town buying real estate in a lot of the bigger emerging market stories of the past few decades:

This is our primary premise in international investing—the transformation of businesses into institutional platforms. We started in Mexico, then went to Brazil. Then to Colombia, India, and China. So far we’ve brought about thirty companies in fifteen countries along for the ride, with four IPOs. I’m drawn to emerging markets because of their built-in demand. I’ve always believed in buying into in-place demand rather than trying to create it. To me, international investing is largely a story of demography. Just look at population growth. Most of the developed countries (e.g., U.K., France, Japan, Spain, Italy) have aging populations and are ending each year with flat or negative population growth rates. For instance, we don’t spend much time looking at Western Europe. It’s Disneyland. It’s great for wine and castles and cheese, but there’s no growth there. Further, Europe has the largest population of pensioners in the world. The number of retirees who don’t work is close to double what we have in the U.S. and most of those European countries fund each year’s pensions from taxes. It begs the question, with a shrinking workforce where will that money come from? In contrast, most of the emerging markets (e.g., India, Mexico, Colombia, South Africa, Brazil) have younger populations and higher growth rates. And while growth rates across the board have fallen off a cliff opportunity there as well. In particular, we are drawn to Mexico. After the Fukushima nuclear disaster occurred in Japan in 2011, nearly every multinational executive I talked to was bemoaning the cost of delays and availabilities in exports coming out of Asia. I couldn’t help but think that companies would not want to get caught in that type of scenario again, so they would be looking for an alternative manufacturing option closer to home. The only logical place was Mexico. Also, Chinese labor costs were steadily rising and eroding the margin for U.S. companies to manufacture there. So we invested in a Mexican warehouse and logistics company to support what I believed to be a pretty good bet on future growth. Sure enough, within four years, Mexico was in a manufacturing boom with a double-digit increase in exports from Mexican factories. We continue to view opportunity on a global scale. I see international investing as a challenge of connecting multiple dots to reach a conclusion. My job has always been to identify the dots we should pay attention to as well as the incentives that will connect them—all to get maximum possible results

See also:

- One of Zell’s early breaks was buying massive amounts of apartments at the bottom of the market in the late 70s He outlined this thesis classic article : “The Grave Dancer”

- Sam Zell Looks Back

- A dozen things I’ve learned from Sam Zell

Beyond headline numbers

Everybody has access to Bloomberg and Google. Every global macro investor closely follows macro data out of every country. To gain an an edge, one must look beyond headline numbers, and find underutilized datasets.

This applies when finding countries, industries, and individual companies in which to invest. Any time you want to combine top down and bottom up insights, you need to get creative with finding the right data.

Schumpeter and Perez

Joseph Schumpeter pointed out that aggregate figures “conceal more than they reveal”.

Relations between aggregates are

“entirely inadequate to teach us anything about the nature of the processes which shape their variations, aggregative theories of the business cycle must be inadequate too…”

In Technological Revolutions and Financial Capital, ( Carlota Perez emphasizes that new technological paradigms can only be analyzed by looking closely at inner workings of an economy. Within the same country, or industry some subsectors will grow at astonishingly high rates, while others decline. Perez’s framework is valuable to analyzing times of great technological change, which is basically anytime. Examples she uses include the first British Industrial Revolution( the age of Steam and Railways, the Age of steel, electricity, and heavy engineering, age of oil, automobile and mass production.

Top line numbers such as GDP or earnings could deceive an analyst, especially when looking at a new market.

Valuation and pricing

“People living through the period of paradigm transition experience real uncertainty as to the ‘right’ price of things(including that of stocks, of course).”

Extreme jumps in productivity change relative price structures in the economy. “The change in relative price structure is radical and centrifugal. Money buying electronics and telecommunications today does not have the same value as money buying furniture or automobiles.” Therefore, looking at inflation or deflation in aggregate is deceptive. Many years after Perez’ book, this now exacerbated by the Amazon effect. To some effect this may impact valuation in some industries.

Research methods

Long term aggregate data, spanning multiple periods of technological change are senseless. This goes for GDP, corporate earnings etc. Yet disaggregated stats are rarely available(except during more stable phases), as Perez points out.

The internet has provided more opportunities to find disaggregated, unique, underutilized datasets. Often this means poking around on weird regulatory websites, and following up on footnotes to academic papers.

This process might be about to get a lot easier.

Google launched a new dataset search engine. I’m excited to see how its impact snowballs as more datasets are added. Although intended for journalists, it is likely to be a valuable tool for investors seeking differentiated alpha.

Of course that means today’s edge, will be tomorrow’s table stakes.

See also: The hard thing about finding easy things

Fistful of Lira

While packing for my redeye flight to Istanbul tonight, I remembered the last time I had travelled to Turkey around 6 years ago. After getting sort of stranded in Kazakhstan for a day, I ended up wandering back alleys of Istanbul talking to questionable people in the non-bank financial service sector.

A planning error left me with no choice but to run an experiment on the fringes of the global forex market.

At the time, I was working at an investment bank in China, but I got a week off for a some sort of Communist Party workers holiday in October. My then girlfriend now wife was a grad student in the US. We decided to meet in Turkey for a little getaway.

As I prepared for the trip I was flush with RMB(Chinese yuan), but short on dollars and Euros(1). None of the banks in Beijing I went to would directly change RMB to Turkish Lira. Plus all them had silly wide bid-ask spreads on RMB/USD or RMB/EUR transactions. No point in changing here I thought, I’ll just change once when I get to Turkey. Turns out that was a rookie mistake.

I was on the Air Astana flight from Beijing to Istanbul with a layover in Almaty, Kazakhstan. Checking in was a bit of a debacle. I had to wait in a long line behind migrant laborers who had absurdly large quantities of luggage to check, much of it in non-traditional suitcases (ie barely sealed cardboard boxes).

The guy in front of me in the line to check in was about 6 foot 4, bald, big boned, with the look of a football referee who let himself go. After some sort of commotion at the front of the line , he turned around, smiled and said in a baritone, probably Russian Accent: “Almaty airlines ,this always happens. “

The flight was delayed a few hours but it ultimately did take off. However we were late enough that I missed my connecting flight. I had a day to wait for the next flight to Istanbul.

Almaty airport wasn’t fancy, but it was no worse than many of the small airports I’ve been to around the globe. I went to a cafe to get some food.

Turns out they wouldn’t accept RMB. No problem I thought, and I walked over to the one moneychanger accessible from the terminal I was at.

Turns out they wouldn’t change RMB at all.

I went to the ATM, and it wouldn’t accept my card for some reason.

For amusement I tested if any of the shops there would take RMB. None would.

At least I got a lot of reading done passing the time with no money to entertain myself in the airport for a day. I don’t remember what the meal was on the next leg of the flight, but I remember it was quite delicious.

When I got to Istanbul, and ran into identical forex issues with shops, moneychangers, and ATMs.(2)

So I wandered the streets going into moneychangers asking to change money. Even banks with China origins wouldn’t do it. Finally one money changer looked surprised, and asked “how much,” as he motioned me over towards the other end of the counter.

I answered him, then he took out a pen and a piece of scrap paper, and started to draw a map.

It was a long journey. As I recall, I had to go to the far end of one of the subway lines, then walk for about 15 minutes. Finally I found a shop that would change RMB. But their rate was horrible so I said I’d be right back.

I finally found another one a block over with a much better rate. I was relieved to at last clutch a fistful of Lira.

The rest of the trip went smoothly. Of course those days were before Erdogan, um “changed” (3).

This time I’m going back to Istanbul, with a mix of USD and Euro I’m excited to enjoy deeply discounted falafel, and drink coffee while working from a deck on the Asia side of the bosphorus, with a perfect view of the river, and Europe on the other side. I won’t have time to explore the far ends of the subway lines since I’ll only be in Istanbul for a day. After that I’ll be going to Sofia Bulgaria and working there for a week.

…

(1)When if ever will the RMB be a global currency? I don’t know. My general view on currencies is I never make pure directional bets. I just try to avoid getting killed by sudden changes. This basically means cautious sizing of any position that is exposed to fringe markets. Smart operational decisions have real alpha implications in these areas as well I guess you can say I learned this on the streets, the hard way.

Anyways, while there is now a surplus of superficial media coverage of China’s One Belt One Road policy,few people are talking about the capital markets implications. China is basically throwing money at every country to its west all the way to Europe, with a potentially huge impact of the smaller countries. What I find interesting is that most of it is going to be financed with yuan denominated debt, not dollar denominated debt. Combined with a yuan denominated oil futures contract hitting the market, One Belt One Road will result in a lot more financial market activity in yuan rather than dollars. I would still consider yuan internationalization(and a decline in the dollars status) a bit of a long shot near term, but these recent changes make it a lot more plausible over the next decade. At the very least there will soon be a lot more funky securities denominated in yuan(many probably, ahem, distressed and deeply discounted), so it makes sense to get comfortable with custody and banking issues involving the currency.

(2) My ATM card ended up getting flagged with a security alert for suspected fraud, which I was later able to resolve.

(3) Much as been said about his more populist tendencies. I also find it amusing how non-populist policies have had unintended consequences contributing to the current crisis. For example, the government incentivized small and medium sized companies to borrow in non-Lira currencies, by loosening restrictions on loans over a threshold(IIRC, $5 million). This part of the economy is seriously hurting now. Alas there will be some fun picking in the distressed debt space before too long.

Is credit really the smart money?

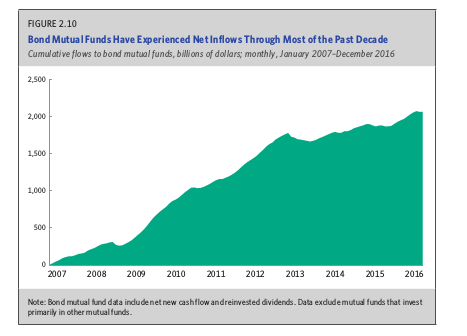

Conventional wisdom holds that credit markets are “smart institutional money” that sees problems faster than equity markets that are full of less sophisticated retail investors. I question whether that is still empirically true. Retail investors now own large portions of the credit market, including high yield. Credit markets appear to be distorted by a combination of indexation and a reach for yield. Its possible that bonds trading at par can be a false comfort signal for an equity investor looking at a highly leveraged company, because in many recent cases equity markets have been faster to react to bad news.

Retail ownership of credit markets.

However you slice and dice the data, there is clearly a lot more retail money in credit than there was a decade ago. The media mostly reports on noisy weekly or monthly flows, even though there has been a clear long term change.

Bond funds in general have experienced dramatic inflows over the past decade:

Source: ICI Fact Book 2017

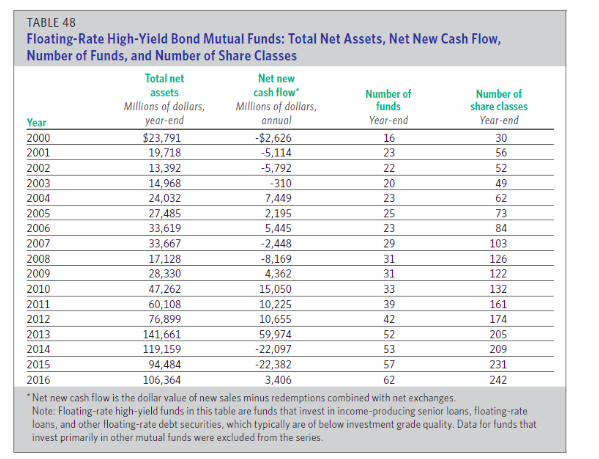

The issues becomes more serious when you look just at the high yield part of the market. Boaz Weinstein of Saba Capital estimated that between ½ or ⅓ of junk bonds are owned by retail investors in the current market. The WSJ cited Lipper data that says mutual fund ownership of high yield bonds/loans is $97 billion today vs $18 billion a decade ago. ICI slices the data differently, and comes up with a much nosier data set for just floating rate unds, indicating large outflows in 2014 and 2015. However it shows net assets in high yield bond funds up 3x compared to 2007, and the total number of funds up over 2x during that time.

Source: ICI Fact Book 2017

Its not just mutual funds either- there are now more closed end type fund structures that market towards retail investors. BDCs experienced a fundraising renaissance through 2014, and are now active in all parts of the high yield credit markets- from large syndicated loans to lower middle market. Closely related, before the last financial crisis, ago there was minimal retail ownership of CLO equity tranches, but now there are a few specialist funds, and a lot of BDCs have big chunks of it as well. Oxford Lane and Eagle Point were sort of pioneers in marketing CLO investments to retail investors but many others have followed. Interval funds are a tiny niche, but over half the funds in registration are focused on credit. It seems just about every asset manager is cooking up a direct lending strategy. The illiquid parts of the credit market are harder to quantify, but there has been a clear uptick in retail investor exposure since before the financial crisis. The marginal buyer impacting pricing is increasingly likely to be a retail investor rather than an institution.

Retail investors to exhibit more extreme herding behavior. According to Ellington Management Group:

This feedback loop between asset returns and asset flows has magnified the growth of the high yield bubble.

Capital Distortions

Its pretty easy to make a loan, its much harder to get paid back.

Trump’s foreign policy: Pulling a Homer

It is almost universally accepted that Donald Trump’s foreign policy is going to be a disaster. But what if his bizarre antics actually work? What if Trump pulls a Homer on foreign policy?

Pulling a Homer

Here’s a scenario under which Trump ends up being known as a foreign policy success. It probably won’t happen, but if it does, you heard it here first.

- The Iran protestors succeed in replacing or drastically reforming the government in Iran. The new regime remembers Trump was the first world leader to directly support them. US-Iran relations open up. Trump takes credit whether he deserves it or not.

- China and South Korea get so concerned with Trump’s impulsiveness that they finally decide to take action on North Korea. Trump takes credit whether he deserves it or not.

- Israel and Palestine come together in sort of a reverse Camp David summit as a result of Trump’s recognition of Jerusalem as the capital of Israel. Both parties are concerned with Trump’s bizarre behaviour, and finally start negotiating from realistic basis. Trump takes credit whether he deserves it or not.

- As a result ⅔ of the “Axis of Evil” is fixed through diplomatic means, and Middle East peace achieved during the Trump administration. History books go on to credit him as a highly persuasive foreign policy president. Scott Adams’ “4d Chess” analogy for Trump’s actions, however preposterous it seems now, ends up becoming the accepted narrative.

Trump Foreign Policy Compared to Nixon

Minsky and the Junk Bond Era

King of Capital: The Remarkable Rise, Fall, and Rise Again of Steve Schwarzman and Blackstone discusses the early days of the leveraged buyouts(LBOs) and junk bonds from the vantage point of Blackstone’s founders.

In 1978, KKR did an LBO of an industrial pumps make (Houdaille Industries). There had been many small LBOS of private businesses, but no one had gone that big, done a public company. A young investment banker named Steve Schwartzman heard about the deal and realized he had to get his hands on that prospectus. “He sensed something new was afoot — a way to make fantastic profits and a new outlet for his talents, a new calling.

“I read that prospectus, looked at the capital structure, and realized the returns that could be achieved.” he recalled years later. “I said to myself, ‘This is a gold mine.’ It was like a Rosetta stone for how to do leveraged buyouts. “

Speculative Bridge Financing

It quickly became apparent how lucrative leveraged buyouts could be.

LBOs were financed with Junk Bonds. The process of issuing junk bonds was messy and cumbersome. It took most banks an extremely long time to issue bonds. Drexel was so adept at hawking junks, that companies and other banks in a deal would go forward on an LBO based solely on Drexel’s assurance that it was “highly confident” it could issue bonds. Other banks that couldn’t do that would offer short term financing, aka bridge loans, so a buyer could close a deal quickly, and then issue bonds later to repay bridge loans This alowed DLK, Merril Lynch, and First Boston to compete with Drexel in the LBO financing space.

But what if the bonds couldn’t issued? How would the bridge loan be paid for?

… bridge lending was risky for banks because they could end up stuck with inventories of large and wobbly loans if the market changed direction or the company stumbled between the time the deal was signed up and the marketing of the bonds. The peril was magnified because bridge loans bre high, junk bond-like interest rates, which ratcheted up to punishing levels if borrowers failed to retire the loans on schedule. The ratchets were meant to prod bridge borrowers to refinance quickly with junk, and up until the fall of 1989, every bridge loan issued by a major investment bank had been paid. But the ratchets began to work against the banks when the credit markets turned that fall. The rates shot so high that the borrowers couldn’t afford them, an the banks found themselves stuck with loans that were headed towards default.

In the late 80s/early 90s. several junk bond deals fell through with disastrous consequences. The $6.8 billion United airlines buyout turned out poorly. Several stores ended up going bankrupt due to a failed junk bond deal: Federated Department stores , the parent of Bloomingdale’s, Abraham & Strauss, Filene’s and Lazarus, etc. etc. First Boston nearly failed due to its exposure to junk bond deals. Blackstone mostly sidestepped the worst problems of the era, but fought hard to get refinancing in some cases, and had a couple deals jeopardized.

The Minsky view of junk bonds and LBOs

The collapse of the bridge financing market in the junk bond era illustrates a key idea in Hyman Minsky’s Financial Instability Hypothesis: the idea of three types of leverage.