Humans have flawed brains that cause them to act crazy sometimes. And in groups, people get even more crazy. Many smart people believe dumb things. Sometimes a group of otherwise completely sane people come together and do something insane. History is full of examples of the “ Extraordinary Popular Delusions and the Madness of Crowds, or Manias, Panics and Financial crisis. Humans sometimes join suicide cults. Human literally burned witches not that long ago. Groupthink is a helluva drug.

Financial markets provide an arena in which the biggest gains can be made betting against consensus. Yet statistically speaking, the consensus is usually right. The times when the crowd goes crazy are notable because they are exceptions. One must carefully decide when to be a contrarian.

Under what conditions is the consensus likely to be wrong? Lets invert the question: under what conditions is the crowd likely to be right?

Most of the time, a large group of people actually comes to a more accurate conclusion than any one individual. The success of Estimize, which crowdsources earnings estimates is one useful empirical example.“Wisdom of Crowds” is a well documented phenomenon, and well summarized in the book by the same title.

Why is the crowd so often right? What must happen for the crowd to be right ? Researchers have identified four interrelated conditions that encourage the wisdom of the crowds:Diversity, Information Availability, Decentralization, and existence of an Aggregation Mechanism.

Understanding these conditions can help one know when to follow the zeitgeist, and when to make a contrarian bet against it. A firm grasp of the facts on both sides of a controversy is necessary, but possibly not sufficient. One can never be sure of all the facts. Its also useful to understand the broader social forces, and how they influence the likelihood of the consensus being right or wrong. Searching for these conditions(or their absence), can be a useful method of avoiding cults and identifying opportunity, beyond just the facts of the individual situations.

The biggest gains are available by being a contrarian who understands the crowd.

The key is understanding when the wisdom of crowds flips to the madness of crowds. And the essential insight is that it has to do with a violation of one or more of the core conditions for a wise crowd.

Diversity implies that each person has their own point of view and some private information, even if only their unique interpretation of the available public information. Diversity is important because it adds different perspectives and increases the amount of available information.

Crowded trades have a tendency to crash- leading to no bid markets all the way down. Academics have noted that in a run up to a market crash diversity of population declines. The market becomes fragile, and eventually there is no one to buy from (or sell to).

One reason Estimize’ earnings estimates have tended to be better than Wall Street Sell side is that Estimize analysts are a diverse group of independent thinkers from around the world, holding a variety of different jobs. A lot of Wall Street analysts go to the same conferences, went to the same schools, etc.

When people come to the same conclusion from different backgrounds, logical methods, etc , their collective wisdom refines understanding of reality. The opposite occurs when people feel pressure to conform. Its important to note this is a genuine deep diversity of thought and perspective, not a superficial check the box diversity.

If multiple people with different viewpoints all come to similar conclusions, the odds of the opposite being true decrease substantially. On the other hand, if there is an obivous archetype of the thinker on the other side, then maybe a contrarian opportunity is available.

As Michael Maubossin has noted- conformity is a nonlinear process:

Scientists even have a sense of the neurobiological basis for conformity.Informational cascades occur when individuals follow the decisions of those who precede them without regard to their personal information.

Epidemiological models are useful here.

Information

The wisdom of crowds does not emerge in groups of idiots. It only applies when there is widespread access to information necessary to reach a conclusion. The extreme opposite occurs in totalitarian societies (or large corporations), where information is tightly restricted. Prior to the internet, information sometimes diffused slowly through a market, leading to massive price discrepancies obvious at even a quick quantitative glance.

Quality of input is critical to the success of crowdsource analysis:

Alternatively, it is possible that the inclusion of forecasts from certain individuals, such as Non-Professionals, may provide no value, or worse, cause the Estimize consensus to deviate further from actuals. Surowiecki (2004) states that although diversity matters, assembling a group of diverse but thoroughly uninformed people is not likely to lead to wise outcomes.

Independence

Independence is related to diversity. People need to be able to freely analyze reality and discuss opinions. Conventional wisdom is more likely to be accurate when it is freely subjected to challenge. When there are institutional or social factors that make people extremely afraid to speak truth, what everybody says to be true, may be wrong.

Children learn of this phenomenon early through the Emperor Wears No Clothes. For grown ups, see Death of Stalin for an example of lack of independence leading to morbidly hilarious results.

Independence requires relative freedom from opinions and actions of others, not complete isolation. Independence enables people to actually express their diverse information and reduces potential bias in the group decision.

Decentralization

Decentralization allows people to specialize and draw on local knowledge, without any individual or small group dictating the process.

Diversity and independence all fit in nicely with decentralization. Through specialization, decentralization encourages independence and increases the scope and diversity of information. Decentralization reduces the risk that independence and diversity will go away. Similarly having capital flows from all around the world, not just from a small group of schools or similarly thinking firms, increases the likelihood that markets become more efficient.

Existence of an Aggregation Mechanism

Finally, an aggregation mechanism is necessary to collect the individual opinions and harness the ‘wisdom-of-crowds’ effect.

This is basically why capitalism has succeeded. The price mechanism aggregates facts about supply and demand better than any bureaucracy could. At the same time, this why often the best opportunities to earn an investment profit are in illiquid asset classes where the market does not function as an aggregation mechanism to make the price close to right.

Of course, just because the market consensus is wrong, doesn’t mean that is necessarily wise to bet against it today. Must also consider reflexivity, narratives, and capital flows etc, and maintain a balance sheet that allows one to survive long periods of mass delusion.

Postscript: This is all indirectly related earlier post on finding underfollowed opportunities: The hard thing about finding easy things . This linked the ideas of both Sun Tzu and Warren Buffett. Some of the specific opportunity sets mentioned in this post have since been too widely known and we’ve moved further into more esoteric off the beaten path ideas. Nonetheless the basic principal still holds: there are more likely to be opportunities where the crowd isn’t looking.

What would happen if the internet crashed everywhere- completely died, and didn’t come back? Tim Maughan’s Infinite Detail is a dystopian sci fi novel that hits close to home.

The book alternates between Before and After chapters, slowly revealing details on the great crash that destroyed the global internet infrastructure. There is also an ongoing long distance love story interrupted by the great crash.

The Before chapters are a slightly more advanced version of our current reality. Everything is connected and everything is tracked. People accept lack of privacy in exchange for extreme convenience. Almost everyone uses “Spex” which are glasses that allow people to access information just by moving your eyes- a step more convenient than a smartphone . Cities are all “smart” with services such as trash collection automated.

The book explores how the underclass is impacted by smart cities. Relying on RFID tags for recycling means people who collect cans to survive(canners) are subject to problems caused by technology. The city is full of canners:

There’s hundreds of us. Thousands, maybe. City is full of ’em. Used to be a lot of people did it as a part-time thing, but more and more are going full-time, it seems. Especially since there’s no work for cabbies now, y’know? I used to know a lot of cabbies that would just do a little canning on the side when work was slow and all, but now they gotta go full-time, they says. Say nobody wants anyone to drive a cab anymore. I ain’t worried, though.

The attitude of one superstar canner is eerily reminiscent of people who fail to keep up with changes in the digital economy:

“Hell yeah! Canning is a growth industry. I been doing this fifteen years, and every year I seen more cans than before. There’s always going to be canning, as long as there’s people that want to drink. They’ll never stop that. Never take that away from me. They might not need cab drivers anymore, but they’ll always need canners.” He smiles, for the first time. Rush isn’t sure what to say to him. He sighs and looks at the cart, and the hundreds of floating tags reappear. His heart sinks.

A group of disillusioned techno optimists are they key characters in the Before scenes. Their views are basically a more extreme version of current critics driving the anti Silicon Valley backlash. Many of them started out as idealists who believed in the internet, but became cynical as corporations and governments started using it for control.

We used to think that we could own it, that we were fighting to build communities for ourselves. That it was ours for the taking. To stake a claim for a place we could control and belong, a fight to make “safe spaces” for ourselves.It was a noble thing to think, that we were fighting for our own spaces, but we were kidding ourselves. We never owned these spaces, we never could. They were never ours to own, never ours to control. Instead we watch our battles turn into spectator sports, our revolutions turn to infighting. We watched our new communities dissolve into civil wars. We watched our political activist and community leaders become celebrity brands, our tech-utopian visionaries bow to capital and shareholders

A group of them builds an experimental community completely cut off from global networks. A terrorist group combines hacking with real life terrorism. Their motto is “With zero bandwidth there is no calling for backup.”

Rumors spread that someone is developing a virus that can impact all internet connected devices. When its released, people experience:

a very real sense that something had ended, had gone, something huge and fundamental. The feeling that a structure — a way of life, something nobody could really imagine changing — had collapsed. The end of being watched. The end of being tracked. The end of being indentured to it all. The end of capital. The end of security. The end of knowing. The end of safety. The end of being reassured. The end of being connected. The end of friendships. It was all there, in that crowd, sprayed across faces that had been denied sleep and electricity and communication for days — the fear, the uncertainty, the excitement, the thrill. The relief.

The After chapters describe a post apocalyptic hellscape where people struggle for survival. Chaos breaks out across the world as every city simultaneously goes dark. The descriptions are fantastic

…video games industry conference in Los Angeles that had to be abandoned and had quickly dissolved into spoiled man-children rioting; an automated container terminal in Shanghai that shut itself down for nearly a week and caused the collapse of at least two shipping companies; and countless other blackouts and disruptive infrastructure failures. He’d also seen it connected to protests—the Times Square blackout being just the latest, after an uprising of migrant workers in Singapore, and the takeover of a brand-new, built-from-scratch, concept-art-perfect smart city by an army of protesters from the slums of Mumbai.

As is often the case, utopian revolutionaries are dismayed at what happens in real life, once they actually “win”. Civil wars occur around the globe. The former unconnected haven ends up turning into a scene of bloody conflict between the old guard government, and a group of outlaws. Basically everything is worse than it was before.

As one character puts it:

Your self-determination is a fucking power vacuum, that’s all it is. Your revolution, with no idea of what would happen next, just created a massive hole full of people fucking each other over to stay alive.

The impact on people’s material well being is most stark.

She finds herself heading down the steps of a long-motionless escalator to the floor below, eager to explore, drawn to join in, wanting to experience what appears to be the decentralized, community-driven anarchic economy they’d spent so many late, stoned, enthusiasm-soaked nights dreaming of…

Instead, standing in the silence of the first shop she passes, she finds inevitable disappointment. For a start, the nameless store has barely any stock, and what is here is a disorganized mess of broken, discarded junk piled up in boxes or spread randomly around the half-bare shelving—at first glance she thinks it could even be the ramshackle debris left over from the original store’s ransacking, but soon she realizes the truth is even more depressing. For that to be true there’d have to be some shred of purpose, form. Between embarrassed glances she starts to think that maybe it’s just her own deep-rooted, bred-in consumer expectations clouding her assessment, so she tries to throw them aside and embrace the nonconforming landfill-mined chaos of scuffed plasticwear, broken crockery, torn clothing, dead electronics, and crumbling paperbacks—but it’s impossible. There’s not just a lack of organization here, it’s a total absence of function, value.

People who had acquired a cargo ship ahead of the crash go on a tour of the world, and observe collapsed cities, and silent ports. Its an interesting commentary on global supply chains. They make everything so convenient, but are really quite fragile.

This was why the supply chains existed, in order to make transactions that logic dictated were most efficient on local scales work on global ones, through sheer size, brute force, cheap labor, and global inequality.

…pinnacle of human effort had been to create a largely hidden, superefficient, globe-spanning infrastructure of vast ships and city-size container ports—and all to do nothing more than keep feeding capitalism’s hunger for the disposable. To move plastic trash made by the global poor into the hands of hapless, clueless consumers. A seemingly unstoppable beast built from parasitic tentacles, clenching the planet with an iron grip.

The crash has an irreversible impact on relationships, especially those that are long distance:

He sits there for a minute, in silence. It’s the first time they’ve been forcibly disconnected like this, and it’s jarring. Like they’ve been ripped apart, like he’s lost control. Suddenly the frailty of their relationship feels exposed, like it’s utterly reliant on this vast global infrastructure that he doesn’t own or control, that’s too complex for any one person to understand, that could break or disappear without even a second’s notice. He could lose him completely, just at the flick of a switch, at the typing of a command.

Benin rice imports more than doubled between 2015 and 2017. Its a tiny country, slightly smaller than Pennsylvania, with a population of 11 million. Yet it is now the world’s largest importer of Thai rice. Why?

Turns out the answer has little to do with cuisine, and a lot to do with incentives. Benin shares a border with Nigeria, a much larger country that put strict tariffs on rice in 2014. Smuggling rice from Benin into Nigeria became big business. (see here,here, and here)

Unintended consequences of trade policy permeate Nigerian life. One of the richest people is a cement manufacturer. It just so happens that cement has a 60% tariff. Oh, and Nigeria doesn’t exactly have great infrastructure. Basically the only businesses of any size that can survive depend on some sort of favorable policy. The textile industry can’t really compete with cheap foreign imports, for example.

Favored importers get access to USD at a favorable rate. Petroleum importers, and the politically connected get an even better rate. Everyone else has to pay nearly twice as much of the local currency (naira) to access USD on the black market. I’m not sure if there is a secondary market in whatever documents importers can use to access cheaper USD, but if there is, these documents could be quite valuable.

Department of Unintended Consequences

Tariffs and exchange controls are not necessarily bad. One can hardly blame Nigerian policy makers. Powerful political constituencies depend on favorable policy. Nigeria has had a rough few decades, and opening up to foreign competition can create disruption. But trying to understand an economy requires looking beyond immediate impact, and finding second order impacts that are the unintended consequences of intervention. Even in neighboring countries. Never underestimate the power of incentives.

Bollore is one of the greatest capitalists most Americans have never heard of. There aren’t many examples of other French corporate raiders. He built up a massive business empire consisting of 457 companies over four decades. In the three decades its main holding company has been public, investors are up 40x, compared to an 8x return to France’s index. Its a story horribly neglected by English language media(most of the time). Some argue that the various holding companies are full of hidden value, others that they are on the brink of collapse. At the very least, as Muddy Waters has pointed out, you can’t model it in a spreadsheet. Here is what it looks like:

Accounting reality and economic reality are often divergent. You get interesting feedback loops from all the cross shareholdings. The Economist article takes a bit of a bearish slant

Analysts attribute over a third of Bollore SA’s Market value to shareholding in its parents; these parents are also worth around 12 billion in total. That does odd things to Bollore SA accounts. When its value falls (like last year when its shares lost 24%), that of the holding companies above it dips too. Because Bollore SA in turn owns them, its balance-sheet and income must be adjusted downwards. This then effects metrics used to calculate the value of its shares, whose fall prompts a further adjustment. Share-price rises cause upward revisions.

I would place clearing houses in the category, of important risk that not a lot of people are thinking about. Everyone knows central clearing is better(which it generally is), but ignores how clearing houses actually work. Clearing houses have offsetting positions, so they never have directional risk. However if one side of a transaction goes bust, and the clearing houses funds are exhausted, then members need to pay in.

Nasdaq Clearing’s recent Norwegian problems have put this issue on more people’s agenda. Clearing houses have outright failed in the past (Paris 1974, Kuala Lumpur 1983, Hong Kong 1987) . Post financial crisis global clearing has become increasingly centralized. If it fails the need for members to pay in could be a systemic problem. Who will clear the clearing houses when they get too big?

The collapse of Cho’s network would lead to one of Hong Kong’s most spectacular stock implosions and is now part of the biggest investigation of market malfeasance in the city’s history, an effort to expose and shut down what the regulator has called “nefarious networks.” These are groups of public companies, licensed dealers and other financial firms that “enrich themselves at the expense of unsuspecting investors,” Securities and Futures Commission enforcement head Thomas Atkinson said in an October speech revealing plans for criminal and civil action against about 60 companies and individuals. Their activities, Atkinson said, are “having a deleterious effect on our markets.”

Over the last few years, the late-stage (pre-IPO) market has become the most competitive, the most crowded, and the frothiest of these financing stages. Investors from all walks of life have decided that “late stage private” is where they want to play. As a result, a “late-stage” financing is no longer reserved for high-revenue, pre-profitability companies getting ready for an IPO; it is simply any large round of financing done at a high price. An unprecedented 80 private companies have raised financings at valuations over $1B in the last few years. These large, high-priced private financings are the defining characteristic of this particular technology cycle.

Some have argued that each of these companies would already be public in a prior era. Buying into such a notion is dangerous – dangerous for the entrepreneur and dangerous for the investor. Actually, very few of these companies are at a point where they could or should consider being public. Lost in this conversation are the dramatic differences between a high priced private round and an IPO. Understanding these differences is crucial to understanding the true risks in this large private-round phenomenon.

In the early stages, we’re looking for a few things. First, is the political environment: you want a country that ha been through political change that has made things more stable. For example, Russia had come out of a period of chaos, and Yeltsin finally established more personal control and installed a prime minister who could make things happen. We’ve seen this many times, in Georgia in 2004, and Mongolia. Second is macroeconomic stabilization. If you have a government that is determined to stabilize the economy, it’s often after a period of high inflation or when they’ve lost a war and everything is in chaos. Someone comes in and manages to get control of the economy, and bring the inflation rate down. Third, we look for a functioning capital market that should have a few investible stocks. It doesn’t have to have a lot. You can make a lot of money on just one stock, which is what we did in Georgia where we made 10x our money on Bank of Georgia. …

In general, ETFs have proven to be a poor way to invest in emerging markets. Institutional investors who want low fees and that have played emerging markets through ETFs are starting to realize that it may not be suitable, and there’s a reason why: ETFs are market cap-weighted. Market caps tend to be the largest in state owned or state-influenced companies, which generally tend not to be managed for the benefit of minority shareholders. The top five stocks in the MSCI Russia constitute 60% of the index. You’re missing out on all these amazing companies that have smaller market caps.

A lot of investors – including us – were influenced by William Thorndike’s excellent book, The Outsiders, which profiled eight CEOs with some common traits that work wonderfully at certain types of businesses. Outsiders improve operational efficiency, make opportunistic buybacks, bold M&A decisions, and so on. They work great when a business generates a lot of cash and has room to generate more. There’s a clear blueprint for success. On the other hand, there are situations in which there is no blueprint for success – new and emerging industries or business models, for example, or trying to revive a company in steady decline. In these situations, an Outsider CEO will do more damage than good. Here, you’d rather have a Visionary/Creative CEO at the helm who inspires his or her staff, is mission-driven, and is willing to experiment with new products or services. Limiting your concept of a “good” CEO to the Outsider archetype can lead to you missing out on opportunities in companies on their way to establishing or dramatically widening their moats.

…we are now faced with a series of peculiar ideas that draw heavily on misleading uses of the term data. They call for the monetisation of data, stating that it is valuable, and customers should be compensated for providing it. These ideas presuppose that data is some kind of commodity, and even the refutations of these positions engage with inherent differences between, say, data, which can be reused, and oil, which can’t. But the conversation doesn’t even need to reach this point.

GSO was a dominant force in the massive restructuring of credit that started a decade ago, becoming a major lender to non-investment-grade companies that the banks could no longer finance with cheap money after 2008. Banks retreated to their traditional role as advisers to corporations, underwriting bonds for highly rated companies and riskless deals. That left an enticing vacuum, and many firms eagerly and profitably stepped in, including Apollo Global Management, Ares Management, TPG Capital, KKR & Co., Bain Capital Credit, and scores of smaller credit shops. GSO capitalized on being early and being part of Blackstone, yet still independent. Now firms like Apollo and Ares have become formidable competitors in huge sectors like business development companies.

When each side has exhausted the potential for trade-damage by tariffs (and the US has inflicted all the self-harm it can bear), if not sooner, we would not be surprised to see Mr Trump apply capital sanctions and force US Persons to dump their holdings of Chinese equities and bonds. They have potentially wide scope to do this, using the US Treasury’s Office of Foreign Assets Control (OFAC)

Side note: since sanctions are such a handy tool, trigger happy Trump has used sanctions a lot. This has created a bull market in financial compliance services, in spite of the general trend towards deregulation.

In the United States there are four schools of thought on China policy. Till recently, the mainstream school of thought was that of engagement. Its proponents argued that China’s market reforms were good for the United States and the international community as a whole, since they believed that economic liberalization would spill over into politics and lead to political democratization, and that China would gradually become more and more like the US. They put their faith in American soft power, believing that the US would exert a subtle influence on China. On the opposite side were the China hawks that supported the school of containment, who argued that the ideologies of the two would never be compatible as long as China remained under the totalitarian rule of the Communist Party. They believed that, as her economic power grew, China’s threat level would go from mere adversary to potential enemy. One can see that people from both camps carry a certain amount of missionary zeal that is the hallmark of American tradition. The third school was the school of pragmatism, particularly popular in the business community. The rationale behind this approach was that China’s rise has created many business opportunities for American companies. In addition, both were big nuclear states, and should stay friendly. Furthermore, closer economic ties could win China’s cooperation and support in addressing global challenges such as global financial crises, nuclear nonproliferation, climate change and counterterrorism. The fourth group was the populists, who came mostly from the lower and middle classes and helped elect Trump. Supporters of populist policy viewed themselves as primarily victims of globalization and the rise of China, citing the ills of unemployment and the hollowing-out of American manufacturing.

My contention is that nearly all really successful businesses — like Dyson, Apple, Starbucks, and Red Bull — owe most of their success to having stumbled onto a psychological magic trick, even if unwittingly. But you don’t have to stumble onto it. To find that magic, you must embrace the idea that anything — from consumer behavior to people’s perception of a product — can be transformed, so long as you’re willing to think like an alchemist.

The models that dominate all human decision-making today are heavy on logic and light on magic. A spreadsheet leaves no room for miracles. But while logic may be right in the narrow sphere of physics, it is hopelessly wrong when it comes to the very different business of psychology.

We don’t value things; we value their meaning. What they are is determined by the laws of physics, but what they mean is determined by the laws of psychology. The reason the alchemists gave up in the Middle Ages was because they were looking at the problem the wrong way. They had set themselves the impossible task of trying to turn lead into gold but had got it into their heads that the value of something lies solely in what it is. This was a false assumption, because you don’t need to tinker with atomic structure to make lead as valuable as gold. All you need to do is to tinker with human psychology so that it feels as valuable as gold, at which point, who cares that it isn’t actually gold? If you think that’s impossible, look at the paper money in your wallet; the value is exclusively psychological.

All these disproportionate successes were entirely illogical. And all of them worked. In the modern world, oversupplied as it is with economists, technocrats, managers, analysts, spreadsheet tweakers, and algorithm designers, it is becoming a more and more difficult place to practice magic — or even to experiment with it. I hope to remind everyone that magic should have a place in our lives. It is never too late to discover your inner alchemist.

Dr. McHugh believes psychiatrists’ first order of business ought to be to determine whether a mental disorder is generated by something the patient has (a disease of the brain), something the patient is (“overly extroverted” or “cognitively subnormal”), something a patient is doing (behavior such as self-starvation), or something a patient has encountered (a traumatic or otherwise disorienting experience). Practitioners too often practice what he calls “DSM checklist psychiatry” — matching up symptoms from the Diagnostic and Statistical Manual of Mental Disorders with the goal of achieving diagnosis — rather than inquiring deeply into the sources and nature of an affliction

Israelis “know that you can get a terrible psychological reaction out of a traumatic battle. And they do take the soldiers out, and they tell them the following: ‘This is perfectly normal; you need to be out of battle for a while. Don’t think that this is a disease that’s going to hurt you, this is like grief. You’re going to get over it, it’s normal. And within a few weeks, after a little rest, we’re going to put you back with your comrades and you’re going to go back to work.’ And they all do.” By contrast, American psychiatrists say: “‘You’ve had a permanent wound. You’re going to be on disability forever. And this country has mistreated you by putting you in a false war.’ They make chronic invalids of them. That’s the difference.”

The Great Weirding and associated narrative collapse is, in a sense, the narratives of the industrial age reaching some sort of diffraction limit. Even the best historians of our age will not be able to handle the narrative collapse we’re living through with traditional history-writing techniques. So what are our options?

We could go grander. Bigger telescopes! This is what a lot of big history theorizing of the Sapiens variety appears to attempt. The results are kinda janky and feel like unsatisfying just-so myth-making. It is just hard to make and hold up really big mirrors to the human condition. We could work with shorter and shorter wavelengths. I think this is roughly what intersectional identity politics is trying, and failing, to do. Or finally, we could learn to work with our own wave-like nature, embracing diffracted identities and multitemporality

I like to think of it in terms of that old stoic line: the only way out is through. I’ve preferred the slight variant the only way through is through, because with time, there is no “out”, even though sometimes it is helpful to pretend like there is. The quantum-tunneling update to that is: the only way through is to diffract through.

That’s why we are in the Age of Diffraction. You have to interfere with yourself to get anywhere at all.

What we are seeing is that, in ultramarathons, more and more of the fatigue comes from central fatigue, which means that the brain is not able to drive the muscle, even though the muscle is capable,” says Shawn Bearden, a professor of exercise physiology at Idaho State University. Researchers in France have hooked runners up to electrodes to stimulate muscles, demonstrating they still have the ability to produce movement. “There’s something about a person’s brain that just isn’t driving the muscle as well late in these very long-distance races,” Bearden says. “It turns out women have a slightly, it seems, better resistance to that kind of fatigue.” While some studies show no real difference—women are on par with men—others show women with an ever-so-slight advantage. “Running economy and fatigue resistance are places where women seem to have a bit of an edge,” says Bearden. “And, with those two factors, the longer the distance of the race, the more important those two factors are.”

A marathon is run on a relatively flat, paved road designed to remove variables. But because there are so many hazards along the course of an ultramarathon—from tree roots and loose rocks to bee stings and hallucinations—few runners have perfected their craft. No one factor in an ultramarathon will propel a winner to the podium, but a single mistake can remove any runner from the race. An ultramarathon, therefore, may be the competition where gender matters the least.

We Are Nowhere Close to the Limits of Athletic Performance Gene editing will have a far bigger impact than doping. Although performance has increased a lot in the past century in basically all sports, we are still far from our true potential. Interesting to think of the search problem inherent in getting the best talent into the right sports.

Now we are entering an era in which it will not be chance that configures DNA, but rather the human intellect via tools of its own creation. As our understanding of complex traits improves, genetic engineers will be able to modify strength, size, explosiveness, endurance, quickness, speed, and even the determination and drive required for extensive athletic training. Estimates of the number of variants controlling height and cognitive ability, two of the most complex traits, yield results in the range of 10,000.5 If, as a simplification, we assume that in each of the 10,000 cases the favorable variant is present in roughly half the population, then the probability of random mating producing a “maximal” outlier is roughly two raised to the power of negative 10,000, or about one part in a googol (10 to the power 100) multiplied by itself 30 times. Of course it may not be possible to simultaneously have all 10,000 favorable variants, due to debilitating higher-order effects like being too large, or too muscular, or having a heart that is too powerful. Nevertheless, it is almost certain that viable individuals will exist with higher ability level than any person has ever had.

In other words, it is highly unlikely that we have come anywhere close to maximum performance among all the 100 billion humans who have ever lived. (A completely random search process might require the production of something like a googol different individuals!

But we should be able to accelerate this search greatly through engineering. After all, the agricultural breeding of animals like chickens and cows, which is a kind of directed selection, has easily produced animals that would have been one in a billion among the wild population. Selective breeding of corn plants for oil content of kernels has moved the population by 30 standard deviations in roughly just 100 generations.6 That feat is comparable to finding a maximal human type for a specific athletic event. But direct editing techniques like CRISPR could get us there even faster, producing Bolts beyond Bolt and Shaqs beyond Shaq.

The Gospel According to X-22 Classic article profiling one of the greatest backgammon players of all time(and the author of classic books). Interesting how he was decades before the “moneyball” movement in sports.

“The dice”, Magriel contends, don’t change the game intellectually, but only psychologically. Theres still a move for every roll in every position. But the dice make the game a gamble. They make a game perverse. It can be unbelievably vexing The dice can mock you, tease you, lead you on. It requires a certain amount of masochism to subject yourself repeatedly to their brutality. But intellectually, the challenge is to react neutrally to the dice, to make the right move on a bad roll on as a good one.

…

Peculiar looking plays of course are relative to one’s expectations. There is no such thing as an inevitable arrangement of checkers in backgammon, any more then there is such thing as an inevitable musical scale. Its purely a matter of convention. But conventions come to seem inevitable ,and it takes a special species of genius to see beyond them.

The rapid growth of ETFs is one of the most significant changes to financial markets in the last decade. Total ETF AUM grew from $0.5 trillion in 2008 to over $3 trillion by the end of 2017. More remarkably, AUM of ETFs invested in illiquid sectors such as global bank loan , emerging market bonds, and global high yield bonds increased 14 fold from $10 billion 2007 to $140 billion at the end of 2017. Prior to the last financial crisis, ETFs were a relatively small niche, but these past few years it seems like every asset manager has launched an ETF. Most investors have a large portion of their retirement assets in ETFs, and many investors exclusively invest in ETFs.

This is a major systemic change from what was in place prior to the last financial crisis. Since markets go through cycles its worth asking: how will the ETF ecosystem hold up next time there is market turmoil?

ETFs have overall been a massive benefit to investors because they lowered costs. Yet as more and investors put more and more money into ETFs, there are growing signs of distortions. Some investors have pointed out how ETFs are creating bizarre valuations that are unlikely to be sustainable. Additionally, there are growing signs that the ETF structure is far more fragile than most market participants realize. These aren’t just doom and gloom conspiracies from Zero Hedge. Organizations such as the IMF, DTCC, G20 Financial Stability Board, and the Congressional Research Service have all pointed out possible risks from the unintended consequences of ETF growth.

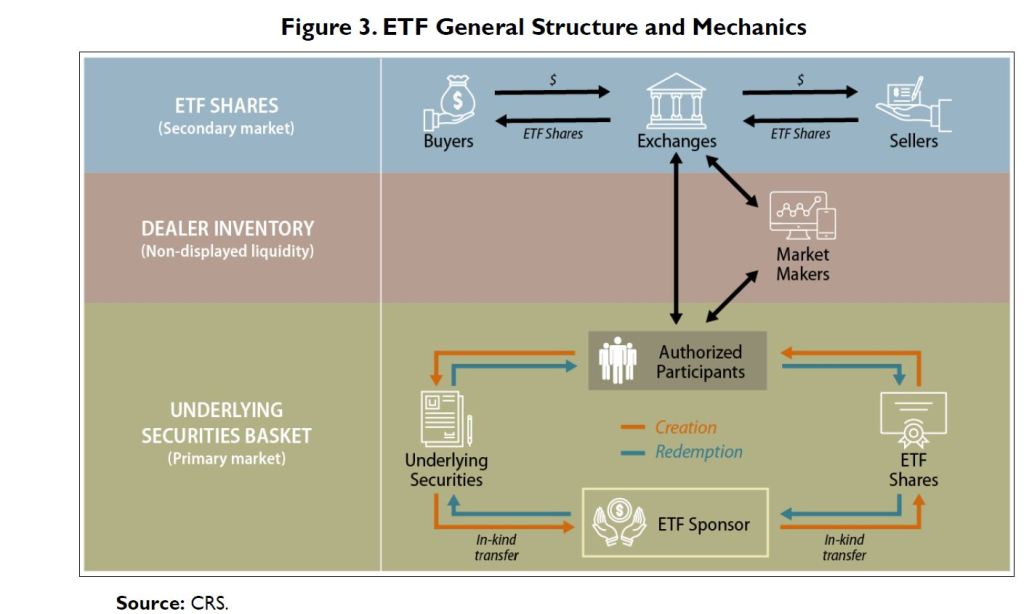

How the ETF ecosystem works

The structure and mechanics of ETFs are unique and different from mutual funds. Unlike mutual funds, ETFs generally don’t have to meet redemptions in cash. The key difference is the role of Authorized Participants (APs), and the arbitrage mechanism. The Congressional Research Service provides a handy diagram explaining the structure (Most fund sponsors have similar diagrams in their whitepapers) :

In a typical ETF creation process, the ETF sponsor would first publish a list of securities in an ETF share basket. The APs have the option to assemble and deliver the securities basket to the ETF sponsor. Once the sponsor receives the basket of securities, it would deliver new ETF shares to the AP. The AP could then sell the ETF shares on a stock exchange to all investors. The redemption process is in reverse, with the APs transferring ETF shares to sponsors and receiving securities.

ETF shares are created and redeemed by authorized participants in the primary market. The fund sponsors do not sell their ETF shares directly to investors; instead, they issue the shares to APs in large blocks called “creation units” that usually consist of 50,000 or more shares. The APs’ creation and redemption process often involves the purchase of the created units “in-kind” rather than in cash. This means that the shares are exchanged for a basket of securities instead of cash settlements. The supply of ETF shares is flexible, meaning that the shares can be created or redeemed to offset changes in demand; however, only authorized participants can create or redeem ETF shares from the sponsors. A large ETF may have dozens of APs, whereas smaller ETFs could use fewer of them.

The “arbitrage mechanism” is a key feature of the ETF ecoystem. The market incentivizes APs to correct supply demand imbalances for ETFs because they can always exchange underlying shares for the securities in the portfolio and vice versa. So theoretically ETFs should not end up with discounts or premiums to NAVs like closed end funds.

Additionally, since the ETF Sponsor can redeem in kind, rather than in cash, they don’t need to sell underlying securities to meet redemption requests, like with mutual funds. Additionally, unlike with mutual funds, you get some intraday price transparency. Sometimes media commentary on “illiquid assets in liquid wrappers” mixes these up, but the nuance is important to how the respective ecosystems will react to market turmoil.

The arbitrage mechanism is a huge benefit for ETFs, and it works pretty well for deep liquid markets, like large cap stocks. Yet with less liquid assets such as leveraged loans or high yield bonds, there is reason to worry. ETFs haven’t really solved the liquidity mismatch problem. Closely related, any understanding of market history leads us to conclude that APs are unlikely to function in a falling market.

Liquidity mismatch in ETFs

Theoretically if there is a flood of selling at ETF level, APs can buy from portfolio managers, then exchange for underlying securities. However what happens if there is no bid/ask for some or all of the underlying securities?

There are several large ETFs that consist of leveraged loans and high yield bonds. A retail investor can have instant liquidity in the ETF market, and theoretically if there is an imbalance in the secondary market APs will step in and exchange ETF shares for the underlying bonds and loans. Yet these underlying assets can go days without actually trading(they are “trade by appointment”) . ETFs may be a small percentage of all outstanding bonds/loans, yet there is very little turnover of these assets, and often its difficult to get pricing. Its not clear how the market would respond if there was a macro event that caused loan prices to gap down, and investors to seek redemptions from ETFs en masse. Prior to the last financial crisis, few ETFs held high yield bonds, and no ETFs held leveraged loans.

Some analysts assert that ETFs have become so large in certain markets that the underlying securities may no longer be sufficiently liquid to facilitate ETF creation/redemption activity during periods of stress and could result in price dislocations.

Consider a crisis scenario where selling pressure causes underlying assets (like fixed income securities) to become illiquid and rapidly lose value prompting ETF holders to quickly sell their shares. Here market makers and APs would likely widen their bid-ask spreads to “compensate for market volatility and pricing errors.” Increased fund redemptions in the primary market could also detrimentally change the composition of the underlying portfolio basket causing APs – who no longer want to redeem ETF shares and receive, in-kind, the plummeting and illiquid securities – to withdraw from the market altogether.

Also notable, post financial crisis regulatory changes caused bond dealers to hold less inventory. This can mean less liquidity in a crisis, as this recent academic paper notes:

When an extreme crisis hits, historically, OTC market liquidity disappears. That is, no one is available to take the other side of the trade. There are simply no bids, no offers, and no trading activity in OTC markets. The recent reduction in dealer inventories means that markets will be even more volatile in the next crisis.

This is unlikely to be a problem for deep liquid markets such as large cap stocks. So any problem with popular stock index funds is likely to be resolve itself quickly But it could take a long time to unwind problems in leveraged loan and high yield bond ETFs.

Won’t the APs fix this?

Its important to emphasize that the APs have no fiduciary duty to provide liquidity. The AP will have an agreement with the fund sponsor, but the fund sponsor does not compensate the AP directly. APs can profit by acting as dealers in the secondary market, or clearing brokers, thus collecting payment for processing and creation/redemption of ETF shares from a wide variety of market participants. APs can stop providing liquidity anytime they want. In the event of a crisis it may be prudent to do so. From Duke Law:

As such, a reliance on discretionary liquidity, in the context of a crisis is inherently “fragile” since dealers and market makers will stop providing it once they start incurring losses, or their balance sheets are negatively impacted from other exposures and they can no longer bear the additional risk from providing the liquidity support

In 2013 some ETFs traded at a steep discount when Citigroup hit its internal risk limits. That was in the middle of a great bull market. What will happen if there is a serious macro problem? As a historical precedent, during the financial crisis the auction rate security market collapsed when discretionary liquidity providers exited due to turmoil.

A different kind of death spiral

There are risks for both ETFs and Mutual Funds that hold illiquid assets. However the reasons are different, and the nuances of a blow up will be different.

A mutual fund can get exemptive relief from the SEC to suspend cash redemptions in extreme circumstances. Mutual fund investors, who thought they had a daily liquidity vehicle, are left holding an illiquid asset. This happened to the Third Avenue Focused Credit fund a couple years back. This caused a short lived mini-panic in the high yield debt market. When the fund suspended cash redemptions, they paid redemptions in shares of a liquidating trust. An outside party offered to buy the shares at a 61% discount to the NAV, which had already declined sharply.

In the case of an ETF it’s a bit more complicated. The death spiral could simply take the form of a self reinforcing feedback loop. Retail investors would be able to exit, albeit at a steep discount. APs would sell underlying securities that they can sell, causing prices to plummet, causing further retail panic. Some assets are more illiquid than others, and once once the dust settles, the ETF will be left holding the most illiquid and opaque assets.

During the past few years we’ve seen a few tremors. There was the short incident in 2013 mentioned above. In May 2010 and August 2015 there were large one day price swings in more liquid parts of the ETF market probably caused by algorithms. In February 2018 there was the great VIX blowup/ “volmageddon”. The VIX example was a bit different because it involved very unique derivatives, but I think the bigger more interesting problems could be in the credit space. In 2018Q4 there was some volatility in the credit space, and MSCI noted ETFs appeared to have a mild impact on bid/ask spreads. Yet by historical standards what happened in 2018Q4 was very minor.

These examples all occurred during a long bull market. What will happen in the next 2008 type scenario? I Still need to look more into how they might actually unwind.

So what can an investor do?

Most ETFs(and mutual funds) will probably be fine. During a crisis there might be temporary NAV discounts even for large cap index funds and lots of panic selling all around. Mutual fund investors will redeem at the worst possible time, and funds will sell shares into a falling market to meet these requests. Headlines will be full of doom and gloom. The prudent thing for most investors will be to ignore it all. Continue dollar cost averaging across the decades to retirement and beyond.

Nonetheless, investors holding some of the more esoteric, illiquid ETFs and mutual funds could be in for an unpleasant surprise and possible permanent capital impairment. Even though these potentially problematic funds are a small portion of the overall market, there is likely to be systemic contagion, as the IMF noted.

I’ve purchased some cheap puts on more fragile ETFs(mainly high yield bond and leveraged loan) although the lack of an imminent catalyst means that the position size needs to be small. I’ll be looking more closely at the way these different types of structures are unwound, since there are likely to be some major time sensitive opportunities next time it occurs.

Other possible case studies of the unwinding of illiquid assets in liquid wrappers:

UK open end commercial property funds during Brexit vote

Auction rate securities during financial crisis

Interval Funds during the financial crisis.

Other mutual fund redemption suspensions and ETF tremors?

Listening to Barakett talk about some of his wildest cases gives some idea of how easy it is for people to fall through the cracks during cursory due diligence. For example, on its website, DDC says it once found that “the president of a large U.S. asset manager was arrested twice for major art theft” but was never charged due to the expiration of the statute of limitations.

The art theft case was a “thing of beauty,” Barakett recalls. The manager, who still runs $2 billion, was even discovered to have one of the stolen paintings in his office when a police investigator went to interview him regarding the second theft. (The man was in college at the time of the thefts, which were from the university.) DDC’s client, a family office considering making a big investment, “could not believe what we were telling them,” Barakett says. It decided to walk away.

Another case involved a Bear Stearns executive whose murder conviction had previously gone undetected because, Barakett suspects, a casual background check either did not look at records in every state he had lived in or checked the wrong name or date of birth. “Our client [an asset manager who was considering hiring the man for an IR position] could not believe it, and we showed him the proof,” he recalls.

Vanguard has discussed licensing its hybrid ETF-mutual fund design to other firms, but no deal has come to fruition, according to people with knowledge of the talks. Those that have expressed interest included both index followers and active stock-pickers. United Services Automobile Association licensed the patent but never used it, and Van Eck Associates Corp. once sought regulatory approval for a similar design. Spokesmen for USAA and Van Eck declined to comment

Many managements probably revile their shareholders, but most of them do not publicly delight in doing so. Sardar Biglari and Phil Cooley, Chairman and Vice Chairman of Biglari Holdings, seem to delight in the annoyance of its shareholders. At one point laughing at them for being upset that the share price went down 58% last year and then subsequently watching the board increase Sardar’s compensation package. It is not my best-self that enjoyed this spectacle, it was more like the part of me that likes watching dragons fight dragons on Game of Thrones that was riveted by Sardar Biglari and Phil Cooley or the part of me that once saw two clowns get into a fist fight at a kid’s party in St. Petersburg and rather enjoyed it.

You get more of what you subsidize and less of what you tax. Unfortunately, the FDA is inadvertently taxing companies for being in the generic drug business. And it’s taxing them more if they’re not a monopolist with economies of scale. That means we get fewer companies in the generics industry, and more monopolists.

So my very tentative guess as to why buspirone is more plagued by shortages than bread or chairs is because number one, the need for FDA approval makes it hard for new companies to enter the buspirone industry, and number two, the FDA’s fee structure favors large-scale monopolies over small-scale competitors.

Legendary stock-picker Peter Lynch’s maxim to “buy what you know” has long been misconstrued to mean invest in the everyday products you consume. That’s not quite right, as it only reflects part of his investment strategy. The other half is buying what you have a unique insight into that the market has yet to figure out. Knowing what those things are is the hard part.

This is where the “Valeant problem” that is rarely discussed, becomes an issue for us: what to do with a position that rapidly increases in size relative to the rest of the portfolio and where Hahn Capital Management and Sequoia/Value Act approaches to the matter differed. While the latter funds continued to hold, and allowed the single position to become almost a third of their portfolio, Hahn Capital had strict risk controls and processes in places that forced them to sell down the position to at least 4% of the portfolio when it became 6% of the portfolio’s weight. Luckily for Hahn, they exited the position prior to the spectacular blow up while the other aforementioned funds suffered significant double-digit portfolio losses when the truth about Valeant’s practices became public. Of course that is not to take away from the spectacular track records of all of the aforementioned funds, but to point out how different investment strategies (concentrated versus diversified), portfolio manager incentives (Management Fee Only versus Performance Carried Interest), and risk control processes (on single position sizes) can result in very different portfolio returns and risk profiles for different shareholders of the same stock. To put another way, sometimes a sell decision is not one of security analysis but one of portfolio risk management and fund strategies. As a result of this, and other similar experiences throughout our career, we have tried to approach the middle ground of the two styles by having a strong degree of concentration and conviction in our portfolio while still maintaining a robust portfolio risk management process focusing on capital preservation, position size, and its risk-reward ratio relative to the rest of the portfolio.

Additionally, we believe the other lesson to be learned from Valeant was no matter how high of a conviction, knowledge base or confidence you have in a publicly traded company or its management, at the end of the day things can and occasionally do go unpredictably wrong and are out of your control. This is a staple of public equities investing and is a common mistake made by even the most reputable investors: having the illusion of control.

How has this profession lasted so long? The industry’s longevity is largely attributable to financial technology (FinTech), which has historically empowered advisers to better serve their clients. Many companies, for example, offer advisers quantitative and accurate measurement of investors’ risk tolerance. Equipped with this technology, advisers have a better sense of how clients will respond to volatility, and can construct portfolios that most accurately reflect a client’s ability to endure market swings.

The ticker technology served as a means for democratizing access to market information. Prior to its invention, only those physically present at the stock exchange – or very close by – were privy to real-time market prices. Everyone else received their data at a substantial lag, often to the point where it was no longer useful. Once the ticker was released, however, cables and telegraphs connected brokers across the country to a network of data constantly flowing from a central source, the New York Stock Exchange. According to Horace Hotchkiss, 23,000 offices paid for ticker services in the United States

In Defense of Complexity Most people are knee jerk advocates of simplicity, but forget what lies beneath.

But simple is impossible without complex. Simple is how you interact with your web browser or an app on your phone. Complex is everything else happening in the background that allows it to function.

There are some valuable and diversifying asset classes that routinely get discarded to the “Too Complex” pile for reasons related to ambiguous classification, unfamiliar tools, novel wrappers and peer/career risk. Which is unfortunate, because I would argue that certain alternative investments are complex in implementation only. Conceptually, they are often quite simple, intuitive, backed by data and grounded in economic theory. The arc of the investable universe is long, and it bends towards democratization and innovation. Not every shiny new toy deserves a spot in your portfolio, but it would be wise to reconsider exactly what constitutes simplicity in investing.

You read in every textbook that cliché: Power corrupts. In my opinion, I’ve learned that power does not always corrupt. Power can cleanse. When you’re climbing to get power, you have to use whatever methods are necessary, and you have to conceal your aims. Because if people knew your aims, it might make them not want to give you power. Prime example: the southern senators who raised Lyndon Johnson up in the Senate. They did that because he had made them believe that he felt the same way they did about black people and segregation. But then when you get power, you can do what you want. So power reveals. Do I want people to know that? Yes.

…. There’s always something the other guy doesn’t want to tell you, and the longer the conversation goes, the easier it is to figure that out

The one thing we haven’t had mercifully over the last 60 year except for the breakdown of Yugoslavia, and Iraq and so on is a major confrontation between big powers wanting to escalate.

While there is a long and lamentable history of science — physics in particular — being hijacked for mystical and New Age ideologies, two things make Jung and Pauli’s collaboration notable. First, the analogies between physics and alchemical symbolism were drawn not only by a serious scientist, but by one who would soon receive the Nobel Prize in Physics. Second, the warping of science into pseudoscience and mysticism tends to happen when scientific principles are transposed onto nonscientific domains with a false direct equivalence. Pauli, by contrast, was deliberate in staying at the level of analogy — that is, of conceptual parallels furnishing metaphors for abstract thought that can advance ideas in each of the two disciplines, but with very different concrete application.

Philosophy is, in part, kept alive by ever-changing sociocultural circumstances that demand new lived responses to its question. But the changes brought by the digital age are of a magnitude beyond the routine vicissitudes of history. The global distribution of knowledge is arming, perhaps overloading us with more information than ever before, and the proliferation of digital interfaces is reprogramming how we experience life itself, our attentive and perceptual faculties.

…What I’m getting at is the possibility that the basic human conundrum is no longer driven by a deficiency in discovery, but in design. That now more than ever, we’re equipped with the information needed to live well, but aren’t integrating that information into our daily routines, our lived realities. There’s a lag between what we’re discovering and how we’re living.

The flood of information made available through the internet filled the discovery container with more than it can hold. We’re spilling things, getting the fabric of human life all wet. These moments of imbalance are when priority shifts from discovery to design. At these points, the work falls upon those positioned between the two containers, using what we’ve discovered to imagine and implement new designs, to convert influxes of knowledge into wisdom that can be embedded into the internal logic of our ecologies, enriching the relational environments from which our sense of being is woven.

In other words, the singularity got cancelled because we no longer have a surefire way to convert money into researchers. The old way was more money = more food = more population = more researchers. The new way is just more money = send more people to college, and screw all that.

But AI potentially offers a way to convert money into researchers. Money = build more AIs = more research.

If this were true, then once AI comes around – even if it isn’t much smarter than humans – then as long as the computational power you can invest into researching a given field increases with the amount of money you have, hyperbolic growth is back on. Faster growth rates means more money means more AIs researching new technology means even faster growth rates, and so on to infinity.

Presumably you would eventually hit some other bottleneck, but things could get very strange before that happens

Our belief is that stocks should be viewed not as “growth” or “value” opportunities, but rather from the perspective of whether the market is efficiently valuing their future earning prospects.

…

Marathon’s approach is to look for investment opportunities among both value and growth stocks, as conventionally defined. They come about because the market frequently mistakes the pace at which profitability reverts to the mean. For a “value” stock, the bet is that profits will rebound more quickly than is expected and for a “growth stock,” that profits will remain elevated for longer than market expectations.

…

Marathon looks to invest in two phases of an industry’s capital cycle. From what is misleadingly labelled the “growth” universe, we search for businesses whose high returns are believed to be more sustainable than most investors expect. Here, the good company manages to resist becoming a mediocre one.From the low return, or “value” universe, our aim is to find companies whose improvement potential is generally underestimated. In both cases, the rate at which a company reverts to mediocrity (or “fade rate”) is often miscalculated by stock market participants. Marathon’s own experience suggests that the resultant mispricing is often systematic for behavioural reasons.

…

Labelling fund managers as “value” or “growth investors risks distorting the investment process

…most analysts feel they must choose between two approaches customarily thought to be in opposition: “value” and “growth.” Indeed, many investment professionals see any mixing of the two terms as a form of intellectual cross- dressing.

We view that as fuzzy thinking (in which, it must be confessed, I myself engaged some years ago). In our opinion, the two approaches are joined at the hip: Growth is always a component in the calculation of value, constituting a variable whose importance can range from negligible to enormous and whose impact can be negative as well as positive. In addition, we think the very term “value investing” is redundant. What is “investing” if it is not the act of seeking value at least sufficient to justify the amount paid? Consciously paying more for a stock than its calculated value – in the hope that it can soon be sold for a still-higher price – should be labeled speculation (which is neither illegal, immoral nor – in our view – financially fattening).

Whether appropriate or not, the term “value investing” is widely used. Typically, it connotes the purchase of stocks having attributes such as a low ratio of price to book value, a low price-earnings ratio, or a high dividend yield. Unfortunately, such characteristics, even if they appear in combination, are far from determinative as to whether an investor is indeed buying something for what it is worth and is therefore truly operating on the principle of obtaining value in his investments. Correspondingly, opposite characteristics – a high ratio of price to book value, a high price-earnings ratio, and a low dividend yield – are in no way inconsistent with a “value” purchase.

Similarly, business growth, per se, tells us little about value. It’s true that growth often has a positive impact on value, sometimes one of spectacular proportions. But such an effect is far from certain….

…Growth benefits investors only when the business in point can invest at incremental returns that are enticing – in other words, only when each dollar used to finance the growth creates over a dollar of long-term market value. In the case of a low-return business requiring incremental funds, growth hurts the investor.

Growth vs. value is a false dichotomy, but it might be a useful heuristic for organizing a portfolio. With a “value” investment, you are buying assets, and betting on a reversion to the mean. Generally this means other people are overestimating the bleakness of the future. With a “growth” investment you are buying the future business, betting on change. Generally this means other people are underestimating the brightness of the future.

The key is having an intellectually honest variant view.

Venture capital and value investing

In a similar vein, its easy to see how venture capital and value investing are actually quite similar. Both are mispriced bets on the probability of change.

Venture capital and value investing share many different elements but each system is based on a different mispricing. This is a critically important point for an investor to understand. If an asset is not mispriced, market outperformance is not mathematically possible. It is also important to understand that investments can be mispriced for different reasons.

In venture capital the mispricing occurs because very few investors or asset owners understand optionality. This allows a VC to buy what are essentially long-dated, deeply-out-of-the-money call options from companies at prices which are a bargain.

…

In value investing the mispricing occurs because the market is bipolar (i.e., neither always rational nor always efficient). This allows an investor to sometimes buy assets at a price which reflects a discount to intrinsic value (i.e., a bargain) and to wait for a good result rather than trying to “time” the market.

… every time I hear a story like See’s Candies, I want to go find the new scientific superfood candy company that’s going to blow them right out of the water. We’re wired completely opposite in that sense. Basically, he’s betting against change. We’re betting for change. When he makes a mistake, it’s because something changes that he didn’t expect. When we make a mistake, it’s because something doesn’t change that we thought would. We could not be more different in that way. But what both schools have in common is an orientation toward, I would say, original thinking in really being able to view things as they are as opposed to what everybody says about them, or the way they’re believed to be.”

A decent portfolio has a combination of mean reversion bets, and underpriced deep out of the money options. It pays to be an intellectual cross dresser

In the past I have been a knee jerk advocate of disintermediation. However upon closer examination I realized that the reality of middlemen is far more nuanced. Many people believe that modern technology is eliminating middleman, yet in fact their role is changing shape, not disappearing. In the Middleman Economy , Marina Krakovsky examines this aspect of the modern economy. The Private Investment Brief has also produced valuable analyses of middleman business models. Additionally, Michael Munger’s paper puts this all into a historical context with emphasis on the importance of reduced transaction costs.

Conventional wisdom says that middleman take a cut of every deal, so they raise buyer costs and reduce seller profits. In reality by facilitating transactions that would otherwise not happen at all, good middlemen enlarge the size of the pie, making all parties better off. Many people assume that middlemen’s work is easy because they don’t actually create anything. But to create value… good middlemen must cultivate distinct skills and practices, which they deploy in work that until now has been largely hidden from public view…

“Instead of the of the demise of the middlemen, we are seeing the rise of the middleman. In fact , ours is more than ever a middleman economy.”

There seems to be a gap between public perception and market reality. Therein lies the opportunity:

And yet—thousands of years after it first occurred to someone to ask “why don’t they just cut out the middleman?”—middlemen continue to exist and even thrive. Therein lies the opportunity, for if we can learn to appreciate what others dismiss or misunderstand, we might then have an investing green field all to ourselves

Indeed, Michael Munger takes it even further and argues that we are experiencing a profound historical shift that will alter capital allocation incentives across the economy:

The Neolithic revolution made it possible for humans to enter complex relations of more or less voluntary dependence, and to share economies of organization and information. The Industrial revolution created an astonishing burst of productivity, which made ownership of a bewildering variety of commodities and tools possible for all but the poorest of people, where just 50 years before such items would have denied all but wealthiest. The Middleman revolution, the third revolution whose leading edges we are now crossing, will transform owning into sharing. The Middleman revolution will make it possible, for the first time, for entrepreneurs to create value almost exclusively by reducing the transactions costs of sharing existing commodities, or by sharing commodities or services made expressly to be shared by the new platforms and new market processes.

In a world where buyers and sellers can just find each other online quickly and easily, middleman must be obsolete, right?

… Wait a minute…

Often when people talk about cutting out the middleman, they are actually just replacing it with a new middleman. All the aggregator platforms are in fact distinct breeds of middlemen whose businesses are made possible by the internet. Examples include: Airbnb, Lyft and Uber, Taskrabbit, Grubhub, ZocDoc, etc. Instead of a person, buyers and sellers deal with software on a website that is developed and managed by people. As Krakovsky points out:

In many ways, the internet is a middleman’s ally. Thanks to the internet, middlemen who used to do business in person — a position that limited their geographic reach can a attract customers from all over and can share information with them more quickly and easier than ever…

…

These days, two sided markets (sometimes called two-sided networks or two sided platforms ) are everywhere because many of today’s internet startups are middlemen business of exactly this type

Understanding middleman requires multidisciplinary thinking. There isn’t really one accepted definition, and there are many different angles from which to analyze how this social and economic phenomenon works:

Economic theory has much to say about transaction-cost economics, two sided markets, and intermediaries ability to reduce information asymmetries between buyers and sellers. In particular, game theory informs our understanding of repeated interactions, reputation, shirking and cheating, and third party enforcement. Social psychology and experimental economics show how acting on behalf of others affect people’s behavior and impressions. And sociology offers insights into the way acting on behalf of others affects people’s behavior and impressions. And sociology offers insights into the ways the structures of social networks create opportunities for middlemen

Six kinds of Middlemen

Krakovsky identifies five different roles that middleman can play. These roles define what middleman’s trading partners expect, so its critical for a middleman to know what role they play, and do play it well. They often overlap, so a successful business may fill of these roles at different times in the same supply chain.

Bridge

A bridge promotes trade by reducing distance(either physical, social or temporal). RA Radford’s study on the development of a market in a WWII POW camp is a stark example. An itinerant priest was willing to connect disparate groups who did not interact, facilitating trade along the way.

Another example featured in the New York Times and highlighted by Private Investment Brief involves an Afghanistan based used clothing wholesaler who makes an annual trip to Pakistan to buy bulk clothing. He is able to succeed for many reason, one of which is the fact that he reduces the fixed costs of dealing with travel, customs, logistics, etc.

Certifier

A certifier gives reassurance about underlying quality. This is important anywhere there is need for a trusted third party. Essentially, they help fix information asymmetry in a market. That same clothing wholesaler who facilitated trade between Pakistan and Afghanistan was also known as a trusted counter party to disparate group of buyers and sellers.

Trust is an elusive and intangible quality, so those of us in the more contemplative, analytical corners of the business world tend to underestimate how important it is to people transacting day to day

An enforcer makes buyers and sellers cooperate and stay honest. Like certifiers, they are important in situations where there is need for a trusted third party. My favorite example of an enforcer is the role of a pimp at a truck stop in Uganda.

Risk Bearer

A risk bearer reduces fluctuations. Micro VCs play this role, especially now that technology has drastically reduced the cost of starting businesses. “Uber for this or that” business models are an example of a risk bearer business model. Additionally in the Japanese fish markets, risk bearing middleman ensure smooth functioning of trade in a highly perishable commodity.

Concierge

A concierge reduces hassles and helps clients deal with information overload. For example, travel agents, in spite of widespread predictions of their demise, play a critical role in high end business travel as concierge middlemen.

Insulator

An insulator helps clients get what they want without being though of as too greedy, self promotional, or confrontational. Sports agents help defuse tensions between players and teams. Additionally, sometimes an investor will use a broker to build up a position without signalling the market. This may be essential in distressed and illiquid securities, or disputed situations.

Transaction costs

Munger looks at markets in the broad sweep of history. The role of technology, he argues, is in creating a new “entrepreneurial revolution” that makes middleman more important in an an economy based on sharing, not owning.

The third entrepreneurial revolution will be based on innovations that reduce transactions costs, not the costs of the products themselves. An unimaginable number and variety of transactions will be made possible by software platforms that make renting from a middleman, rather than renting from one’s self, cheaper.

A former student of Douglass North, Munger emphasizes the transaction cost angle throughout:

To succeed, a middleman has to reduce three key transactions costs: • Provide information about options and prices in a way that is searchable, sortable, and immediate • Outsource trust to assure safety and quality in a way that requires no investigation or effort by the users • Consummate the transaction in a way that is reliable, immediate, and does not require negotiation or enforcement on the part of the users

The Dawn of Eurasia: On the Trail of the New World Order is a fascinating analysis of the shifting geopolitical landscape. The author, a former Secretary of State for European Affairs for Portugal, mixes a travelogue with discussions of history, literature, and economics. Eurasia is not just a geographical entity, but rather a “descriptive term for a certain way of thinking about a new moment in political history”. It expresses a world order that is the integration of two ideas often seen as contradictory being brought together into a single word.

The rise of the east

Many people wrongly assume that the world will converge on a social organization that is based on western ideals. Instead different societies are adapting and iterating based on their own historical experiences and present circumstances. The dominant cultures of the future may be organized in a very different manner than what we are used to:

On the one hand, it conveys the sense that the European order has come to an end. This moment, so often announced, has been, on the contrary, persistently evaded. When European countries abandoned their imperial dreams, they did so under the illusion that the rest of the world no longer needed guidance because it had voluntarily embraced European rules and ideas. It was an illusion, but an illusion that only now is being revealed as such. On the other hand, this should not be confused with the belief that Europe’s legacy has likewise been abandoned. What we see is that those who are more actively working to replace the old world order with something are just the heirs of the European scientific and revolutionary traditions,. When competing with the European model, they try to present an alternative that is more modern, more rational, better able to lead the transformations of the future. Theirs are new an alternative visions of what a modern society looks like.

The west is merely a reference point: