Category: Books

Why its wise to think in bets

The secret is to make peace with walking around in a world where we recognize that we are not sure and that’s okay. As we learn more about how our brains operate, we recognize that we don’t perceive the world objectively. But our goal should be to try.

Annie duke’s “Thinking in Bets” is basically long essay with an extremely valuable message. Under a plethora of entertaining anecdotes about professional poker it contains a valuable framework for making decisions in this uncertain world. This requires accepting uncertainty, and being intellectually honest. Good decision making habits compound over time

Thinking in Bets is a slightly less nerdy and less nuanced compliment to pair with “Fortune’s Formula”. It also fits in well with some of the more important behavioral finance books, such as…. Misbehaving, and Hour Between wolf and dog, Kluge, etc.

I’ve organized some of my highlights and notes from Thinking in Bets below.

The implications of treating decisions as bets made it possible for me to find learning opportunities in uncertain environments. Treating decisions as bets, I discovered, helped me avoid common decision traps, learn from results in a more rational way, and keep emotions out of the process as much as possible.

Outcome quality vs decision quality

We can get better at separating outcome quality from decision quality, discover the power of saying, “I’m not sure,” learn strategies to map out the future, become less reactive decision-makers, build and sustain pods of fellow truthseekers to improve our decision process, and recruit our past and future selves to make fewer emotional decisions. I didn’t become an always-rational, emotion-free decision-maker from thinking in bets. I still made (and make) plenty of mistakes. Mistakes, emotions, losing—those things are all inevitable because we are human. The approach of thinking in bets moved me toward objectivity, accuracy, and open-mindedness. That movement compounds over time

Thinking in bets starts with recognizing that there are exactly two things that determine how our lives turn out: the quality of our decisions and luck. Learning to recognize the difference between the two is what thinking in bets is all about.

Why are we so bad at separating luck and skill? Why are we so uncomfortable knowing that results can be beyond our control? Why do we create such a strong connection between results and the quality of the decisions preceding them? How

Certainty is an illusion

Trying to force certainty onto an uncertain world is a recipe for poor decision making. To improve decision making, learn to accept uncertainty. You can always revise beliefs.

Seeking certainty helped keep us alive all this time, but it can wreak havoc on our decisions in an uncertain world. When we work backward from results to figure out why those things happened, we are susceptible to a variety of cognitive traps, like assuming causation when there is only a correlation, or cherry-picking data to confirm the narrative we prefer. We will pound a lot of square pegs into round holes to maintain the illusion of a tight relationship between our outcomes and our decisions.

There are many reasons why wrapping our arms around uncertainty and giving it a big hug will help us become better decision-makers. Here are two of them. First, “I’m not sure” is simply a more accurate representation of the world. Second, and related, when we accept that we can’t be sure, we are less likely to fall

Our lives are too short to collect enough data from our own experience to make it easy to dig down into decision quality from the small set of results we experience.

Incorporating uncertainty into the way we think about our beliefs comes with many benefits. By expressing our level of confidence in what we believe, we are shifting our approach to how we view the world. Acknowledging uncertainty is the first step in measuring and narrowing it. Incorporating uncertainty in the way we think about what we believe creates open-mindedness, moving us closer to a more objective stance toward information that disagrees with us. We are less likely to succumb to motivated reasoning since it feels better to make small adjustments in degrees of certainty instead of having to grossly downgrade from “right” to “wrong.” When confronted with new evidence, it is a very different narrative to say, “I was 58% but now I’m 46%.” That doesn’t feel nearly as bad as “I thought I was right but now I’m wrong.” Our narrative of being a knowledgeable, educated, intelligent person who holds quality opinions isn’t compromised when we use new information to calibrate our beliefs, compared with having to make a full-on reversal. This shifts us away from treating information that disagrees with us as a threat, as something we have to defend against, making us better able to truthseek. When we work toward belief calibration, we become less judgmental .

In an uncertain world, the key to improving is to revise, revise, revise.

Not much is ever certain. Samuel Arbesman’s The Half-Life of Facts is a great read about how practically every fact we’ve ever known has been subject to revision or reversal. We are in a perpetual state of learning, and that can make any prior fact obsolete. One of many examples he provides is about the extinction of the coelacanth, a fish from the Late Cretaceous period. A mass-extinction event (such as a large meteor striking the Earth, a series of volcanic eruptions, or a permanent climate shift) ended the Cretaceous period. That was the end of dinosaurs, coelacanths, and a lot of other species. In the late 1930s and independently in the mid-1950s, however, coelacanths were found alive and well. A species becoming “unextinct” is pretty common. Arbesman cites the work of a pair of biologists at the University of Queensland who made a list of all 187 species of mammals declared extinct in the last five hundred years.

Getting comfortable with this realignment, and all the good things that follow, starts with recognizing that you’ve been betting all along.

The danger of being too smart

The popular wisdom is that the smarter you are, the less susceptible you are to fake news or disinformation. After all, smart people are more likely to analyze and effectively evaluate where information is coming from, right? Part of being “smart” is being good at processing information, parsing the quality of an argument and the credibility of the source. So, intuitively, it feels like smart people should have the ability to spot motivated reasoning coming and should have more intellectual resources to fight it. Surprisingly, being smart can actually make bias worse. Let me give you a different intuitive frame: the smarter you are, the better you are at constructing a narrative .

… the more numerate people (whether pro- or anti-gun) made more mistakes interpreting the data on the emotionally charged topic than the less numerate subjects sharing those same beliefs. “This pattern of polarization . . . does not abate among high-Numeracy subjects.

It turns out the better you are with numbers, the better you are at spinning those numbers to conform to and support your beliefs. Unfortunately, this is just the way evolution built us. We are wired to protect our beliefs even when our goal is to truthseek. This is one of those instances where being smart and aware of our capacity for irrationality alone doesn’t help us refrain from biased reasoning. As with visual illusions, we can’t make our minds work differently than they do no matter how smart we are. Just as we can’t unsee an illusion, intellect or willpower alone can’t make us resist motivated reasoning.

The Learning Loop

Thinking rationally is a lot about revising, and refuting beliefs(link to reflexivity) By going through a learning loop faster we are able to get an advantage. This is similar to John Boyd’s concept of an OODA loop.

We have the opportunity to learn from the way the future unfolds to improve our beliefs and decisions going forward. The more evidence we get from experience, the less uncertainty we have about our beliefs and choices. Actively using outcomes to examine our beliefs and bets closes the feedback loop, reducing uncertainty. This is the heavy lifting of how we learn.

Chalk up an outcome to skill, and we take credit for the result. Chalk up an outcome to luck, and it wasn’t in our control. For any outcome, we are faced with this initial sorting decision. That decision is a bet on whether the outcome belongs in the “luck” bucket or the “skill” bucket. This is where Nick the Greek went wrong. We can update the learning loop to represent this like so: Think about this like we are an outfielder catching a fly ball with runners on base. Fielders have to make in-the-moment game decisions about where to throw the ball.

Key message: How poker players adjust their play from experience determines how much they succeed. This applies ot any competitive endeavor in an uncertain world.

Intellectual Honesty

The best players analyze their performance with extreme intellectual honesty. This means if they win, they may end up being more focused on erros they made, as told in this anecdote:

In 2004, my brother provided televised final-table commentary for a tournament in which Phil Ivey smoked a star-studded final table. After his win, the two of them went to a restaurant for dinner, during which Ivey deconstructed every potential playing error he thought he might have made on the way to victory, asking my brother’s opinion about each strategic decision. A more run-of-the-mill player might have spent the time talking about how great they played, relishing the victory. Not Ivey. For him, the opportunity to learn from his mistakes was much more important than treating that dinner as a self-satisfying celebration. He earned a half-million dollars and won a lengthy poker tournament over world-class competition, but all he wanted to do was discuss with a fellow pro where he might have made better decisions. I heard an identical story secondhand about Ivey at another otherwise celebratory dinner following one of his now ten World Series of Poker victories. Again, from what I understand, he spent the evening discussing in intricate detail with some other pros the points in hands where he could have made better decisions. Phil Ivey, clearly, has different habits than most poker players—and most people in any endeavor—in how he fields his outcomes. Habits operate in a neurological loop consisting of three parts: the cue, the routine, and the reward. A habit could involve eating cookies: the cue might be hunger, the routine going to the pantry and grabbing a cookie, and the reward a sugar high. Or, in poker, the cue might be winning a hand, the routine taking credit for it, the reward a boost to our ego. Charles Duhigg, in The Power of Habit, offers the golden rule of habit change….

Being in an environment where the challenge of a bet is always looming works to reduce motivated reasoning. Such an environment changes the frame through which we view disconfirming information, reinforcing the frame change that our truthseeking group rewards. Evidence that might contradict a belief we hold is no longer viewed through as hurtful a frame. Rather, it is viewed as helpful because it can improve our chances of making a better bet. And winning a bet triggers a reinforcing positive update.

Note: Intellectual Honesty thinking clearly= thinking in bets

Good decisions compound

One useful model is to view everything as one big long poker game. Therefore the result of individual games won’t upset you so much. Furthermore, good decision making habits compound over time. So the key is to always be developing good long term habits, even as you deal with the challenges of a specific game.

The best poker players develop practical ways to incorporate their long-term strategic goals into their in-the-moment decisions. The rest of this chapter is devoted to many of these strategies designed to recruit past- and future-us to help with all the execution decisions we have to make to reach our long-term goals. As with all the strategies in this book, we must recognize that no strategy can turn us into perfectly rational actors. In addition, we can make the best possible decisions and still not get the result we want. Improving decision quality is about increasing our chances of good outcomes, not guaranteeing them. Even when that effort makes a small difference—more rational thinking and fewer emotional decisions, translated into an increased probability of better outcomes—it can have a significant impact on how our lives turn out. Good results compound. Good processes become habits, and make possible future calibration and improvement.

At the very beginning of my poker career, I heard an aphorism from some of the legends of the profession: “It’s all just one long poker game.” That aphorism is a reminder to take the long view, especially when something big happened in the last half hour, or the previous hand—or when we get a flat tire. Once we learn specific ways to recruit past and future versions of us to remind ourselves of this, we can keep the most recent upticks and downticks in their proper perspective. When we take the long view, we’re going to think in a more rational way.

Life, like poker, is one long game, and there are going to be a lot of losses, even after making the best possible bets. We are going to do better, and be happier, if we start by recognizing that we’ll never be sure of the future. That changes our task from trying to be right every time, an impossible job, to navigating our way through the uncertainty by calibrating our beliefs to move toward, little by little, a more accurate and objective representation of the world. With strategic foresight and perspective, that’s manageable work. If we keep learning and calibrating, we might even get good at it.

Hierarchies vs networks: Notes on the Square and the Tower

“Often the biggest changes in history are the achievements of thinly documented, informally organized groups of people. “

The Square and the Tower examines the role informal networks have played throughout history. Its one of the few books I’ve seen that takes a rigorous, empirical and non-sensational look at what secret societies actually did throughout history. More importantly it delineates between societies/institutions that are driven by informal networks, vs those that are driven by formal hierarchies. The world kind of goes back and forth between the two over time. The spread of diseases and ideas follow similar processes and are both are heavily influenced by the role of networks and hierarchies in society. Among its most useful(and amusing) conclusions is that Martin Luther and Donald Trump have something very important in common.

Historical Background

The first ‘networked era’ followed the introduction of the printing press to Europe in the late fifteenth century and lasted until the end of the eighteenth century. The second – our own time – dates from the 1970s, though I argue that the technological revolution we associate with Silicon Valley was more a consequence than a cause of a crisis of hierarchical institutions. The intervening period, from the late 1790s until the late 1960s, saw the opposite trend: hierarchical institutions re-established their control and successfully shut down or co-opted networks. The zenith of hierarchically organized power was in fact the mid-twentieth century – the era of totalitarian regimes and total war.

Martin Luther and Donald Trump

The key insight is that Martin Luther and Donald Trump and their respective suorters both made highly skilld and aggressive use of a new communication medium to spread their message. Luther had ht ebrand new thing called the printing press. Trump had this brand new thing called social media(mainly twitter)

Without Gutenberg, Luther might well have become just another heretic whom the Church burned at the stake, like Jan Hus. His original ninety-five theses, primarily a critique of corrupt practices such as the sale of indulgences, were originally sent as a letter to the Archbishop of Mainz on 31 October 1517. It is not wholly clear if Luther also nailed a copy of them to the door of All Saints’ Church, Wittenberg, but it scarcely matters. That mode of publishing had been superseded. Within months, versions of the original Latin text had been printed in Basel, Leipzig and Nuremberg. By the time Luther was officially condemned as a heretic by the Edict of Worms in 1521, his writings were all over German-speaking Europe. Working with the artist Lucas Cranach and the goldsmith Christian Döring, Luther revolutionized not only Western Christianity but also communication itself. In the sixteenth century German printers produced almost 5,000 editions of Luther’s works, to which can be added a further 3,000 if one includes other projects he was involved with, such as the Luther Bible. Of these 4,790 editions, almost 80 per cent were in German, as opposed to Latin, the international language of the clerical elite.3 Printing was crucial to the Reformation’s success. Cities with at least one printing press in 1500 were significantly more likely to adopt Protestantism than cities without printing, but it was cities with multiple competing

Likewise, Trump was able to get an enormous amount of massive publicity do to his exploitation of social media. It also didn’t hurt that their were highly skilled foreign actors also using social media to spread his influence. Much of this was done in an automated fashion, using bots, etc. Social media allowed this message to spread directly without any filter from media gatekeepers.

Gutenberg’s printing press helped make Lutheranism. Twitter bots helped make Trumpism.

Difficult to suppress

Why was Protestantism so resistant to repression? One answer to that question is that, as they proliferated throughout northern Europe, the Protestant sects developed impressively resilient network structures.

Similarly, traditional political operatives have had difficulty penetrating the social media networks that Trump has so successfully exploited.

Bringing the medium to the masses

Just as the printing press caused a drastic fall in the price of written books, the falling prices of phones and PCs made the internet more widely accessible.

The decline in the price of a PC between 1977 and 2004 followed a very similar trajectory to the decline in the price of a book between the 1490s and the 1630s. Yet the earlier, slower revolution in information technology appears to have had the larger economic impact. The best explanation for this difference is the role of printing in disseminating hitherto unavailable knowledge fundamental to the functioning of a modern economy. The first known printed mathematics text was the Treviso Arithmetic (1478). In 1494, Luca Pacioli’s Summa de arithmetica, geometria, proportioni et proportionalita was published in Venice, extolling the benefits of double-entry book-keeping.

Luther and Trump both spread their message just as new technology was making it much easier for something to go viral. Luther upended the church hierarchy by bringing religious texts and thoughts to the common people. Prior to Luther religious text were almost exclusively in Latin, which the common people could not read or understand. The idea that common people could be allowed to read the bible was considered heretical (see a world lit only by fire). Luther spread his messages into far away villages causing the Catholic church to lose control of its traditional followers. Likewise, Trump upended the political hierarchy by spreading a populist message far and wide, even overtaking previously Democratic strongholds. Many people who felt abandoned by the political process went to his rallies. Washington insiders have been thrown out, an outsiders have taken control. Many readers of this blog may not want to think of Trump in this way, but the analogy is valuable in understanding why Trump has been so successful.

Spread of disease

The speed with which an infectious disease spreads has as much to do with the network structure of the exposed population as with the virulence of the disease itself, as an epidemic amongst teenagers in Rockdale County, Georgia, made clear twenty years ago. The existence of a few highly connected hubs causes the spread of the disease to increase exponentially after an initial phase of slow growth.7 Put differently, if the ‘basic reproduction number’ (how many other people are newly infected by a typical infected individual) is above one, then a disease becomes endemic;

Impact on economics

For economists, too, advances in network science had important implications. Standard economics had imagined more or less undifferentiated markets populated by individual utility-maximizing agents with perfect information. The problem – resolved by the English economist Ronald Coase, who explained the importance of transaction costs* – was to explain why firms existed at all. (We are not all longshoremen, hired and paid by the day like Marlon Brando in On the Waterfront, because employing us regularly within firms can reduce the costs that arise when workers are hired on a daily basis.) But if markets were networks, with most people inhabiting more or less interconnected clusters, the economic world looked very different, not least because information flows were determined by the networks’ structures. Many exchanges are not just one-off transactions in which price is a matter of supply and demand. Credit is a function of trust, which in turn is higher within a cluster of similar people (e.g. an immigrant community). This has implications not only for employment markets, the case studied by Granovetter. Closed networks of sellers can collude against the public and deter innovation. More open networks can promote innovation as new ideas reach the cluster thanks to the strength of weak ties. Such observations prompted the question of

Spread of ideas

The key point, as with disease epidemics, is that network structure can be as important as the idea itself in determining the speed and extent of diffusion. In the process of going viral, a key role is played by nodes that are not merely hubs or brokers but ‘gate-keepers’ – people who decide whether or not to pass information to their part of the network. Their decision will be based partly on how they think that information will reflect back on them. Acceptance of an idea, in turn, can require it to be transmitted by more than one or two sources. A complex cultural contagion, unlike a simple disease epidemic, first needs to attain a critical mass of early adopters with high degree centrality (relatively large numbers of influential friends).In the words of Duncan Watts, the key to assessing the likelihood of a contagion-like cascade is ‘to focus not on the stimulus itself but on the structure of the network the stimulus hits’. This helps explain why, for every idea that goes viral, there are countless others that fizzle out in obscurity because they began with the wrong node, cluster or network.

…

That is because so many real-world networks follow Pareto-like distributions: that is, they have more nodes with a very large number of edges and more nodes with very few than would be the case in a random network. This is a version of what the sociologist Robert K. Merton called ‘the Matthew effect’, after the Gospel of St Matthew: ‘For unto every one that hath shall be given, and he shall have abundance: but from him that hath not shall be taken away even that which he hath.’* In science, success breeds success: to him who already has prizes, more prizes shall be given. Something similar can be seen in ‘the economics of superstars’. In the same way, as many large networks

Just like the printing press destroyed the ruling classes monopoly on spirituality, social media has destroyed the “establishment’s” monopoly on political ideology.

Martin Luther and Donald Trump would agree on this

The value of improvisation and informal processes

Seeing Like a State: How Certain Schemes to Improve the Human Condition Have Failed summarizes the key dangers of centrally managed social engineering projects. Its a bit dense, but well worth it. It shows similarities between many seemingly different disasters caused by top-down control and central planning. Case studies include modernist architecture, Soviet collectivization, herding or rural people into villages in Africa,and early errors in scientific agriculture, etc.

Anyone trying to build and manage an organization needs to be aware of the lessons in this book.

One key lesson is that practical knowledge, informal processes, and improvisation in the face of unpredictability are indispensable.

Formal scheme was parasitic on informal processes that alone, it could not create or maintain. The the degree that the formal scheme made no allowance for those processes or actually suppressed them, it failed both its intended beneficiaries and ultimately its designers as well. “

Radically simplified designs for social organization seem to court the same risks of failure courted by radically simplified designs for natural environments.

It makes the case for resilience of both social and natural diversity, and a strong case for limits about what can be known about complex social order. Avoid reductive social science.

Four elements of centrally planned disasters

According to the book, there four elements necessary for a full fledged disaster to be caused by state initiated social engineering.

- Administrative ordering of nature and society

- “High Modernist Ideology” a faith that borrowed the legitimacy of science and technology. Uncritical unskeptical public and therefore unscientific optimism about possibilities for comprehensive planning of human settlement and production. Often with aesthetic terms too.

- Authoritarian state willing to use the full weight of its coercive power for #2

- Prostrate civil society lacking capacity to resist these plans.

“By themselves they are unremarkable tools of modern statecraft; they are as vital to the maintenance of our welfare and freedom as they are to the designs of a would be modern despot. They undergird the concept of citizenship and the provision of social welfare just as they might undergird a policy of rounding up undesirable minorities.”

Overlooking ecology

The discussion of the ecological disasters caused by forestry regulation in 18th and 19th century Germany is instructive:

The metaphorical value of this brief account of scientific production forestry is that it illustrates the dangers of dismembering an exceptionally complex and poorly understood set of relations and processes in order to isolate a single element of instrumental value. The instrument, the knife, that carved out the new, rudimentary forest was the razor sharp interest in the production of a single commodity. Everything that interfered with the efficient production of the key commodity was implacably eliminated. Everything that seemed unrelated to efficient production was ignored. Having come to see the forest as a commodity, scientific forestry set about refashioning it as a commodity machine. Utilitarian simplification in the forest was an effective way of maximizing wood production in the short and intermediate term. Ultimately, however, its emphasis on yield and paper profits, its relatively short time horizon, and , above all, the vast array of consequences it had resoloutley bracketed came back to haunt it.

Department of unintended consequences

I like to joke about wanting to start a department of unintended consequences to oversee economic policy. Often central planners fail because they arrograntly fail to foresee unintended consequences of their policies.

“ the door and window tax established in France under the directory and abolished only in 1917 is a striking case in point. Its originator must have reasoned that the number of windows and doors in a dwelling was proportional to the dwelling a size. Thus a tax assessor need not enter the house or measure it but merely count the doors and windows. As a simple, workable formula, it was a brilliant stroke, but it was not without consequences. Peasant dwellings were subsequently designed or renovated with the formula in mind so as to have as few openings as possible. While the fiscal losses could be recouped by raising the tax per opening, the long-term effects on the health of the rural population lasted for more than a century. “

See also: Goodhart’s Law

Carl Icahn: Capitalist Kingpin

Carl Icahn is one of my favorite capitalists. For all his flaws, his glory days were epic. He shook up the corporate aristocracy, and created massive value for his early financial backers. The economy has benefited from the disruption of complacency led by corporate raiders like Icahn.

Carl Icahn’s bio covers the evolution of his takeover style and thought process. It pairs well with Tobias Carlisle’s work, including The Acquirer’s Multiple, and Deep Value.

Below are some of my notes from Icahn’s bio:

The importance of philosophy

Icahn studied philosophy in college. This proved useful in understanding markets and navigating high stakes situations. He focused on the concept of empiricism.

Empiricism says knowledge is based on observation and experience, not feelings,” Icahn said. “In a funny way, studying twentieth-century philosophy trains your mind for takeovers. “. . There’s a strategy behind everything. Everything fits. Thinking this way taught me to compete in many things, not only takeovers but chess and arbitrage.

….It seems to me that the quest for an explication of the empiricist meaning criterion, as it has progressed, may be likened to the tale of the city that suddenly finds itself in possession of a great homogeneous mixture of gold and sand. If the gold could be separated from the sand it would prove a great deal more valuable to the inhabitants. The wise men of the city diligently search for a method of separation. By so doing they not only vastly increase their insight into the nature of gold, sand, homogeneous mixtures, etc., but also produce a series of increasingly potent methods of separating the chaff from the gold, the meaningless from the significant.”

Waiting for the right opportunity to pounce

He waits until someone is so stretched out and in need of a deal that he can come in and buy under the most favorable terms.

From the PPM/pitchbook for Icahn’s first fund:

It is our opinion that the elements in today’s economic environment have combined in a unique way to create large profit-making opportunities with relatively little risk. Our nation’s huge need for energy has resulted in a massive flow of dollars abroad. This, coupled with huge deficit spending and decreasing productivity, has caused a high inflation rate and a sharply declining dollar. As a result, the value of gold and goods in general has skyrocketed. An obvious corollary to this is that the real or liquidating value of many American companies has increased markedly in the last few years; however, interestingly, this has not at all been reflected in the market value of their common stocks. Thus we are faced with a unique set of circumstances that, if dealt with correctly, can lead to large profits…

Non linear thinking

Like most great investors, Icahn is a non-linear thinker.

In part, his success is based on an intellectual skill that enables him to plot dozens of moves in advance. While his adversaries are thinking in linear fashion—”If I can get from A to B, then I’ll proceed to C”—Icahn sees dozens of possibilities on a single screen. The mental agility that enables him to zigzag from C to F to Z and back to R, leaves his opponents so thoroughly confused and frustrated they are on the verge of shorting out. “In trying to beat Carl, and failing to do so, people come away baffled,” said Brain Freeman. “But I can tell them why they fail. Because they think they know what Carl’s goal is when in fact he has no fixed goal.

Expanding options

Presented with an ultimatum in which he is told to choose between evil A or lesser evil B, Icahn moves into intellectual overdrive, expanding the range of options. In this way, he turns the tables on his adversaries, who find themselves facing a more ominous threat than they hurled at the raider.

Limitations of Icahn’s approach

Icahn was a great liquidator, a great investor in asset intensive businesses, but sticking too closely to his methods would cause a modern investor to miss great opportunities to invest in rapidly growing businesses. Additionally, based on the performance of IEP, its possible that he has failed to adapt to recent technological disruption, and the age of asset lite businesses.

Carl is a smart Neanderthal,” said Marty Whitman. “He’s a Neanderthal because he doesn’t listen. He has fixed ideas. He doesn’t see that you can’t make money by investing in a business. He only wants to cash out—to get cash flow. He doesn’t understand that most of the great businesses built in this country were cash consumers. They used public markets and consumed cash to build fabulous wealth for their owners. But Carl just wants the cash-out approach.

As with most corporate titans, sometimes his ego gets the best of him. He nearly went bankrupt messing around with airlines, for example. Nonetheless his story is valuable and entertaining, and he wrote the playbook for many situations faced by investors today.

See also:

The Next Level of Shareholder Activism

Sam Zell: Poet laureate of contrarians and dumpster divers

Sam Zell is the patron saint of contrarians and poet laureate of dumpster divers. He has one of the best track records of any real estate or distressed asset investor, and helped pioneer the use of REITs, NOLs, and other key strategies and structures. His excellent autobiography is a valuable lens from which to understand the last 50 years of economic history.

Although he built up his reputation in off the beaten path markets, his sense of macro timing is also surreal. He loaded up on multifamily properties at the bottom of the market in the 1970s. He sold out of a large portion of his holdings near the top of the market in 2007(although that story was a bit more nuanced than I realized prior to reading the book).

Here are my notes and highlights from the book:

A full throttle opportunist

This isn’t a dress rehearsal. I try to live full throttle. I believe I was put on this earth to make a difference, and to do that I have to test my limits. I look for ways to do that every day. After all, I think it was Confucius who said, “The definition of a schmuck is someone who’s reached his goals.” It’s up to me to keep moving the end zone, and go for greatness.

….At some point the guy I was sitting next to turned to me and asked, “So what do you do?” I replied, “I’m a professional opportunist.” And that has been my response to that question ever since.

History

Zell’s Jewish parents were on one of the last trains out of Poland, just hours before the Nazi’s bombed the train tracks and took over. Many of his ancestors perished in concentration camps. His parents reminded him of this, and it appears to have had a significant impact on his world view

Did you ever wonder how the Jews allowed the Nazis to come into Poland without taking action? I asked my father that when I was little, and I’ll never forget what he said. The Jewish community in Poland at the time was extraordinarily myopic—it had little idea what was going on in the world. And it cost most of them the ultimate price. In contrast, my father’s macro understanding of world events and the conviction to act saved the lives of my family. I apply the same strategy on a much less life-and-death scale. I rely on a macro perspective to identify opportunities and make better decisions, both in my investment activity and in leading my portfolio companies. I am always questioning, always calculating the implications of broader events. How will worldwide depressed currencies affect capital flows and world trade? Does it create opportunity for international expansion among multinational companies? What real estate needs will they have? How can we get a first-mover advantage into new markets? And on and on.

Avoiding the crowd

Zell was clearly unafraid of career risk. Several times in his career he safely sat out major bubbles, and pounced later when it all burst.

The industry has a long history of overbuilding when there’s easy money, without regard for who will occupy those spaces once they’re built. At the same time that construction cranes were dotting the horizon of every major city, the country was just starting to tip into a recession. Supply was going up and prospects for demand were not good. I was certain that we were headed toward a massive oversupply and a crash was coming. That’s when I just said, “Stop.” I was done. I stopped buying assets, started accumulating capital, and got ready for what I was sure would be the greatest buying opportunity of my career thus far. My thesis was that over the next five years, we would have the opportunity to make a fortune by acquiring distressed real estate. So I established a property management firm, First Property Management Company (FPM), to focus on distressed assets. Everyone thought I was nuts. After all, occupancies were still over 90 percent. Absorption was high. Companies were hiring. It was one of many times I would hear people tell me that I just didn’t understand.

I didn’t listen. I just stepped aside while the music was still playing. It was the biggest risk I had taken to date in my career. After all, I had a stable of investors by then. What would they think if I bowed out and the end didn’t come? That would mean I was forgoing a lot of upside for them. It was a true test of my conviction. But I had to follow the logic of supply and demand. Turns out I was right. Less than one year later, in 1974, the market crashed. Hard.

Overnight, we were buying assets at 50 cents on the dollar. At the time, financial institutions did not have to mark to market. In other words, they didn’t have to adjust the book value of their assets to the current market value those assets could actually sell for. If you were an insurance company, instead of marking to market, you could avoid taking a hit

Avoiding competition

By being contrarian, Zell avoided competition.

In 1980, Bob and I sat down and listed the reasons we didn’t like where the real estate market was headed. First, the key to our prior success had been an inefficient market. The real estate industry had always been fragmented, with valuations and projections that often varied widely. That started changing rapidly with the debut of Hewlett-Packard’s financial calculator. All of a sudden, any owner could hire an MBA with an HP-12C to run ten years of cash flows, none of which considered recessions or rent dips, and make an elaborate and sophisticated case for investment—and a bunch of eager investors would show up to check out the property.

That was not an arena we wanted to compete in. Second, up until then, lenders made long-term, fixed-rate, nonrecourse loans. But as a result of inflation in the 1970s, they got scared and switched to short-term, floating-rate loans. We believed the real money in real estate came from borrowing long-term, fixed-rate debt in an inflationary scenario that ultimately depreciated the value of the loan and increased the position of the borrower. Finally, we had always looked at the tax benefits of real estate as what you got for the lack of liquidity. All of a sudden, sellers were including a value for tax benefits in their asset pricing. So we said, “If we’ve been as successful in real estate as we have been, aren’t we really just good businessmen? And if we’re good businessmen, then why wouldn’t the same principles that apply to buying real estate apply to buying anything else?” We checked the boxes—supply and demand, barriers to entry, tax considerations—all of the criteria that governed our decisions in real estate, and didn’t see any differences. So we set a goal that we would diversify our investment portfolio to be 50 percent real estate and 50 percent non–real estate by 1990.

We narrowed our universe by targeting good asset-intensive companies with bad balance sheets, a thesis similar to real estate. We liked asset-intensive investments because if the world ended, there would be something to liquidate. The low-tech manufacturing and agricultural chemical industries were perfect fits for us—the former driven by Bob with his expertise in engineering and passion for anything mechanical.

…….

I’ve spent my career trying to avoid its destructive consequences. Competition skews people’s assessments; as buyers get competitive, the demand for assets inflates pricing, often beyond reason. I jokingly tell people that competition is great—for you. Me, I’d rather have a natural monopoly, and if I can’t get that, I’ll take an oligopoly. Not long after we got involved with GAMI,

Micro Opportunities in Macro Events

As an investor, Zell has a unique way of combining macro insights with bottom up research.Several examples in the book highlight this. He was “all about seeing micro opportunities in macro events. For example:

In this case, the macro event was legislation similar to the impact of the Economic Recovery Tax Act of 1981 on NOLs. But I find implications for opportunity everywhere—in world events, economic news, and conversations. I’ve always been on the lookout for big-picture influencers and anomalies that will direct the course of industries and companies. But first-mover advantage requires conviction. While the rest of the radio industry was deliberating about what the telecom bill meant and how it would be implemented and whether it was a good change or a bad change, we moved and bought up

Zell’s abiliy to see the big picture gave him an edge in international investing. He was the first gringo in town buying real estate in a lot of the bigger emerging market stories of the past few decades:

This is our primary premise in international investing—the transformation of businesses into institutional platforms. We started in Mexico, then went to Brazil. Then to Colombia, India, and China. So far we’ve brought about thirty companies in fifteen countries along for the ride, with four IPOs. I’m drawn to emerging markets because of their built-in demand. I’ve always believed in buying into in-place demand rather than trying to create it. To me, international investing is largely a story of demography. Just look at population growth. Most of the developed countries (e.g., U.K., France, Japan, Spain, Italy) have aging populations and are ending each year with flat or negative population growth rates. For instance, we don’t spend much time looking at Western Europe. It’s Disneyland. It’s great for wine and castles and cheese, but there’s no growth there. Further, Europe has the largest population of pensioners in the world. The number of retirees who don’t work is close to double what we have in the U.S. and most of those European countries fund each year’s pensions from taxes. It begs the question, with a shrinking workforce where will that money come from? In contrast, most of the emerging markets (e.g., India, Mexico, Colombia, South Africa, Brazil) have younger populations and higher growth rates. And while growth rates across the board have fallen off a cliff opportunity there as well. In particular, we are drawn to Mexico. After the Fukushima nuclear disaster occurred in Japan in 2011, nearly every multinational executive I talked to was bemoaning the cost of delays and availabilities in exports coming out of Asia. I couldn’t help but think that companies would not want to get caught in that type of scenario again, so they would be looking for an alternative manufacturing option closer to home. The only logical place was Mexico. Also, Chinese labor costs were steadily rising and eroding the margin for U.S. companies to manufacture there. So we invested in a Mexican warehouse and logistics company to support what I believed to be a pretty good bet on future growth. Sure enough, within four years, Mexico was in a manufacturing boom with a double-digit increase in exports from Mexican factories. We continue to view opportunity on a global scale. I see international investing as a challenge of connecting multiple dots to reach a conclusion. My job has always been to identify the dots we should pay attention to as well as the incentives that will connect them—all to get maximum possible results

See also:

- One of Zell’s early breaks was buying massive amounts of apartments at the bottom of the market in the late 70s He outlined this thesis classic article : “The Grave Dancer”

- Sam Zell Looks Back

- A dozen things I’ve learned from Sam Zell

Biology and risk taking

Cleaning more book notes out of my Google Drive files…

Hour Between Dog and Wolf is a useful complement to Misbehaving and Thinking Fast and Slow. The author started out as a derivatives trader, then changed their career to neuroscience bringing unique personal perspective to the well worn path of studying how humans can act irrationality in financial markets and life.

Thinking Fast and Slow is a somewhat pendantic and rambling summary of groundbreaking research. Misbehaving is a humorous summary of the development of behavioral economics. Hour Between Dog and Wolf is a more personal story, with emphasis on dealing with risk and stress. All three are worth reading.

Written on the temple of Delphi was the maxim “know thyself” and today that increasingly knowing your biochemistry.

Brain-Body Connection

Probably the most valuable part of the book is a discussion of mind-body connection in the context of dealing with risk.

Category divide between body and mind, runs deep in western philosophy. This idea:

originated with Pythagoras, who needed the idea of immortal soul for his doctrine of reincarnation, but the idea of a mind-body split awas cast in its most durable form by Plato, who claimed that within our decaying flesh there flickers a spark of divinity, being an eternal and rational soul. The idea was subsequently taken up by St. Paul and enthroned as Christian dogma. It was a very edict also enthroned as a philosophical conundrum later known as the mind-body problem; and physicists such as Rene Descartes, a devout Catholic and committed scientist, wrestled with the problem of how this disembodied mind could interact with the physical body, eventually coming up with the memorable image of a ghost in a machine, watching and giving orders.

Today Platonic dualism as the doctrine is called is widely disputed within philosophy and mostly ignored in neuroscience, but there is one unlikely place where a vision of the rational mind and pure as anything contemplated by Plato or Descartes still lingers- and that is in economics.

Author argues that this platonic dualism has impaired ability to understand financial markets. Need to study how people react to volatile markets. For too long people have ignored brain body feedback.

Book goes on to discuss crazy behavior of traders, bankers, and the idiotic decision they made. Not original, but well worth reading, and the author puts a unique spin on it.

A couple other related ideas:

- Neocortex gave us reading, writing philosophy. Making tools throwing spears etc.

- Another brain region outgrew neocortex- cerebellum like a separate brain acting as operating system for rest of brain.

We may be gifted with considerable rational powers, but to solve a problem with them we must first be able to narrow down the potentially limitless amount of information, options and consequences. We face a tricky problem of limiting our search and to solve it we rely on emotions and gut feelings.

See also- Cialdini’s Law of Data Smog.

“Somatic Market Hypothesis”

Each event we store in memory comes bookmarked with the bodily sensations…. Called somatic markets we felt at time of living through it at our first time, and these help us decide what to do when we find ourselves in similar situations. These bookmarkers basically help us sort through options. Somatic markers help rational brain function.

Moving towards stress adaptation

Some scientists study stress and response too it. Chronic stress leads to illness, learned helplessness. Short lived bursts of stress, in contrast, cause people to emerge hardier. Can be verified with lab rats. Well known for anyone building muscle mass or aerobic capacity.

Humans are built to move, so we should. The more research emerges on physical exercise, the more we find that its benefits extend far beyond our muscles and cardiovascular systems. Exercise expands the productive capacity of our amine-producing cells, helping to inoculate us against anxiety, stress, depression and learned helplessness.It also floods our brains with what are called growth factors, and these keep existing neurons young and new neurons growing – some scientists call these growth factor brain fertilizer- so our brains are strengthened against stress and aging. A well -designed regime of physical exercise can be a boot camp for the brain.

Fatigue and focus

I once had a coach who told me “rest is a part of training. ” Similarly, one of the top performing hedge fund managers I know sleeps 9 hours a night, and is obsessed with importance of rest.

A recently developed model in neurosciences provides an alternative explanation of fatigue. According to this model, fatigue should be understood as a signal our body and brain use to inform us that than expected return from our current activity has dropped below its metabolic cost. The brain quietly searches for the optimal allocation of attentional and metabolic resources and fatigue is one way it communicates its results. If we are engaged in some form of search and have not turned up any results, our brain, through the languages o fatigue and distractibility tells us we are wasting our time and encourages us to look elsewhere. The cure for fatigues, according to this account, is not rest, it is a fresh task. Support form this idea comes from data showing that overtime work in itself does not in itself lead to work-related illness such as hypertension and heart disease, these occur mainly if workers have no control over allocation of their attention. Applying such a model could benefit workers and management alike, for more flexibility in choosing what to work on, and when, could reduce worker fatigues, while management might be delighted to find that workers may be just as refreshed by a new assignment as by a vacation. This model of fatigue provides a good example of how understanding a bodily signal can alter the way we deal with it.

Only complaint about Hour Between Dog and Wolf is it probably could have been a long form article- I suspect the book publisher wanted to fill it out. Still worth taking a look though. Hour Between Dog and Wolf provides a useful framework for anyone who has a high stakes job that requires stamina.

See also:

Askeladden Capital on Sleep/Rest/Chronotypes Mental Model

Askeladden Capital’s review of Misbehaving

Jack Ma’s Iron Triangle

I was cleaning out some files and came across notes from Alibaba: The House that Jack Ma Built.

The Iron Triangle

According to this book, Ali Baba’s rise has been the result of a combination of three strengths : E-commerce, logistics and finance. The author refers to these as the “Iron Triangle”

E-commerce, logistics, finance.

Ali Bababa’s e-commerce sites offer an unparalleled variety of goods to consumers. Its logistics offering ensures those goods are delivered quickly and reliably. Finance subsidiary ensures that Alibaba can get paid via a process is easy and worry free.

One can’t help but notice that there are many companies that have one or two parts of the iron triangle, but few that have all three. Of course there were several unique characteristics of China that Jack Ma has profitably exploited. It will be interesting to see if he succeeds in bringing this model abroad to other emerging markets, and to developed markets.

E-Commerce

China’s retail market is highly fragmented and inefficient.

“Key factor in success of e-commerce in China is the burden of real estate on traditional retailers. Land is expensive in China because it is a crucial source of income for the government. Land sales account for one-quarter of the government’s fiscal revenues. At the local government level they account for more than one-third. A prominent e-commerce executive summed it up “ because of the way our economy is structured, the government has a lot of resources. The Government decides the price of land…. The government relies too heavily on the taxes and fees associated with selling land. That almost destroyed the retail business in China, and pushed a lot of demand online. They deprived offline retailers of the opportunity to benefit from rising consumer demand- which they effectively channeled to e-commerce players. “

As a consequence, there has been far less investment in marketing, customer service, human resources or logistics in China’s traditional retail sector in the West. The result? China’s retail market is highly fragmented and inefficient. In the United States, the top 3 grocery chains account for 37% of all sales, In China they account for just 7 percent.

Despite all the shopping malls, offline retail penetration is quite low. In China there is six square feet of retail space per person, less than ¼ the amount in the US. Nature abhors a vacuum, and online retail filled in the gap left by inefficiencies.

“China’s e commerce market differs in important ways from the US and other western economies, the legacy of decades of state planning and important role played by state-owned enterprises. Alibaba has sought out and exploited inefficiencies these have creates, first in e-commerce, now in media and finance. “

Yiwu wholesale market was the template for first e-commerce operations. E commerce had started out with non-standardized products for mom and pop businesses.Lack of national supply chains removed barriers to entry that exist in west, making it possible for individuals to make a money.

Now China has greater e-commerce penetration than the US. Its always fascinating to see the leapfrogging phenomenon in action.

Logistics

China post laughed at Jack Ma’s attempt to enter logistics.

Zhejiang, where Ali Baba is headquartered is now home to most of China’s largst curior companies: Shentong(STO Express), Tuantong (YTO Express), Zhongtong ZTO Express, Yunda. This small cluster, referred to as the “Tonglu Gang” delivers 50% of all packages

Note that Wells Fargo had its own parcel delivery service in California gold rush.

Finance

Having its own financial services arm, Alipay diffuses trust throughout e-commerce empire. The rise of the smartphone was huge for Ali Baba’s financial services segment. Many financial innovations happened in nearby Wenzhou.

Ali Baba exploited inefficiencies in the financial services market, just like it did with online retail. State owned banks paid little heed to needs of individuals and small businesses. Alibaba has access to entire trading history of business customers, much better position to assess credit risk than traditional banks.

The Beginnings

Jack Ma’s story is quite inspiring for entrepreneurs.

In 1978, only 728 foreign tourists visit Hangzhou. Jack Ma went to the one hotel where foreigners went and read an English book, starting at 5 am. Every . Single. Day. He’d give free tours of West Lake to foreign tourists in exchange for English practice . He did this day for 9 years.

Long before Ali Baba, Jack Ma had an online directory business called China Pages. When he launched China Pages hardly any one in China had the internet.

Instead Jack came up with an alternative approach. First, he spread the word through friends and contact about what the Internet could do for their business. He then asked those interested to send him marketing materials to introduce their companies and products.

Then he mailed them to Seattle, had a company put them online. Then he printed out screenshots of websites and mailed them to friends.

People treated him like a con man, because he would get people to pay him $2,400(in RMB at the the then exchange rate), to design and host a website, even though the clientele couldn’t see the internet. That was a lot of money in China back then. He must have been a great salesman if he could get customers to pay that much for something they couldn’t see

Key lessons from Jack Ma’s early internet businesses

“It is difficult for an elephant to trample an ant to death as long as you can dodge well. “

More tech entrepreneurs began to emerge as China invested in telecom infrastructure. But internet bubble came and went. How did Jack Ma navigate this?

“ for Jack, the bursting of the bubble represented a great opportunity for Alibaba “ I made a call to our Hangzhou team and said “Have you heard the exciting news about the Nasdaq? … I’d like to have had a champagne on hand. This is healthy for the market, healthy for companies like us

He felt confident that now the IPO gate had closed, venture capital would stop funding Alibaba’s competitors. “In the next three months, more than sixty percent of the internet companies in China will close their doors, he said, adding that Alibaba had spent only $5 million of the $25 million it had raised. “ We haven’t touched our second round funding. “ We have lots of gasoline in our tank.”

Once the bubble burst, Alibaba started using the cash it had built up. Jack started hiring foreign talent and travelling around to tradeshows.

Tao Bao’s Iron Triangle Crushes E-Bay

Two key lessons from Ebay’s failure in China:

- Localize, Localize, Localize

- Its critical to have a faster product development cycle( this fits with John Boyd’s OODA Loop)

Ebay in China was led by foreigners and foreign educated with little knowledge of local amret. They tried to force feed American website standards.

Ebay’s arrogant disaster in China is a valuable business lesson. They continued to represent to investors that they were winning in China, but they lost disastrously. Alibaba had a faster product development cycle(ie OODA loop), and it adapted more quickly to local needs than eBay. eBay burned a lot of money. In the process, E Bay made everything look great on powerpoints and conference calls , but at odds with situation on ground.

Corporate headquarters demoralized local talent, (they ran a site called EachNet in China)

“This gap was reflected in the design of the two rivals’ websites. eBay moved quickly to align the EachNet site with its global site, revamping how products were categorized and altering the design and functionality of the website. This not not only confused customers, but also alienated a number of important merchants who saw their previously valuable China account names had been deleted. This invalidated their trading history and forced them to reapply for new names on an unfamiliar global platform. Worse still, the Chinese websites lacked a customer service telephone number. Ebay’s China site, modeled closely on eBay in the States looked foreign to local users, who found it “empty” when compared to local sites.

In website design, culture matters.

Taobao structured like local bazaar. Edge in e-commerce(see iron triangle above). Better understanding of country’s merchants. Let them do initial listings for free. Eachnet gave into short term shareholder pressure to charge for simply listing products online.

“Ebay just wouldn’t take Alibaba seriously, questioning the reliability of mounting data that showed Taobao was selling more goods than eBay in China. Taobao now had more listings, but eBay convinced itself that because these listings were free, they must be inferior. Jack vigorously rejected that thesis: “The survival and growth of Taobao are not because of the free service. 1Pao[the joint venture of Yahoo and Sina] is also free but it is nowhere close to Taobaol. Taobao is more eBay than eBay China [because] Taobao pays more attention to user experiences.”

Sensing it was over Alan Tien concluded, “Taobao’s product development cycle is much faster. Jack Ma’s right. We cannot fight on his terms.”

Jack Ma’s Iron Triangle had won.

Beyond headline numbers

Everybody has access to Bloomberg and Google. Every global macro investor closely follows macro data out of every country. To gain an an edge, one must look beyond headline numbers, and find underutilized datasets.

This applies when finding countries, industries, and individual companies in which to invest. Any time you want to combine top down and bottom up insights, you need to get creative with finding the right data.

Schumpeter and Perez

Joseph Schumpeter pointed out that aggregate figures “conceal more than they reveal”.

Relations between aggregates are

“entirely inadequate to teach us anything about the nature of the processes which shape their variations, aggregative theories of the business cycle must be inadequate too…”

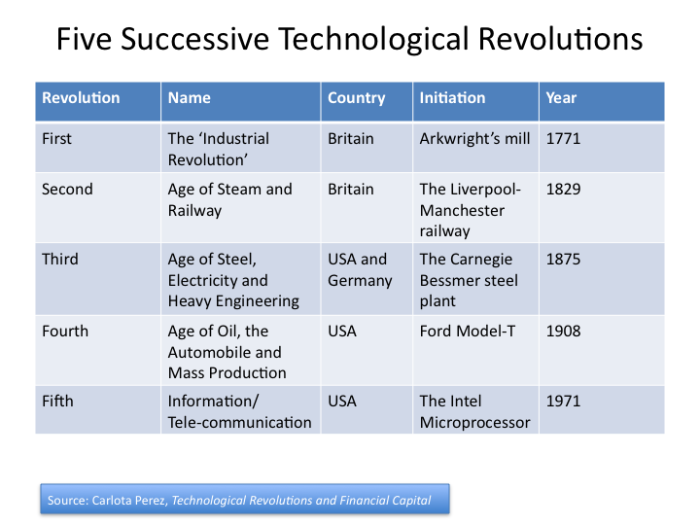

In Technological Revolutions and Financial Capital, ( Carlota Perez emphasizes that new technological paradigms can only be analyzed by looking closely at inner workings of an economy. Within the same country, or industry some subsectors will grow at astonishingly high rates, while others decline. Perez’s framework is valuable to analyzing times of great technological change, which is basically anytime. Examples she uses include the first British Industrial Revolution( the age of Steam and Railways, the Age of steel, electricity, and heavy engineering, age of oil, automobile and mass production.

Top line numbers such as GDP or earnings could deceive an analyst, especially when looking at a new market.

Valuation and pricing

“People living through the period of paradigm transition experience real uncertainty as to the ‘right’ price of things(including that of stocks, of course).”

Extreme jumps in productivity change relative price structures in the economy. “The change in relative price structure is radical and centrifugal. Money buying electronics and telecommunications today does not have the same value as money buying furniture or automobiles.” Therefore, looking at inflation or deflation in aggregate is deceptive. Many years after Perez’ book, this now exacerbated by the Amazon effect. To some effect this may impact valuation in some industries.

Research methods

Long term aggregate data, spanning multiple periods of technological change are senseless. This goes for GDP, corporate earnings etc. Yet disaggregated stats are rarely available(except during more stable phases), as Perez points out.

The internet has provided more opportunities to find disaggregated, unique, underutilized datasets. Often this means poking around on weird regulatory websites, and following up on footnotes to academic papers.

This process might be about to get a lot easier.

Google launched a new dataset search engine. I’m excited to see how its impact snowballs as more datasets are added. Although intended for journalists, it is likely to be a valuable tool for investors seeking differentiated alpha.

Of course that means today’s edge, will be tomorrow’s table stakes.

See also: The hard thing about finding easy things

History Repeats: The Serpent on the Rock

“History Repeats. The first time as a tragedy, the second time as a farce.”

– Karl Marx(1)

There are amusing parallels between the rise and fall of the real estate private partnership market in the 1980s, the pre financial crisis tenant in common(TIC) syndication market, and the post financial crisis non-traded REIT market driven by Nick Schorsch and his AR Global empire.

Each episode involved high fee investment products designed to fulfill investor desires for yield, tax efficiency and perceived stability, while creating disproportionate benefits for intermediaries. Each episode ended badly. And the cycle repeats, again and again.

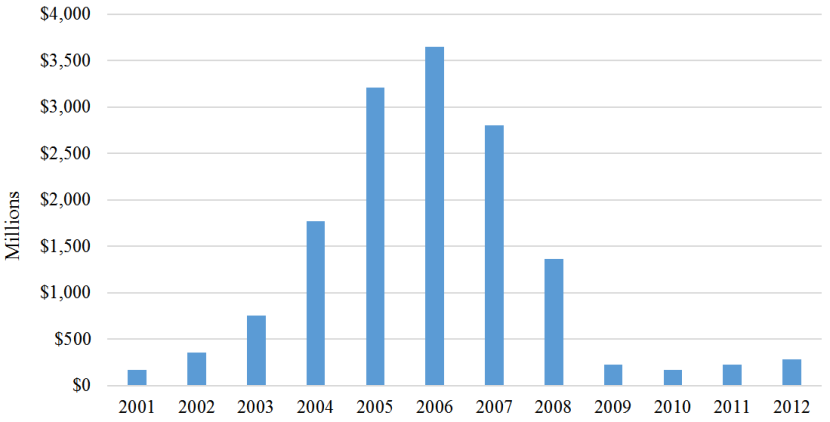

First of all, the charts tell parallel stories:

Real Estate Limited Partnerships 1970-1991

TIC Equity raised 2001-2012:

Source: Securities Litigation and Consulting Group

Non-traded REIT Equity Raise 2000-2016:

Source: Stanger Report, author’s calculations based on SEC filings.

Note that the 2015-2016 dropoff would be much sharper if you excluded Blackstone’s REIT, which entered the wirehouse channel in late 2016, and accounted for 50% of total annual NT REIT sales within a few months. Sales to the independent broker dealer(IBD) channel, which Blackstone largely bypasses, were completely decimated, and the dropoff has accelerated in 2017. (2)

May Day

High fee products are sold, not bought. The commissions on illiquid real estate products have always been higher than other investments available to retail investors.

In Serpent on the Rock Eichenwald traces the original real estate partnership craze back to the May 1, 1975 abandonment of fixed commissions on sale of stocks and bonds. Yes it is viciously ironic that commissions were fixed before 1975. The financial services industry was apparently afraid of capitalist competition and all the wonderful creative destruction it brings. Once they lost large commissions on simple security trades, they went looking through more complex higher fee product.

After May Day:

No longer could brokerage firms subsidize their bloated through fat commissions on securities trades. Firms unable to adjust collapsed by the dozens. The industry had to either dramatically cut back expenses or find new products with higher commissions that could be pumped through the sales force. Suddenly tax shelters, which sold for higher commissions than stocks and bonds didn’t look so unappealing.

The impact of May Day has continued to drive down commissions decades later. This makes sense. After all, transactional costs should approach zero over the long run, because with computers the marginal cost of doing a trade in all but the most illiquid complex markets is effectively zero. Significant scale and technological investment is necessary to run a brokerage business focused on liquid markets.

Consequently, the current IBD ecosystem is highly dependent on non-traded REITs and other high fee direct private placement programs. This is complicated by the fact that IBDs payout a high proportion of commissions to the financial advisers(like 90% in many cases). Many financial advisers built their business on 1031 exchanges, non-traded REITs or other private placements. TICs typically charged 20-30% commissions. Commissions eat up a large portion of offering proceeds for non-traded REITs. Additionally, non-traded REIT sponsors pay out a due diligence kickback to broker dealer home offices. Many smaller IBDs depend on these kickbacks for survival.

Of course, the commissions were much more egregious the first time around. Old timers fondly remember 20%+ loads on product. up front sales loads have now declined to high single digits and low double digits. Inland has driven down commissions on 1031 exchange product. Plus state securities regulators put out NASAA guidelines to limit loads on registered products. Nonetheless in an age where interactive Brokers charges $1 per side on a trade regardless of size, and few modern brokerages charge more than $7 per trade, even high single digit sales loads on non-traded retail product are absurd.

In Backstage Wall Street Josh Brown outlines his “Iron law of product compensation”:

The higher the commission or selling concession a broker is paid to sell a product, the worse that product will be for his or her clients.

This was the thread that connects the 1980s private partnership craze, with the pre financial crisis TIC explosion and the post financial crisis non-traded REIT market.

Yield Pig Exploitation and the Illusion of Safety

Just like private partnerships in the 1970s and 1980s, brokers sold TICs and Non-traded REITs to unsophisticated yield hungry retirees as safe, stable investments.

Here is one description of the private partnership market:

Many of the public offerings were promoted as a way for the small investor to participate in real estate, widely believed to be an inflation hedge, offering greater return and moderate risk as compared to stocks. The ability for an individual of modest net worth or income to invest in securitized real estate was viewed as a real benefit of public syndications.

The limited partners were sold their investments on the assumption that real estate was a safe, growing investment. Often these investors were unsophisticated in investment matters, and were more often swayed by aggressive brokerage salesmanship. The importance of liquidity became apparent to the investors only after substantial investment had already occurred. Liquidity was never promised for limited partnership securities and the partnership structure itself was designed to constrain liquidity.

In Serpent on the Rock Eichenwald meticulously tracked the juxtaposition between sales materials promising safety and the ultimate collapse in values.Non-traded REITs and TICs are also sold as safe investments that do not have the volatility of the stock market. Of course the stability is an illusion, and investors are still highly dependent on the real estate performance.

Due diligence

Eichenwald describes due diligence at Prudentialduring the peak of the private partnership craze:

The due diligence team was not just overwhelmed from the number new deals they had to approve- they also had to keep tabs on the old deals that had already been sold. Darr had negotiated for Bache to be paid a monitoring fee from some tax shelters it sold in exchange for reviewing their financial performance. Supposedly, this was designed to make sure that the general partners managing the deals did things right and took care of their investors. It was a key selling point for Bache brokers: In sales pitches, they painted a picture of top Bache financiers in green eyeshades peering over the shoulders of the General partners, watching everything that was done, The image of financial professionals crunching numbers late into the night to make sure investors were protected was a persuasive marketing tool.

But asset monitoring paid only a small fraction of the fees that Bache received from selling new deals. So the job of keeping an eye on the performance of old shelters quickly became viewed as simply a headache. It was an obligation that slowed down the whole process of churning out deals., without enough juice from fees to make up for the effort. The monitoring assignment became a hot potato, passed from executive to subordinates, and from then on down the line.

Many similar scenes in the book are shockingly familiar to anyone who has worked in the alternative investments space.

In subsequent years, third party due diligence firms serving broker dealers helped drive improvements in deal quality, but there are still many serious gaps. Since IBDs depend on the revenue from commissions and due diligence kickbacks, they are under pressure to find product to approve. This bias leads to cognitive dissonance. As non fiduciary middlemen, they often sell things that they wouldn’t invest in themselves, especially with a full sales load.

In the wake of the bankruptcy of TIC Sponsor DBSI, and the collapse of several tax driven energy deals, Reuters investigated due diligence in the independent broker dealer space. It highlighted a too cozy relationship between sponsors and third party due diligence firms.

Perhaps of even greater concern is the disconnect between due diligence process and the needs of end investors.

Potentially alarming findings are often obscured in multiple pages of recondite language, with no definitive conclusions. “They’re these long-winded things that bury things that might be important inside boilerplate disclosures,” said Jennifer Johnson, a professor at Lewis & Clark Law School in Portland, Oregon, who has written extensively about the private-placement business.

Due diligence firms say their reports aren’t designed to be read or understood by investors. Rather, they are meant to help brokers decide whether to recommend private placements to their customers.

Same Same, But Different

Although the distorted incentives,exploitation of unsophisticated yield pigs,were almost identical in each of the three historical examples in this post, there are several key differences. Broker dealers primarily sold private partnerships in the 1980s as a way of reducing taxes. An investor can use a TIC structure as part of a 1031 exchange to delay taxes when selling a property. REITS are a unique IRS creation but the reason for investing in a REIT is mainly income(Excluding situations where someone exchanges via an UPREIT transaction)

The private partnership market collapsed because the tax reform act of 1986 destroyed their entire structure, and basically collapsed the national real estate market. (see: this FDIC report )

The TIC market collapsed when the financial crisis hit the entire real estate market, exposing the problematic underwriting of the TIC Sponsors. However, regulatory issues weren’t the main driver of the collapse. Like the private partnership craze in the 1980s, the modern Non-traded REIT market also collapsed due to regulatory change although the . Finra 15-02, which increased the transparency on client statements, made it harder for advisors to get away with charging the massive sales loads. The fiduciary standard required broker-dealers to act in the best interest of clients, also led many broker-dealers to suspend or slow down the sales of high commission products.

The farce of AR Global’s collapse

Although private partnerships and TIC sponsors generally overpaid for properties they purchased, the collapse of their structures happened during a time of across the board real estate declines in the US

In contrast, investors in post financial crisis vintage non-traded REITs have suffered, in spite of a buoyant real estate market. ARC Hospitality(Now Hospitality Investors Trust) offered shares at $25.00 a share from 2013-2015, and a client statement never would have shown a value below $22.00 until this summer. It revalued at $13.20. A PE fund recently offered $5.53 for the shares. Likewise ARC Healthcare Trust III sold shares $25.00, and recently marked its value down to $17.64, and is now subject to an affiliated transaction with no liquidity event in site.

Private partnerships and TICs were tragedies, AR Global was a farce.

To be continued….

(1) This is from The Eighteenth Brumaire of Louis Napolean.

The full translated quote is :Hegel remarks somewhere that all great world-historic facts and personages appear, so to speak, twice. He forgot to add: the first time as tragedy, the second time as farce.

(2) Wirehouses generally did not sell non-traded REITs until Blackstone entered the market in 2016 Anyone who carefully read The Serpent on the Rock will note how incredibly ironic it is that wirehouses have started to sell non-traded real estate securities again. More on his in a future post.

Minsky and the Junk Bond Era

King of Capital: The Remarkable Rise, Fall, and Rise Again of Steve Schwarzman and Blackstone discusses the early days of the leveraged buyouts(LBOs) and junk bonds from the vantage point of Blackstone’s founders.

In 1978, KKR did an LBO of an industrial pumps make (Houdaille Industries). There had been many small LBOS of private businesses, but no one had gone that big, done a public company. A young investment banker named Steve Schwartzman heard about the deal and realized he had to get his hands on that prospectus. “He sensed something new was afoot — a way to make fantastic profits and a new outlet for his talents, a new calling.

“I read that prospectus, looked at the capital structure, and realized the returns that could be achieved.” he recalled years later. “I said to myself, ‘This is a gold mine.’ It was like a Rosetta stone for how to do leveraged buyouts. “

Speculative Bridge Financing

It quickly became apparent how lucrative leveraged buyouts could be.

LBOs were financed with Junk Bonds. The process of issuing junk bonds was messy and cumbersome. It took most banks an extremely long time to issue bonds. Drexel was so adept at hawking junks, that companies and other banks in a deal would go forward on an LBO based solely on Drexel’s assurance that it was “highly confident” it could issue bonds. Other banks that couldn’t do that would offer short term financing, aka bridge loans, so a buyer could close a deal quickly, and then issue bonds later to repay bridge loans This alowed DLK, Merril Lynch, and First Boston to compete with Drexel in the LBO financing space.

But what if the bonds couldn’t issued? How would the bridge loan be paid for?

… bridge lending was risky for banks because they could end up stuck with inventories of large and wobbly loans if the market changed direction or the company stumbled between the time the deal was signed up and the marketing of the bonds. The peril was magnified because bridge loans bre high, junk bond-like interest rates, which ratcheted up to punishing levels if borrowers failed to retire the loans on schedule. The ratchets were meant to prod bridge borrowers to refinance quickly with junk, and up until the fall of 1989, every bridge loan issued by a major investment bank had been paid. But the ratchets began to work against the banks when the credit markets turned that fall. The rates shot so high that the borrowers couldn’t afford them, an the banks found themselves stuck with loans that were headed towards default.