Tagged: Social Psychology

When is the crowd right?

Humans have flawed brains that cause them to act crazy sometimes. And in groups, people get even more crazy. Many smart people believe dumb things. Sometimes a group of otherwise completely sane people come together and do something insane. History is full of examples of the “ Extraordinary Popular Delusions and the Madness of Crowds, or Manias, Panics and Financial crisis. Humans sometimes join suicide cults. Human literally burned witches not that long ago. Groupthink is a helluva drug.

Financial markets provide an arena in which the biggest gains can be made betting against consensus. Yet statistically speaking, the consensus is usually right. The times when the crowd goes crazy are notable because they are exceptions. One must carefully decide when to be a contrarian.

Under what conditions is the consensus likely to be wrong? Lets invert the question: under what conditions is the crowd likely to be right?

Most of the time, a large group of people actually comes to a more accurate conclusion than any one individual. The success of Estimize, which crowdsources earnings estimates is one useful empirical example. “Wisdom of Crowds” is a well documented phenomenon, and well summarized in the book by the same title.

Why is the crowd so often right? What must happen for the crowd to be right ? Researchers have identified four interrelated conditions that encourage the wisdom of the crowds:Diversity, Information Availability, Decentralization, and existence of an Aggregation Mechanism.

Understanding these conditions can help one know when to follow the zeitgeist, and when to make a contrarian bet against it. A firm grasp of the facts on both sides of a controversy is necessary, but possibly not sufficient. One can never be sure of all the facts. Its also useful to understand the broader social forces, and how they influence the likelihood of the consensus being right or wrong. Searching for these conditions(or their absence), can be a useful method of avoiding cults and identifying opportunity, beyond just the facts of the individual situations.

The biggest gains are available by being a contrarian who understands the crowd.

The key is understanding when the wisdom of crowds flips to the madness of crowds. And the essential insight is that it has to do with a violation of one or more of the core conditions for a wise crowd.

Michael Mauboussin: Who is on the other side?

Diversity

Diversity implies that each person has their own point of view and some private information, even if only their unique interpretation of the available public information. Diversity is important because it adds different perspectives and increases the amount of available information.

The Value of Crowdsourcing: Evidence from Earnings Forecasts

Crowded trades have a tendency to crash- leading to no bid markets all the way down. Academics have noted that in a run up to a market crash diversity of population declines. The market becomes fragile, and eventually there is no one to buy from (or sell to).

One reason Estimize’ earnings estimates have tended to be better than Wall Street Sell side is that Estimize analysts are a diverse group of independent thinkers from around the world, holding a variety of different jobs. A lot of Wall Street analysts go to the same conferences, went to the same schools, etc.

When people come to the same conclusion from different backgrounds, logical methods, etc , their collective wisdom refines understanding of reality. The opposite occurs when people feel pressure to conform. Its important to note this is a genuine deep diversity of thought and perspective, not a superficial check the box diversity.

If multiple people with different viewpoints all come to similar conclusions, the odds of the opposite being true decrease substantially. On the other hand, if there is an obivous archetype of the thinker on the other side, then maybe a contrarian opportunity is available.

As Michael Maubossin has noted- conformity is a nonlinear process:

Scientists even have a sense of the neurobiological basis for conformity.Informational cascades occur when individuals follow the decisions of those who precede them without regard to their personal information.

Epidemiological models are useful here.

Information

The wisdom of crowds does not emerge in groups of idiots. It only applies when there is widespread access to information necessary to reach a conclusion. The extreme opposite occurs in totalitarian societies (or large corporations), where information is tightly restricted. Prior to the internet, information sometimes diffused slowly through a market, leading to massive price discrepancies obvious at even a quick quantitative glance.

Quality of input is critical to the success of crowdsource analysis:

Alternatively, it is possible that the inclusion of forecasts from certain individuals, such as Non-Professionals, may provide no value, or worse, cause the Estimize consensus to deviate further from actuals. Surowiecki (2004) states that although diversity matters, assembling a group of diverse but thoroughly uninformed people is not likely to lead to wise outcomes.

Independence

Independence is related to diversity. People need to be able to freely analyze reality and discuss opinions. Conventional wisdom is more likely to be accurate when it is freely subjected to challenge. When there are institutional or social factors that make people extremely afraid to speak truth, what everybody says to be true, may be wrong.

Children learn of this phenomenon early through the Emperor Wears No Clothes. For grown ups, see Death of Stalin for an example of lack of independence leading to morbidly hilarious results.

Independence requires relative freedom from opinions and actions of others, not complete isolation. Independence enables people to actually express their diverse information and reduces potential bias in the group decision.

Decentralization

Decentralization allows people to specialize and draw on local knowledge, without any individual or small group dictating the process.

Diversity and independence all fit in nicely with decentralization. Through specialization, decentralization encourages independence and increases the scope and diversity of information. Decentralization reduces the risk that independence and diversity will go away. Similarly having capital flows from all around the world, not just from a small group of schools or similarly thinking firms, increases the likelihood that markets become more efficient.

Existence of an Aggregation Mechanism

Finally, an aggregation mechanism is necessary to collect the individual opinions and harness the ‘wisdom-of-crowds’ effect.

This is basically why capitalism has succeeded. The price mechanism aggregates facts about supply and demand better than any bureaucracy could. At the same time, this why often the best opportunities to earn an investment profit are in illiquid asset classes where the market does not function as an aggregation mechanism to make the price close to right.

Of course, just because the market consensus is wrong, doesn’t mean that is necessarily wise to bet against it today. Must also consider reflexivity, narratives, and capital flows etc, and maintain a balance sheet that allows one to survive long periods of mass delusion.

Postscript: This is all indirectly related earlier post on finding underfollowed opportunities: The hard thing about finding easy things . This linked the ideas of both Sun Tzu and Warren Buffett. Some of the specific opportunity sets mentioned in this post have since been too widely known and we’ve moved further into more esoteric off the beaten path ideas. Nonetheless the basic principal still holds: there are more likely to be opportunities where the crowd isn’t looking.

The future of non-traded REITs

“All under heaven is in utter chaos. The situation is excellent.”

Mao Zedong (1)

Non-traded REITs, in most incarnations, have been reprehensible financial products sold by the unscrupulous to the naive. Nevertheless, they persisted. The 7% commission was just irresistible to brokers while it lasted.

Now the mess of legacy products is left for vulture investors to cleanup. Technologically advanced secondary markets will make the process a little smoother than last time. While the traditional group of Sponsors and brokers struggle to raise capital, institutional players such as Blackstone and Oaktree are launching new non-traded REITs, and finding no shortage of demand. The next generation of non-traded REITs are a major improvement over the previous generation,although the bar isn’t exactly that high.

New entrants distributing newly improved product to new distribution channels will define the future of non-traded REITs. Several large “brand name” asset managers have recently launched non-traded REITs. They are selling via wirehouses, which have generally avoided non-traded REITs for over 20 years. They’re also selling via registered investment advisers, who, as fiduciaries, previously avoided non-traded REITs. Furthermore several well known real estate firms are launching non-traded REITs or other products and selling directly to investors online, a phenomenon completely unheard of a decade ago.

Legacy non-traded REITs and secondary market

There is a massive overhang of legacy product that is preventing sales of new non-traded REITs via the independent broker dealer(IBD) channel. Post financial crisis, non-traded REIT Sponsors tried to take non-traded REITs full cycle(either via merger or IPO) after 2-4 years. This allowed financial advisers to collect the 7% commissions over and over again. Constant recycling became a critical source of income for IBDs, and an absolute bonanza for Sponsors However, after the AR Global scandal, fiduciary standard, and FINRA 15-02, the pace of new product slowed down suddenly.

FOMO is a hell of a drug

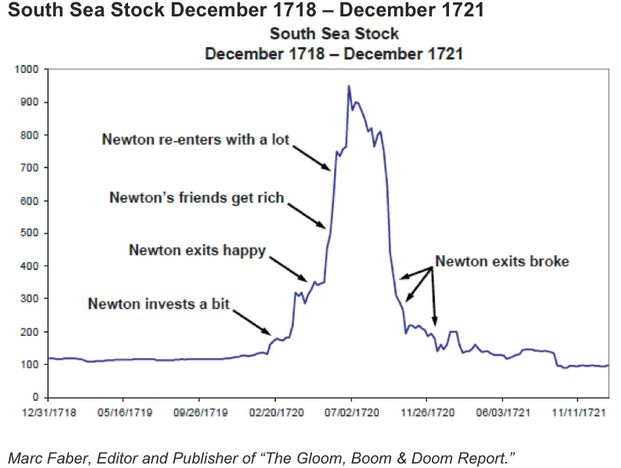

The most dangerous feeling in finance is “fear of missing out”(FOMO). FOMO causes people to make hasty emotional decisions, generally near to the top of a speculative mania. FOMO is the force behind ponzi schemes, stock promotions, and simple legit bubbles. The Stanford Business School has even looked into this

The danger of FOMO impacts people regardless of socieoeconomic status or education. It even impacted Isaac Newton:

Source: the Vantage, (which has some excellent personal finance tips on avoiding the dangers of FOMO)

Last week things got a bit volatile. Markets corrected all the way to… (wait for it) the price level of a couple months ago. This was the result of a sudden sharp reversal of record retail inflows. Although it wasn’t really an abnormal reversal, the media made it sounded like the beginning of another financial crisis.

Warren Buffett, Aesop’s Fables, and the Dot-Com Bubble

I recently went back and re-read the Berkshire Hathaway letters from during the dot-com bubble. Buffett and Charlie Munger mostly sat out the mania, then used Aesop’s Fables to explain it all when it was done. Investors can learn from their ability to maintain equanimity amidst the madness of crowds. However its also important to note that they made errors of omission as technology altered industries. Investors do themselves a disservice if they automatically reject tech investments, just because those are not areas that Berkshire Hathaway invested. Buffett’s letters to investors are a pretty good vantage point from which to understand repeating historical patterns.

1997: Maintain discipline in the mania

As the dotcom bubble started gathering momentum, Warren Buffett reaffirmed commitment to discipline:

Though we are delighted with what we own, we are not pleased with our prospects for committing incoming funds. Prices are high for both businesses and stocks. That does not mean that the prices of either will fall — we have absolutely no view on that matter — but it does mean that we get relatively little in prospective earnings when we commit fresh money.

Under these circumstances, we try to exert a Ted Williams kind of discipline. In his book The Science of Hitting, Ted explains that he carved the strike zone into 77 cells, each the size of a baseball. Swinging only at balls in his “best” cell, he knew, would allow him to bat .400; reaching for balls in his “worst” spot, the low outside corner of the strike zone, would reduce him to .230. In other words, waiting for the fat pitch would mean a trip to the Hall of Fame; swinging indiscriminately would mean a ticket to the minors.

If they are in the strike zone at all, the business “pitches” we now see are just catching the lower outside corner. If we swing, we will be locked into low returns. But if we let all of today’s balls go by, there can be no assurance that the next ones we see will be more to our liking. Perhaps the attractive prices of the past were the aberrations, not the full prices of today. Unlike Ted, we can’t be called out if we resist three pitches that are barely in the strike zone; nevertheless, just standing there, day after day, with my bat on my shoulder is not my idea of fun.

Although way too early, he started lamenting high prices:

In the summer of 1979, when equities looked cheap to me, I wrote a Forbes article entitled “You pay a very high price in the stock market for a cheery consensus.” At that time skepticism and disappointment prevailed, and my point was that investors should be glad of the fact, since pessimism drives down prices to truly attractive levels. Now, however, we have a very cheery consensus. That does not necessarily mean this is the wrong time to buy stocks: Corporate America is now earning far more money than it was just a few years ago, and in the presence of lower interest rates, every dollar of earnings becomes more valuable. Today’s price levels, though, have materially eroded the “margin of safety” that Ben Graham identified as the cornerstone of intelligent investing.

Notable Actions in 1997:

Net sales of 5% of the stock portfolio

increasing emphasis on “unconventional commitments”, including oil derivatives, and direct investments in silver.

1998: Trimming positions too early

Using Old Books to Exploit New Media

Trust Me, I’m Lying: Confessions of a Media Manipulator exposes the twisted incentive system that makes the media susceptible to manipulation, and the boiler room environment in which much of the “news” is manufactured. The book outlines tricks used to steal people’s time and attention. while serving some other agenda. By understanding the logic behind business choices that the media makes, readers can better predict and anticipate actions(some might even be able to use the book to redirect, accelerate and control stories). It was written back in 2012, but after reading, it makes sense that clickbait could help swing an election.

In the the book Ryan Holiday also hints at what gives him an intellectual edge: