Category: Alternative Investments

Sam Zell: Poet laureate of contrarians and dumpster divers

Sam Zell is the patron saint of contrarians and poet laureate of dumpster divers. He has one of the best track records of any real estate or distressed asset investor, and helped pioneer the use of REITs, NOLs, and other key strategies and structures. His excellent autobiography is a valuable lens from which to understand the last 50 years of economic history.

Although he built up his reputation in off the beaten path markets, his sense of macro timing is also surreal. He loaded up on multifamily properties at the bottom of the market in the 1970s. He sold out of a large portion of his holdings near the top of the market in 2007(although that story was a bit more nuanced than I realized prior to reading the book).

Here are my notes and highlights from the book:

A full throttle opportunist

This isn’t a dress rehearsal. I try to live full throttle. I believe I was put on this earth to make a difference, and to do that I have to test my limits. I look for ways to do that every day. After all, I think it was Confucius who said, “The definition of a schmuck is someone who’s reached his goals.” It’s up to me to keep moving the end zone, and go for greatness.

….At some point the guy I was sitting next to turned to me and asked, “So what do you do?” I replied, “I’m a professional opportunist.” And that has been my response to that question ever since.

History

Zell’s Jewish parents were on one of the last trains out of Poland, just hours before the Nazi’s bombed the train tracks and took over. Many of his ancestors perished in concentration camps. His parents reminded him of this, and it appears to have had a significant impact on his world view

Did you ever wonder how the Jews allowed the Nazis to come into Poland without taking action? I asked my father that when I was little, and I’ll never forget what he said. The Jewish community in Poland at the time was extraordinarily myopic—it had little idea what was going on in the world. And it cost most of them the ultimate price. In contrast, my father’s macro understanding of world events and the conviction to act saved the lives of my family. I apply the same strategy on a much less life-and-death scale. I rely on a macro perspective to identify opportunities and make better decisions, both in my investment activity and in leading my portfolio companies. I am always questioning, always calculating the implications of broader events. How will worldwide depressed currencies affect capital flows and world trade? Does it create opportunity for international expansion among multinational companies? What real estate needs will they have? How can we get a first-mover advantage into new markets? And on and on.

Avoiding the crowd

Zell was clearly unafraid of career risk. Several times in his career he safely sat out major bubbles, and pounced later when it all burst.

The industry has a long history of overbuilding when there’s easy money, without regard for who will occupy those spaces once they’re built. At the same time that construction cranes were dotting the horizon of every major city, the country was just starting to tip into a recession. Supply was going up and prospects for demand were not good. I was certain that we were headed toward a massive oversupply and a crash was coming. That’s when I just said, “Stop.” I was done. I stopped buying assets, started accumulating capital, and got ready for what I was sure would be the greatest buying opportunity of my career thus far. My thesis was that over the next five years, we would have the opportunity to make a fortune by acquiring distressed real estate. So I established a property management firm, First Property Management Company (FPM), to focus on distressed assets. Everyone thought I was nuts. After all, occupancies were still over 90 percent. Absorption was high. Companies were hiring. It was one of many times I would hear people tell me that I just didn’t understand.

I didn’t listen. I just stepped aside while the music was still playing. It was the biggest risk I had taken to date in my career. After all, I had a stable of investors by then. What would they think if I bowed out and the end didn’t come? That would mean I was forgoing a lot of upside for them. It was a true test of my conviction. But I had to follow the logic of supply and demand. Turns out I was right. Less than one year later, in 1974, the market crashed. Hard.

Overnight, we were buying assets at 50 cents on the dollar. At the time, financial institutions did not have to mark to market. In other words, they didn’t have to adjust the book value of their assets to the current market value those assets could actually sell for. If you were an insurance company, instead of marking to market, you could avoid taking a hit

Avoiding competition

By being contrarian, Zell avoided competition.

In 1980, Bob and I sat down and listed the reasons we didn’t like where the real estate market was headed. First, the key to our prior success had been an inefficient market. The real estate industry had always been fragmented, with valuations and projections that often varied widely. That started changing rapidly with the debut of Hewlett-Packard’s financial calculator. All of a sudden, any owner could hire an MBA with an HP-12C to run ten years of cash flows, none of which considered recessions or rent dips, and make an elaborate and sophisticated case for investment—and a bunch of eager investors would show up to check out the property.

That was not an arena we wanted to compete in. Second, up until then, lenders made long-term, fixed-rate, nonrecourse loans. But as a result of inflation in the 1970s, they got scared and switched to short-term, floating-rate loans. We believed the real money in real estate came from borrowing long-term, fixed-rate debt in an inflationary scenario that ultimately depreciated the value of the loan and increased the position of the borrower. Finally, we had always looked at the tax benefits of real estate as what you got for the lack of liquidity. All of a sudden, sellers were including a value for tax benefits in their asset pricing. So we said, “If we’ve been as successful in real estate as we have been, aren’t we really just good businessmen? And if we’re good businessmen, then why wouldn’t the same principles that apply to buying real estate apply to buying anything else?” We checked the boxes—supply and demand, barriers to entry, tax considerations—all of the criteria that governed our decisions in real estate, and didn’t see any differences. So we set a goal that we would diversify our investment portfolio to be 50 percent real estate and 50 percent non–real estate by 1990.

We narrowed our universe by targeting good asset-intensive companies with bad balance sheets, a thesis similar to real estate. We liked asset-intensive investments because if the world ended, there would be something to liquidate. The low-tech manufacturing and agricultural chemical industries were perfect fits for us—the former driven by Bob with his expertise in engineering and passion for anything mechanical.

…….

I’ve spent my career trying to avoid its destructive consequences. Competition skews people’s assessments; as buyers get competitive, the demand for assets inflates pricing, often beyond reason. I jokingly tell people that competition is great—for you. Me, I’d rather have a natural monopoly, and if I can’t get that, I’ll take an oligopoly. Not long after we got involved with GAMI,

Micro Opportunities in Macro Events

As an investor, Zell has a unique way of combining macro insights with bottom up research.Several examples in the book highlight this. He was “all about seeing micro opportunities in macro events. For example:

In this case, the macro event was legislation similar to the impact of the Economic Recovery Tax Act of 1981 on NOLs. But I find implications for opportunity everywhere—in world events, economic news, and conversations. I’ve always been on the lookout for big-picture influencers and anomalies that will direct the course of industries and companies. But first-mover advantage requires conviction. While the rest of the radio industry was deliberating about what the telecom bill meant and how it would be implemented and whether it was a good change or a bad change, we moved and bought up

Zell’s abiliy to see the big picture gave him an edge in international investing. He was the first gringo in town buying real estate in a lot of the bigger emerging market stories of the past few decades:

This is our primary premise in international investing—the transformation of businesses into institutional platforms. We started in Mexico, then went to Brazil. Then to Colombia, India, and China. So far we’ve brought about thirty companies in fifteen countries along for the ride, with four IPOs. I’m drawn to emerging markets because of their built-in demand. I’ve always believed in buying into in-place demand rather than trying to create it. To me, international investing is largely a story of demography. Just look at population growth. Most of the developed countries (e.g., U.K., France, Japan, Spain, Italy) have aging populations and are ending each year with flat or negative population growth rates. For instance, we don’t spend much time looking at Western Europe. It’s Disneyland. It’s great for wine and castles and cheese, but there’s no growth there. Further, Europe has the largest population of pensioners in the world. The number of retirees who don’t work is close to double what we have in the U.S. and most of those European countries fund each year’s pensions from taxes. It begs the question, with a shrinking workforce where will that money come from? In contrast, most of the emerging markets (e.g., India, Mexico, Colombia, South Africa, Brazil) have younger populations and higher growth rates. And while growth rates across the board have fallen off a cliff opportunity there as well. In particular, we are drawn to Mexico. After the Fukushima nuclear disaster occurred in Japan in 2011, nearly every multinational executive I talked to was bemoaning the cost of delays and availabilities in exports coming out of Asia. I couldn’t help but think that companies would not want to get caught in that type of scenario again, so they would be looking for an alternative manufacturing option closer to home. The only logical place was Mexico. Also, Chinese labor costs were steadily rising and eroding the margin for U.S. companies to manufacture there. So we invested in a Mexican warehouse and logistics company to support what I believed to be a pretty good bet on future growth. Sure enough, within four years, Mexico was in a manufacturing boom with a double-digit increase in exports from Mexican factories. We continue to view opportunity on a global scale. I see international investing as a challenge of connecting multiple dots to reach a conclusion. My job has always been to identify the dots we should pay attention to as well as the incentives that will connect them—all to get maximum possible results

See also:

- One of Zell’s early breaks was buying massive amounts of apartments at the bottom of the market in the late 70s He outlined this thesis classic article : “The Grave Dancer”

- Sam Zell Looks Back

- A dozen things I’ve learned from Sam Zell

History Repeats: The Serpent on the Rock

“History Repeats. The first time as a tragedy, the second time as a farce.”

– Karl Marx(1)

There are amusing parallels between the rise and fall of the real estate private partnership market in the 1980s, the pre financial crisis tenant in common(TIC) syndication market, and the post financial crisis non-traded REIT market driven by Nick Schorsch and his AR Global empire.

Each episode involved high fee investment products designed to fulfill investor desires for yield, tax efficiency and perceived stability, while creating disproportionate benefits for intermediaries. Each episode ended badly. And the cycle repeats, again and again.

First of all, the charts tell parallel stories:

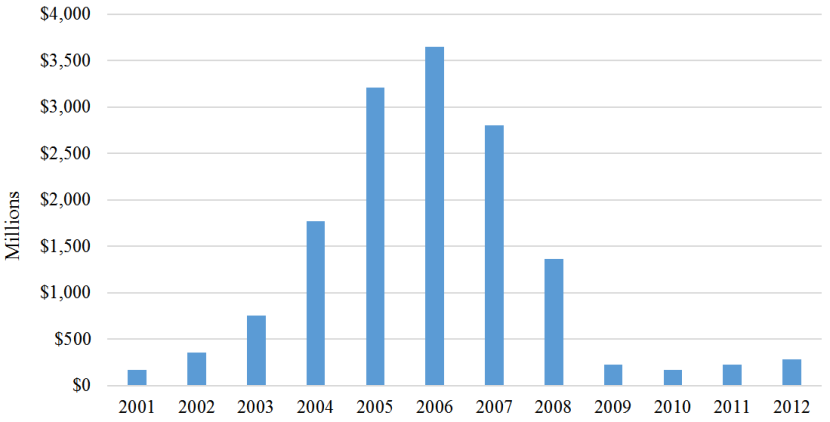

Real Estate Limited Partnerships 1970-1991

TIC Equity raised 2001-2012:

Source: Securities Litigation and Consulting Group

Non-traded REIT Equity Raise 2000-2016:

Source: Stanger Report, author’s calculations based on SEC filings.

Note that the 2015-2016 dropoff would be much sharper if you excluded Blackstone’s REIT, which entered the wirehouse channel in late 2016, and accounted for 50% of total annual NT REIT sales within a few months. Sales to the independent broker dealer(IBD) channel, which Blackstone largely bypasses, were completely decimated, and the dropoff has accelerated in 2017. (2)

May Day

High fee products are sold, not bought. The commissions on illiquid real estate products have always been higher than other investments available to retail investors.

In Serpent on the Rock Eichenwald traces the original real estate partnership craze back to the May 1, 1975 abandonment of fixed commissions on sale of stocks and bonds. Yes it is viciously ironic that commissions were fixed before 1975. The financial services industry was apparently afraid of capitalist competition and all the wonderful creative destruction it brings. Once they lost large commissions on simple security trades, they went looking through more complex higher fee product.

After May Day:

No longer could brokerage firms subsidize their bloated through fat commissions on securities trades. Firms unable to adjust collapsed by the dozens. The industry had to either dramatically cut back expenses or find new products with higher commissions that could be pumped through the sales force. Suddenly tax shelters, which sold for higher commissions than stocks and bonds didn’t look so unappealing.

The impact of May Day has continued to drive down commissions decades later. This makes sense. After all, transactional costs should approach zero over the long run, because with computers the marginal cost of doing a trade in all but the most illiquid complex markets is effectively zero. Significant scale and technological investment is necessary to run a brokerage business focused on liquid markets.

Consequently, the current IBD ecosystem is highly dependent on non-traded REITs and other high fee direct private placement programs. This is complicated by the fact that IBDs payout a high proportion of commissions to the financial advisers(like 90% in many cases). Many financial advisers built their business on 1031 exchanges, non-traded REITs or other private placements. TICs typically charged 20-30% commissions. Commissions eat up a large portion of offering proceeds for non-traded REITs. Additionally, non-traded REIT sponsors pay out a due diligence kickback to broker dealer home offices. Many smaller IBDs depend on these kickbacks for survival.

Of course, the commissions were much more egregious the first time around. Old timers fondly remember 20%+ loads on product. up front sales loads have now declined to high single digits and low double digits. Inland has driven down commissions on 1031 exchange product. Plus state securities regulators put out NASAA guidelines to limit loads on registered products. Nonetheless in an age where interactive Brokers charges $1 per side on a trade regardless of size, and few modern brokerages charge more than $7 per trade, even high single digit sales loads on non-traded retail product are absurd.

In Backstage Wall Street Josh Brown outlines his “Iron law of product compensation”:

The higher the commission or selling concession a broker is paid to sell a product, the worse that product will be for his or her clients.

This was the thread that connects the 1980s private partnership craze, with the pre financial crisis TIC explosion and the post financial crisis non-traded REIT market.

Yield Pig Exploitation and the Illusion of Safety

Just like private partnerships in the 1970s and 1980s, brokers sold TICs and Non-traded REITs to unsophisticated yield hungry retirees as safe, stable investments.

Here is one description of the private partnership market:

Many of the public offerings were promoted as a way for the small investor to participate in real estate, widely believed to be an inflation hedge, offering greater return and moderate risk as compared to stocks. The ability for an individual of modest net worth or income to invest in securitized real estate was viewed as a real benefit of public syndications.

The limited partners were sold their investments on the assumption that real estate was a safe, growing investment. Often these investors were unsophisticated in investment matters, and were more often swayed by aggressive brokerage salesmanship. The importance of liquidity became apparent to the investors only after substantial investment had already occurred. Liquidity was never promised for limited partnership securities and the partnership structure itself was designed to constrain liquidity.

In Serpent on the Rock Eichenwald meticulously tracked the juxtaposition between sales materials promising safety and the ultimate collapse in values.Non-traded REITs and TICs are also sold as safe investments that do not have the volatility of the stock market. Of course the stability is an illusion, and investors are still highly dependent on the real estate performance.

Due diligence

Eichenwald describes due diligence at Prudentialduring the peak of the private partnership craze:

The due diligence team was not just overwhelmed from the number new deals they had to approve- they also had to keep tabs on the old deals that had already been sold. Darr had negotiated for Bache to be paid a monitoring fee from some tax shelters it sold in exchange for reviewing their financial performance. Supposedly, this was designed to make sure that the general partners managing the deals did things right and took care of their investors. It was a key selling point for Bache brokers: In sales pitches, they painted a picture of top Bache financiers in green eyeshades peering over the shoulders of the General partners, watching everything that was done, The image of financial professionals crunching numbers late into the night to make sure investors were protected was a persuasive marketing tool.

But asset monitoring paid only a small fraction of the fees that Bache received from selling new deals. So the job of keeping an eye on the performance of old shelters quickly became viewed as simply a headache. It was an obligation that slowed down the whole process of churning out deals., without enough juice from fees to make up for the effort. The monitoring assignment became a hot potato, passed from executive to subordinates, and from then on down the line.

Many similar scenes in the book are shockingly familiar to anyone who has worked in the alternative investments space.

In subsequent years, third party due diligence firms serving broker dealers helped drive improvements in deal quality, but there are still many serious gaps. Since IBDs depend on the revenue from commissions and due diligence kickbacks, they are under pressure to find product to approve. This bias leads to cognitive dissonance. As non fiduciary middlemen, they often sell things that they wouldn’t invest in themselves, especially with a full sales load.

In the wake of the bankruptcy of TIC Sponsor DBSI, and the collapse of several tax driven energy deals, Reuters investigated due diligence in the independent broker dealer space. It highlighted a too cozy relationship between sponsors and third party due diligence firms.

Perhaps of even greater concern is the disconnect between due diligence process and the needs of end investors.

Potentially alarming findings are often obscured in multiple pages of recondite language, with no definitive conclusions. “They’re these long-winded things that bury things that might be important inside boilerplate disclosures,” said Jennifer Johnson, a professor at Lewis & Clark Law School in Portland, Oregon, who has written extensively about the private-placement business.

Due diligence firms say their reports aren’t designed to be read or understood by investors. Rather, they are meant to help brokers decide whether to recommend private placements to their customers.

Same Same, But Different

Although the distorted incentives,exploitation of unsophisticated yield pigs,were almost identical in each of the three historical examples in this post, there are several key differences. Broker dealers primarily sold private partnerships in the 1980s as a way of reducing taxes. An investor can use a TIC structure as part of a 1031 exchange to delay taxes when selling a property. REITS are a unique IRS creation but the reason for investing in a REIT is mainly income(Excluding situations where someone exchanges via an UPREIT transaction)

The private partnership market collapsed because the tax reform act of 1986 destroyed their entire structure, and basically collapsed the national real estate market. (see: this FDIC report )

The TIC market collapsed when the financial crisis hit the entire real estate market, exposing the problematic underwriting of the TIC Sponsors. However, regulatory issues weren’t the main driver of the collapse. Like the private partnership craze in the 1980s, the modern Non-traded REIT market also collapsed due to regulatory change although the . Finra 15-02, which increased the transparency on client statements, made it harder for advisors to get away with charging the massive sales loads. The fiduciary standard required broker-dealers to act in the best interest of clients, also led many broker-dealers to suspend or slow down the sales of high commission products.

The farce of AR Global’s collapse

Although private partnerships and TIC sponsors generally overpaid for properties they purchased, the collapse of their structures happened during a time of across the board real estate declines in the US

In contrast, investors in post financial crisis vintage non-traded REITs have suffered, in spite of a buoyant real estate market. ARC Hospitality(Now Hospitality Investors Trust) offered shares at $25.00 a share from 2013-2015, and a client statement never would have shown a value below $22.00 until this summer. It revalued at $13.20. A PE fund recently offered $5.53 for the shares. Likewise ARC Healthcare Trust III sold shares $25.00, and recently marked its value down to $17.64, and is now subject to an affiliated transaction with no liquidity event in site.

Private partnerships and TICs were tragedies, AR Global was a farce.

To be continued….

(1) This is from The Eighteenth Brumaire of Louis Napolean.

The full translated quote is :Hegel remarks somewhere that all great world-historic facts and personages appear, so to speak, twice. He forgot to add: the first time as tragedy, the second time as farce.

(2) Wirehouses generally did not sell non-traded REITs until Blackstone entered the market in 2016 Anyone who carefully read The Serpent on the Rock will note how incredibly ironic it is that wirehouses have started to sell non-traded real estate securities again. More on his in a future post.

The future of non-traded REITs

“All under heaven is in utter chaos. The situation is excellent.”

Mao Zedong (1)

Non-traded REITs, in most incarnations, have been reprehensible financial products sold by the unscrupulous to the naive. Nevertheless, they persisted. The 7% commission was just irresistible to brokers while it lasted.

Now the mess of legacy products is left for vulture investors to cleanup. Technologically advanced secondary markets will make the process a little smoother than last time. While the traditional group of Sponsors and brokers struggle to raise capital, institutional players such as Blackstone and Oaktree are launching new non-traded REITs, and finding no shortage of demand. The next generation of non-traded REITs are a major improvement over the previous generation,although the bar isn’t exactly that high.

New entrants distributing newly improved product to new distribution channels will define the future of non-traded REITs. Several large “brand name” asset managers have recently launched non-traded REITs. They are selling via wirehouses, which have generally avoided non-traded REITs for over 20 years. They’re also selling via registered investment advisers, who, as fiduciaries, previously avoided non-traded REITs. Furthermore several well known real estate firms are launching non-traded REITs or other products and selling directly to investors online, a phenomenon completely unheard of a decade ago.

Legacy non-traded REITs and secondary market

There is a massive overhang of legacy product that is preventing sales of new non-traded REITs via the independent broker dealer(IBD) channel. Post financial crisis, non-traded REIT Sponsors tried to take non-traded REITs full cycle(either via merger or IPO) after 2-4 years. This allowed financial advisers to collect the 7% commissions over and over again. Constant recycling became a critical source of income for IBDs, and an absolute bonanza for Sponsors However, after the AR Global scandal, fiduciary standard, and FINRA 15-02, the pace of new product slowed down suddenly.

Minsky and the Junk Bond Era

King of Capital: The Remarkable Rise, Fall, and Rise Again of Steve Schwarzman and Blackstone discusses the early days of the leveraged buyouts(LBOs) and junk bonds from the vantage point of Blackstone’s founders.

In 1978, KKR did an LBO of an industrial pumps make (Houdaille Industries). There had been many small LBOS of private businesses, but no one had gone that big, done a public company. A young investment banker named Steve Schwartzman heard about the deal and realized he had to get his hands on that prospectus. “He sensed something new was afoot — a way to make fantastic profits and a new outlet for his talents, a new calling.

“I read that prospectus, looked at the capital structure, and realized the returns that could be achieved.” he recalled years later. “I said to myself, ‘This is a gold mine.’ It was like a Rosetta stone for how to do leveraged buyouts. “

Speculative Bridge Financing

It quickly became apparent how lucrative leveraged buyouts could be.

LBOs were financed with Junk Bonds. The process of issuing junk bonds was messy and cumbersome. It took most banks an extremely long time to issue bonds. Drexel was so adept at hawking junks, that companies and other banks in a deal would go forward on an LBO based solely on Drexel’s assurance that it was “highly confident” it could issue bonds. Other banks that couldn’t do that would offer short term financing, aka bridge loans, so a buyer could close a deal quickly, and then issue bonds later to repay bridge loans This alowed DLK, Merril Lynch, and First Boston to compete with Drexel in the LBO financing space.

But what if the bonds couldn’t issued? How would the bridge loan be paid for?

… bridge lending was risky for banks because they could end up stuck with inventories of large and wobbly loans if the market changed direction or the company stumbled between the time the deal was signed up and the marketing of the bonds. The peril was magnified because bridge loans bre high, junk bond-like interest rates, which ratcheted up to punishing levels if borrowers failed to retire the loans on schedule. The ratchets were meant to prod bridge borrowers to refinance quickly with junk, and up until the fall of 1989, every bridge loan issued by a major investment bank had been paid. But the ratchets began to work against the banks when the credit markets turned that fall. The rates shot so high that the borrowers couldn’t afford them, an the banks found themselves stuck with loans that were headed towards default.

In the late 80s/early 90s. several junk bond deals fell through with disastrous consequences. The $6.8 billion United airlines buyout turned out poorly. Several stores ended up going bankrupt due to a failed junk bond deal: Federated Department stores , the parent of Bloomingdale’s, Abraham & Strauss, Filene’s and Lazarus, etc. etc. First Boston nearly failed due to its exposure to junk bond deals. Blackstone mostly sidestepped the worst problems of the era, but fought hard to get refinancing in some cases, and had a couple deals jeopardized.

The Minsky view of junk bonds and LBOs

The collapse of the bridge financing market in the junk bond era illustrates a key idea in Hyman Minsky’s Financial Instability Hypothesis: the idea of three types of leverage.