Category: Investing

The Paradox of Alternative Data

“My God, they’re purple and green. Do fish really take these lures?” And he said, “Mister, I don’t sell to fish.

Informational edge can drive fantastic alpha while it lasts. This explains the increasing investment industry focus on non-traditional data sources, aka alternative data. If you are the first to acquire a new alternative data set, you might be able to develop insights no one has.

Yet once a lot of people are using it, it is less likely to drive alpha. It might be table stakes to not get screwed, or it might be already be instantaneously reflected in the price of assets.

Furthermore, most opportunities really hinge on a couple factors- more info isn’t always useful. That won’t stop the alternative data industry from doubling to $400 million by 2021, as a widely cited Tabb Group report predicts This is worth considering while one is caught up in an alternative data arms race.

Yet some data sets genuinely will provide an edge.

Perhaps a data set that no one else is looking at provides the edge you need. If a data set isn’t established as useful, the provider of that data will probably offer it cheaper in the early days of their business. There are so many alternative data providers out there, that marketing strategy is important for startups.

Ironically, the provider can charge higher price once word about its value gets out among investors.. So later adopters might pay more for an edge that is already gone.

Of course eventually someone will put all the data online for free and meta data of how investors use that alternative data can also be useful.

Now can I interest you in an alternative data feed that will make all your dreams come true?

See also: https://ockhamsnotebook.wordpress.com/2016/09/18/the-hard-thing-about-finding-easy-things/

The ecological consequences of hedge fund extinction

Investing goes through fads. Investing strategies and fund structures(1) go in and out of style. Nowadays long/short hedge funds are out and infrastructure funds are in. Within the public equity markets, value is out, growth/momentum is in. Each time this happens, people forget how the cycle repeats.

In fact, one CIO contended that if he brought a hedge fund that paid him to invest to his board, the board would dismiss it without consideration — simply because it’s called a hedge fund, and hedge funds are bad.

Institutional Investor

Hedge funds may have to do a name change if they want to raise capital.

Remember last time?

And yet people forget:

Allocators woke up craving the next rising hedge fund star and couldn’t invest enough at high and increasing management fees after the widespread success of long-short funds in the weak equity markets of 2000-2002. Board rooms back then castigated CIOs for not having long-short equity hedge funds in their portfolios.

This isn’t the first time:

People forget that 40 years ago, officials such as Paul Volcker of the Federal reserve wanted an active hedge fund industry to absorb the risk that was not well managed by state-insured banks.

Financial Times

Each investment strategy picks up a certain type of risk(and potentially earns a profit in doing so)- if a strategy disappears that particular risk can become a systemic issue. Fortunately, around this time it also becomes more lucrative to bear the risk others are unwilling to bear. Eventually the risk reward tradeoff starts to make sense again.

Different, different, yet same

In the 1960’s Warren Buffett put up ridiculous returns, and Alfred Winslow Jones proteges profitably exploited anomalies in markets. By the mid 1970’s of there were many articles about hedge funds shutting down though. Industry AUM declined ~70% peak to trough. Nifty fifty boom and bust followed by the long nasty bear market. But as the institutional architecture of international trade and currency shifted we entered glory years of global macro/commodities traders. Then the 80’s were great for Graham deep value and Icahn style activist investing after the 70’s bear market left a huge portion of the market selling below liquidation value.

Likewise late 90’s again saw the death of hedge funds as day traders in pajamas earned easy returns from the latest dot-com- until the crash. Yet out of the rubble of the tech bubble rose a new generation of great hedge fund managers. There was rich pickings for surviving value hunters- and those with the guts and skills to execute became household names a few years later. Many value managers that nearly went out of business during the tech bubble put up ridiculous numbers 2000-2002 and through the next financial crisis. (See: The arb remains the same)

The greatly exaggerated death of a style gives rise to an environment where there is a plethora of opportunities for something similar to that style to work. Each time the narrative in the greater investment community favors some type of uniform strategy, and LPs give less capital to other strategies- causing them to nearly die off. But then the lack of people pursuing the out of fashion strategy makes its return potential more lucrative. Eventually someone finds a new method to pick up those dollar bills on the ground that shouldn’t exist.

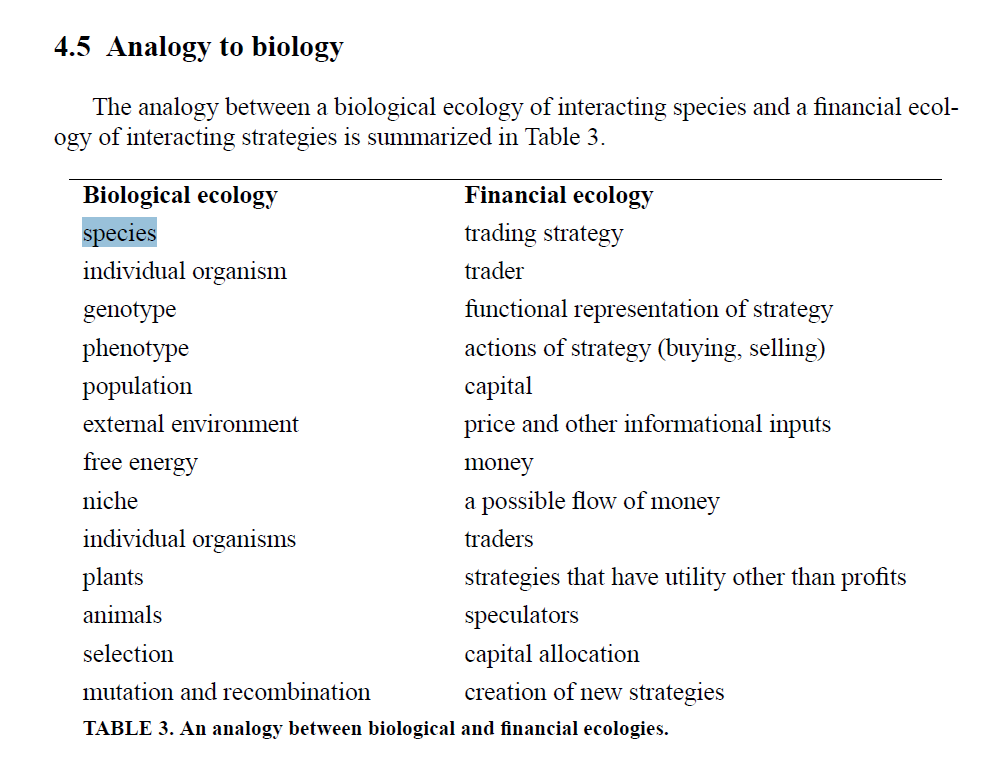

Economics emphasizes rational actors and equilibrium. Yet the messy reality is far more complicated. Ecology is a far more useful mental model.

A giant self over-correcting ecosystem

There is in ecological function to speculative capital and over time there should be some excess returns to those willing to take mark-to-market losses

Financial Times

Like biological species, financial strategies can have competitive, symbiotic, or predator-prey relationships. The tendency of a market to become more efficient can be understood in terms of an evolutionary progression toward a richer and more complex set of financial strategies.

Market force, ecology and evolution

Ecology emphasizes interrrelationships between different individuals and groups within a changing environment, and indentifies second order impacts.

Thinking like a biologist

One can develop a useful framework by replacing species with strategy, population with capital, etc

Flows and valuation interact, self correct, and overshoot.

….capital varies as profits are reinvested, strategies change in popularity,and new strategies are discovered. Adjustments in capital alter the financial ecology and change its dynamics, causing the market to evolve. At any point in time there is a finite set of strategies that have positive capital; innovation occurs when new strategies acquire positive capital and enter this set. Market evolution is driven by capital allocation.

Market evolution occurs on a longer timescale than day-to-day price changes. There is feedback between the two timescales: The day-to-day dynamics determine profits, which affect capital allocations, which in turn alter the day-to-day dynamics. As the market evolves under static conditions it becomes more efficient. Strategies exploit profit-making opportunities and accumulate capital, which increases market impact and diminishes returns. The market learns to be more efficient.

Evolution

When an ecoystem is overpopulated with a certain species, it eventually overshoots and results in mass starvation. Populations fluctuate wildly across decades, and sometimes species go extinct or evolve into something that seems new.

New conditions give rise to new dominant species.

See also:

George Soros on disequilibrium analysis

The arb remains the same

Book:

Investing: The Last Liberal Art

Hedgehogging

More Money than God

(1) Although I am frequently pedantic about the differences between structure, strategy, and sector, many in the media seem to use these interchangeably when discussing reversion to mean situations. Fortunately they all exhibit the same boom/bust phenomenon, so I am using them interchangeably here.

The arb remains the same

Imagine if Warren Buffett of 1960 puts down the deadtree 10-K he got in the mail and time travels forward to 2019. Then he looks over the shoulder of an analyst at present day O’Shaughnessy Asset Management. He would find the scene unrecognizable.

Or, if the original Jesse Livermore time traveled from the 1920s stock exchange to the present day trading floor of DE Shaw or Renaissance. Again, completely unrecognizable.

Back in the day people went to the SEC office in the Washington DC to access annual reports faster. That was how one got a fundamental edge. Now people scrape filings the minute they come out. Or use satellites and credit card data to get an edge on information before it hits regulatory filings. People used to gauge momentum by looking at the facial expressions of other traders, now they use complex computer models. People mine market and fundamental data around the globe looking for a bit of an edge. New techniques, same thing.

Over time there is the change in the physical activities, and words we use to describe the process of identifying and exploiting market inefficiencies. Nonetheless the ecological function is the same. Investors are just looking for mispriced risk, and exploiting it till its no longer mispriced.

Around the world there are unfair coins waiting for someone to flip them. Arbitrageurs will need to use weirder and weirder methods to find and exploit them. Methods change, but the arb remains the same.

See also:

The hard thing about finding easy things

Riches among the ruins

Cheap stuff and cheap capital

Two main factors drive an upsurge in entrepreneurship: cheap stuff and cheap capital. Cheap stuff is primarily a long run secular trend. Cheap capital is cyclical.

By cheap stuff I mean the inputs to a business, mainly technology. This has gone consistently down over time. One can build a website or an app for a few thousand dollars that is better than what they could have done for millions of dollars a decade ago.

Even if capital becomes scarce, cheap stuff will still be a positive factor driving entrepreneurship.

By cheap capital I mean the flood of venture capital. This is primarily cyclical. Consider this quote:

“There’s so much money chasing these deals that venture capitalists are in competition with each other. They spend their energies marketing themselves instead of screening the deals. It’s gotten silly”

Think it applies today? Or maybe to the late 1990s tech boom? This quote is from the WSJ in 1981, and referenced in this excellent article about 1980s venture capital.

During a boom its easy for most ideas to raise capital, regardless of business viability(as long as they fit with theme of the times). Indeed they can keep raising rounds in hopes of a profit decades in the future. After a bust its hard to raise capital, even for a great idea. Entrepreneurs need to bootstrap and get revenue a soon as possible.

Right now it seems there is a ton of venture capital financing companies that are losing money.

Cheap stuff and cheap capital are partly entangled. You might be reading this from within a WeWork. If they couldn’t keep raising cheap capital you think your rent is going to stay the same? Or maybe you are building a business on top of a money losing social media platform, or somehow benefiting from a thriving open source ecosystem. On the other hand, its harder to source talent when there is a flood of capital, and certain commodity based goods can have their own production cycle. Yet you can run your business from a garage and the new inventions of the latest venture boom aren’t going away.

Which is most important- cheap stuff or cheap capital ? I don’t know, but we’ll get to find out when this cycle turns. Creative entrepreneurs will still take advantage of technological improvements to bootstrap groundbreaking ideas, even if they can’t raise venture capital. Sometimes they do it out of choice, other times they do it out of necessity.

Once this cycle turns, we’ll go through a few years where most new businesses have no choice but to bootstrap.

This idea generally applies across all industries, not just venture funded. However in commodity based industries the cyclicality functions differently. Cheap capital often leads to inflation in hard assets. See also: Capital Returns: Investing Through the Capital Cycle

Thinking and Applying Minsky

Hyman Minsky developed a framework for understanding how debt impacts the behavior of the financial system, causing periods of stability to alternate with periods of instability. Stability inevitably leads to instability. Minsky identified three types of financing: Hedge financing, speculative financing, and ponzi financing. It seems some people only remember Minsky every so often when there is a financial crisis, but the framework is useful in all seasons.

Hedge Financing

An asset generates enough cash flow to fulfill all contractual payment obligations. For example, a conservatively leveraged rental property that generates enough rent to pay down the entire mortgage over time, regardless of the change in quoted property prices. Or a company that issues some bonds, then pays them back using cash flow from the business Generally hedge financing units have a lot of equity down. Even a market crash, will not cause an investor to suffer permanent capital impairment if they only use hedge financing. The equity holder who uses hedge financing will never depend on the capital markets.

Speculative Financing

An asset generates enough cash flow to fulfill all debt payments, but not the full principal amount. In this case debt must be rolled over, or the asset must be sold, in order to pay back the full amount. For example, a rental property financed with some sort of balloon payment structure that generates enough cash flow to pay off mortgage payments up until the balloon payment at the end. When the balloon payment comes due, the investor must roll over the debt or sell the asset. An investor ttat uses speculative financing is dependent on capital markets. If there is a delay or a problem in refinancing, they could lose their investment.

Ponzi Financing

This is basically “greater fool” investing. Ponzi financing means there is so much leverage n an asset, that the investment must be refinanced, or sold at a higher price quickly, otherwise the entire investment is lost. Sometimes property purchases will be financed with shorter term bridge loan. If the bridge loan can’t be refinanced with longer term mortgage, the investor is out of luck. Towards the end of the market cycle, many companies will be issuing bank loans or bonds that can only be repaid by refinancing. If their unable to refinance, they go bankrupt.

Use of ponzi financing means the investor is highly dependent on capital markets. The slightest disruption in capital markets or change in interest rates/inflation results in a large capital loss.

Junk bonds are not inherently bad. A higher interest rate can in many cases compensate for greater risk, especially across a portfolio of non correlated investments. Howeve, duringthe junk bond era, many companies

Similarly securitization is not inherently bad. It can allow capital to flow more effeiciently. But often banks would end up aggressively securitizing, with the need to sell the loans they made quickly. But if they weren’t able to resell they couldn’t hold the loans. This happened to Nomura during the Asian financial crisis, as vividly told in this Ethan Penner interview.

Ponzi in this case is not illegal activity, just extremely risky. Of course those investors who finance their activities ponzi style often end up feeling the need to commit illegal acts. The Minsky Kindleberger model is useful here.

The cycle repeats

During a recession is very difficult to get any debt financing that is not “hedge financing”. Lenders are scarred from the last cycle, and there is a paucity of available risk capital. But a price rise, and investors get more comfortable, more and more financing becomes ponzi units In fact. Lenders may lower their standards and become more accepting of ponzi units.

Throughout the market cycle, more and more financing is ponzi units. Eventually there is no greater fool to sell to. When many ponzi units are forced to sell at once, it eventually leads to a collapse in values. This is how stability inevitably leads to stability. The cycle repeats.

How to apply this?

To protect my capital, I look try to mainly expose myself to hedge financing, with a small amount of speculative financing. I position my portfolio so that I don’t need to refinance anything or sell anything in a rush. When I invest in leveraged companies with speculative or ponzi financing, I make it small position(always in some sort of limited liability structure), and generally won’t average down much if at all. Additionally, when I notice an increase in ponzi financing in the markets, I become more cautious.

Leverage, like liquor , must be consumed carefully if at all.

See also:

What Private Equity Has In Common with Renaissance Charlatans

No man need despair of gaining converts to the most extravagant hypothesis who has art enough to represent it in favorable colors.

-David Hume

Sometimes the private equity industry reminds me of travelling charlatans in late Renaissance Europe. I recently reread Robert Greene’s The 48 Laws of Power, and realized that Law 32 “ Play on People’s Fantasies” must be the guide some people use to draft fund pitchbooks.

( I refer to“Private Equity” or “PE” , but the same general logic applies to the entire alternative investments industry. This includes venture capital, some hedge funds, non-traded REITs, etc. )

PE funds have long term lock ups. The lack of mark to market smooths out volatility. It looks nice on a statement to see something holding steady as markets tank. There can be good reasons for long lockups. Many investments genuinely take a long term to workout. Most short term price fluctuation in the public markets is noise that some find hard to ignore. Warren Buffett once remarked that he bought stocks with the idea that public markets could close for a decade, and it wouldn’t bother him. But often unscrupulous fund managers use questionable marketing techniques and exploit the ability to keep money locked up for a long time.

Marco Bragadino, Private Equity Fund Manager

Often allocators or wealthy individuals will seek out private equity and other alternative investments because of frustration with public markets. Maybe the mark to market volatility has been painful. Perhaps the index funds squeezed all the alpha out of the markets. Maybe they feel that better connected people have access to investments. If only they also had access they too could grow their wealth for multiple generations. Plus they might have something to brag about at cocktail parties or in the nursing home.

Similarly, Marco Bragadino, or Il Bragadino was a famous Charlatan who first targeted Venice in the late 1500s, a time that the city was gripped with the feeling that its best days were behind it. The opening of the “New World” transferred power to the Atlantic Side of Europe. Venice struggled to keep up with the Spanish, Portuguese, Dutch, and English. Worse yet, The Turks were making incursions into Venice’s mediterranean possessions.

Now noble families went broke in Venice, and banks began to fold. A kind of gloom and depression settled over the citizens. They had known a glittering past — had either lived through it or heard stories about it from their elders. The closeness of the glory years was humiliating. The Venetians half believed that the goddess Fortune was only playing a joke onthem, and that the old days would soon return. For the time being, though, what could they do?

Exclusivity

Many alternative asset managers claim to have proprietary models, and tend to give of an air of exclusivity. Madoff, who managed a fraudulent hedge fund, was an extreme example of this. If only investors have the right “access”, they too can get exposure to that magic investment. This is right out of Il Bragadino’s playbook:

In 1589 rumors began to swirl around Venice of the arrival not far away of a mysterious man called “II Bragadino,” a master of alchemy, a man who had won incredible wealth through his ability, it was said, to multiply gold through the use of a secret substance. The rumor spread quickly because a few years earlier, a Venetian nobleman passing through Poland had heard a learned man prophesy that Venice would recover her past glory and power if she could find a man who understood the alchemic art of manufacturing gold. And so, as word reached Venice of the gold this Bragadino possessed — he clinked gold coins continuously in his hands, and golden objects filled his palace — some began to dream: Through him, their city would prosper again.

Modern asset managers are known for having well scripted due diligence meetings that leave investors with a feeling of awe and urgency. Il Bragadino did this too:

Members of Venice’s most important noble families accordingly went together to Brescia, where Bragadino lived. They toured his palace and watched in awe as he demonstrated his gold-making abilities, taking a pinch of seemingly worthless minerals and transforming it into several ounces of gold dust. The Venetian senate prepared to debate the idea of extending an official invitation to Bragadino to stay in Venice at the city’s expense, when word suddenly reached them that they were competing with the Duke of Mantua for his services. They heard of a magnificent party in Bragadino’ s palace for the duke, featuring garments with golden buttons, gold watches, gold plates, and on and on. Worried they might lose Bragadino to Mantua, the senate voted almost unanimously to invite him to Venice, promising him the mountain of money he would need to continue living in his luxurious style — but only if he came right away.

But look at that Sharpe Ratio!

Some private equity fund managers will claim a superb track record without ever having an exit. Sometimes legacy funds will be valued higher, but fail to provide any cash flow. Sometimes those legacy funds work out, but sometimes are actually complete disasters and the manager is delaying the inevitable reckoning.

Again, this is something they could have learned from Il Bragadino:

Bragadino had only scorn for the doubters, but he responded to them. He had, he said, already deposited in the city’s mint the mysterious substance with which he multiplied gold. He could use this substance up all at once, and produce double the gold, but the more slowly the process took place, the more it would yield. If left alone for seven years, sealed in a cas-

ket, the substance would multiply the gold in the mint thirty times over. Most of the senators agreed to wait to reap the gold mine Bragadino promised. Others, however, were angry: seven more years of this man living royally at the public trough! And many of the common citizens of Venice echoed these sentiments. Finally the alchemist’s enemies demanded he produce a proof of his skills: a substantial amount of gold, and soon.

Sometimes mark to market is indeed mark to fantasy.

Finding new suckers

When an asset manager fails to deliver with one target fundraising channel, they look to others. There is nothing wrong with expanding and diversifying a business. But I get suspicious when a fund manager suddenly shifts their whole targeted capital base. Especially when they shift from institutional to retail. Like certain modern fund managers, Il Bragadino focused on finding new clients when became increasingly suspicious of his unfulfilled promises.

Lofty, apparently devoted to his art, Bragadino responded that Venice, in its impatience, had betrayed him, and would therefore lose his services. He left town, going first to nearby Padua, then, in 1590, to Munich, at the invitation of the Duke of Bavaria, who, like the entire city of Venice, had known great wealth but had fallen into bankruptcy through his own profligacy, and hoped to regain his fortune through the famous alchemist’s services. And so Bragadino resumed the comfortable arrangement he had known in Venice, and the same pattern repeated itself.

Believe in the smart people

Yet fund managers, even bad ones, often get incredibly rich in spite of not adding much value to their investors. Their talent is in exploiting human psychology, not investing. It all links back to their ability to exploit people’s need to believe:

His obvious wealth confirmed his reputation as an alchemist, so that patrons like the Duke of Mantua gave him money, which allowed him to live in wealth, which reinforced his reputation as an alchemist, and so on. Only once this reputation was established, and dukes and senators were fighting over him, did he resort to the trifling necessity of a demonstration. By then, however, people were easy to deceive: They wanted to believe. The Venetian senators who watched him multiply gold wanted to believe so badly that they failed to notice the glass pipe up his sleeve, from which he slipped gold dust into his pinches of minerals. Brilliant and capricious, he was the alchemist of their fantasies — and once he had created an aura like this, no one noticed his simple deceptions.

Psychology of Avoiding Charlatans

There is a paradox here. In most cases, it is better to make investments with the intention of making money over decades, not quarters. Yet that is not a reason to not monitor progress. There are many great alternative asset managers who deliver massive value to their clients over decades. I know from experience that they are usually straight shooters.

Charlatans exploit default tendencies in human psychology. Therefore we must guard against this. Building wealth requires discipline. There is no magic investment that will solve everything. People don’t want to hear that, and the Bragadinos of the world prey on this by giving easy answers. Its critical to get comfortable with being uncomfortable. The market doesn’t owe anyone a good return. We must monitor our own psychology as much as the activity of our fund managers.

Constant vigilance is needed to avoid getting tricked by the Bragadinos of the investment world.

Why its wise to think in bets

The secret is to make peace with walking around in a world where we recognize that we are not sure and that’s okay. As we learn more about how our brains operate, we recognize that we don’t perceive the world objectively. But our goal should be to try.

Annie duke’s “Thinking in Bets” is basically long essay with an extremely valuable message. Under a plethora of entertaining anecdotes about professional poker it contains a valuable framework for making decisions in this uncertain world. This requires accepting uncertainty, and being intellectually honest. Good decision making habits compound over time

Thinking in Bets is a slightly less nerdy and less nuanced compliment to pair with “Fortune’s Formula”. It also fits in well with some of the more important behavioral finance books, such as…. Misbehaving, and Hour Between wolf and dog, Kluge, etc.

I’ve organized some of my highlights and notes from Thinking in Bets below.

The implications of treating decisions as bets made it possible for me to find learning opportunities in uncertain environments. Treating decisions as bets, I discovered, helped me avoid common decision traps, learn from results in a more rational way, and keep emotions out of the process as much as possible.

Outcome quality vs decision quality

We can get better at separating outcome quality from decision quality, discover the power of saying, “I’m not sure,” learn strategies to map out the future, become less reactive decision-makers, build and sustain pods of fellow truthseekers to improve our decision process, and recruit our past and future selves to make fewer emotional decisions. I didn’t become an always-rational, emotion-free decision-maker from thinking in bets. I still made (and make) plenty of mistakes. Mistakes, emotions, losing—those things are all inevitable because we are human. The approach of thinking in bets moved me toward objectivity, accuracy, and open-mindedness. That movement compounds over time

Thinking in bets starts with recognizing that there are exactly two things that determine how our lives turn out: the quality of our decisions and luck. Learning to recognize the difference between the two is what thinking in bets is all about.

Why are we so bad at separating luck and skill? Why are we so uncomfortable knowing that results can be beyond our control? Why do we create such a strong connection between results and the quality of the decisions preceding them? How

Certainty is an illusion

Trying to force certainty onto an uncertain world is a recipe for poor decision making. To improve decision making, learn to accept uncertainty. You can always revise beliefs.

Seeking certainty helped keep us alive all this time, but it can wreak havoc on our decisions in an uncertain world. When we work backward from results to figure out why those things happened, we are susceptible to a variety of cognitive traps, like assuming causation when there is only a correlation, or cherry-picking data to confirm the narrative we prefer. We will pound a lot of square pegs into round holes to maintain the illusion of a tight relationship between our outcomes and our decisions.

There are many reasons why wrapping our arms around uncertainty and giving it a big hug will help us become better decision-makers. Here are two of them. First, “I’m not sure” is simply a more accurate representation of the world. Second, and related, when we accept that we can’t be sure, we are less likely to fall

Our lives are too short to collect enough data from our own experience to make it easy to dig down into decision quality from the small set of results we experience.

Incorporating uncertainty into the way we think about our beliefs comes with many benefits. By expressing our level of confidence in what we believe, we are shifting our approach to how we view the world. Acknowledging uncertainty is the first step in measuring and narrowing it. Incorporating uncertainty in the way we think about what we believe creates open-mindedness, moving us closer to a more objective stance toward information that disagrees with us. We are less likely to succumb to motivated reasoning since it feels better to make small adjustments in degrees of certainty instead of having to grossly downgrade from “right” to “wrong.” When confronted with new evidence, it is a very different narrative to say, “I was 58% but now I’m 46%.” That doesn’t feel nearly as bad as “I thought I was right but now I’m wrong.” Our narrative of being a knowledgeable, educated, intelligent person who holds quality opinions isn’t compromised when we use new information to calibrate our beliefs, compared with having to make a full-on reversal. This shifts us away from treating information that disagrees with us as a threat, as something we have to defend against, making us better able to truthseek. When we work toward belief calibration, we become less judgmental .

In an uncertain world, the key to improving is to revise, revise, revise.

Not much is ever certain. Samuel Arbesman’s The Half-Life of Facts is a great read about how practically every fact we’ve ever known has been subject to revision or reversal. We are in a perpetual state of learning, and that can make any prior fact obsolete. One of many examples he provides is about the extinction of the coelacanth, a fish from the Late Cretaceous period. A mass-extinction event (such as a large meteor striking the Earth, a series of volcanic eruptions, or a permanent climate shift) ended the Cretaceous period. That was the end of dinosaurs, coelacanths, and a lot of other species. In the late 1930s and independently in the mid-1950s, however, coelacanths were found alive and well. A species becoming “unextinct” is pretty common. Arbesman cites the work of a pair of biologists at the University of Queensland who made a list of all 187 species of mammals declared extinct in the last five hundred years.

Getting comfortable with this realignment, and all the good things that follow, starts with recognizing that you’ve been betting all along.

The danger of being too smart

The popular wisdom is that the smarter you are, the less susceptible you are to fake news or disinformation. After all, smart people are more likely to analyze and effectively evaluate where information is coming from, right? Part of being “smart” is being good at processing information, parsing the quality of an argument and the credibility of the source. So, intuitively, it feels like smart people should have the ability to spot motivated reasoning coming and should have more intellectual resources to fight it. Surprisingly, being smart can actually make bias worse. Let me give you a different intuitive frame: the smarter you are, the better you are at constructing a narrative .

… the more numerate people (whether pro- or anti-gun) made more mistakes interpreting the data on the emotionally charged topic than the less numerate subjects sharing those same beliefs. “This pattern of polarization . . . does not abate among high-Numeracy subjects.

It turns out the better you are with numbers, the better you are at spinning those numbers to conform to and support your beliefs. Unfortunately, this is just the way evolution built us. We are wired to protect our beliefs even when our goal is to truthseek. This is one of those instances where being smart and aware of our capacity for irrationality alone doesn’t help us refrain from biased reasoning. As with visual illusions, we can’t make our minds work differently than they do no matter how smart we are. Just as we can’t unsee an illusion, intellect or willpower alone can’t make us resist motivated reasoning.

The Learning Loop

Thinking rationally is a lot about revising, and refuting beliefs(link to reflexivity) By going through a learning loop faster we are able to get an advantage. This is similar to John Boyd’s concept of an OODA loop.

We have the opportunity to learn from the way the future unfolds to improve our beliefs and decisions going forward. The more evidence we get from experience, the less uncertainty we have about our beliefs and choices. Actively using outcomes to examine our beliefs and bets closes the feedback loop, reducing uncertainty. This is the heavy lifting of how we learn.

Chalk up an outcome to skill, and we take credit for the result. Chalk up an outcome to luck, and it wasn’t in our control. For any outcome, we are faced with this initial sorting decision. That decision is a bet on whether the outcome belongs in the “luck” bucket or the “skill” bucket. This is where Nick the Greek went wrong. We can update the learning loop to represent this like so: Think about this like we are an outfielder catching a fly ball with runners on base. Fielders have to make in-the-moment game decisions about where to throw the ball.

Key message: How poker players adjust their play from experience determines how much they succeed. This applies ot any competitive endeavor in an uncertain world.

Intellectual Honesty

The best players analyze their performance with extreme intellectual honesty. This means if they win, they may end up being more focused on erros they made, as told in this anecdote:

In 2004, my brother provided televised final-table commentary for a tournament in which Phil Ivey smoked a star-studded final table. After his win, the two of them went to a restaurant for dinner, during which Ivey deconstructed every potential playing error he thought he might have made on the way to victory, asking my brother’s opinion about each strategic decision. A more run-of-the-mill player might have spent the time talking about how great they played, relishing the victory. Not Ivey. For him, the opportunity to learn from his mistakes was much more important than treating that dinner as a self-satisfying celebration. He earned a half-million dollars and won a lengthy poker tournament over world-class competition, but all he wanted to do was discuss with a fellow pro where he might have made better decisions. I heard an identical story secondhand about Ivey at another otherwise celebratory dinner following one of his now ten World Series of Poker victories. Again, from what I understand, he spent the evening discussing in intricate detail with some other pros the points in hands where he could have made better decisions. Phil Ivey, clearly, has different habits than most poker players—and most people in any endeavor—in how he fields his outcomes. Habits operate in a neurological loop consisting of three parts: the cue, the routine, and the reward. A habit could involve eating cookies: the cue might be hunger, the routine going to the pantry and grabbing a cookie, and the reward a sugar high. Or, in poker, the cue might be winning a hand, the routine taking credit for it, the reward a boost to our ego. Charles Duhigg, in The Power of Habit, offers the golden rule of habit change….

Being in an environment where the challenge of a bet is always looming works to reduce motivated reasoning. Such an environment changes the frame through which we view disconfirming information, reinforcing the frame change that our truthseeking group rewards. Evidence that might contradict a belief we hold is no longer viewed through as hurtful a frame. Rather, it is viewed as helpful because it can improve our chances of making a better bet. And winning a bet triggers a reinforcing positive update.

Note: Intellectual Honesty thinking clearly= thinking in bets

Good decisions compound

One useful model is to view everything as one big long poker game. Therefore the result of individual games won’t upset you so much. Furthermore, good decision making habits compound over time. So the key is to always be developing good long term habits, even as you deal with the challenges of a specific game.

The best poker players develop practical ways to incorporate their long-term strategic goals into their in-the-moment decisions. The rest of this chapter is devoted to many of these strategies designed to recruit past- and future-us to help with all the execution decisions we have to make to reach our long-term goals. As with all the strategies in this book, we must recognize that no strategy can turn us into perfectly rational actors. In addition, we can make the best possible decisions and still not get the result we want. Improving decision quality is about increasing our chances of good outcomes, not guaranteeing them. Even when that effort makes a small difference—more rational thinking and fewer emotional decisions, translated into an increased probability of better outcomes—it can have a significant impact on how our lives turn out. Good results compound. Good processes become habits, and make possible future calibration and improvement.

At the very beginning of my poker career, I heard an aphorism from some of the legends of the profession: “It’s all just one long poker game.” That aphorism is a reminder to take the long view, especially when something big happened in the last half hour, or the previous hand—or when we get a flat tire. Once we learn specific ways to recruit past and future versions of us to remind ourselves of this, we can keep the most recent upticks and downticks in their proper perspective. When we take the long view, we’re going to think in a more rational way.

Life, like poker, is one long game, and there are going to be a lot of losses, even after making the best possible bets. We are going to do better, and be happier, if we start by recognizing that we’ll never be sure of the future. That changes our task from trying to be right every time, an impossible job, to navigating our way through the uncertainty by calibrating our beliefs to move toward, little by little, a more accurate and objective representation of the world. With strategic foresight and perspective, that’s manageable work. If we keep learning and calibrating, we might even get good at it.

Carl Icahn: Capitalist Kingpin

Carl Icahn is one of my favorite capitalists. For all his flaws, his glory days were epic. He shook up the corporate aristocracy, and created massive value for his early financial backers. The economy has benefited from the disruption of complacency led by corporate raiders like Icahn.

Carl Icahn’s bio covers the evolution of his takeover style and thought process. It pairs well with Tobias Carlisle’s work, including The Acquirer’s Multiple, and Deep Value.

Below are some of my notes from Icahn’s bio:

The importance of philosophy

Icahn studied philosophy in college. This proved useful in understanding markets and navigating high stakes situations. He focused on the concept of empiricism.

Empiricism says knowledge is based on observation and experience, not feelings,” Icahn said. “In a funny way, studying twentieth-century philosophy trains your mind for takeovers. “. . There’s a strategy behind everything. Everything fits. Thinking this way taught me to compete in many things, not only takeovers but chess and arbitrage.

….It seems to me that the quest for an explication of the empiricist meaning criterion, as it has progressed, may be likened to the tale of the city that suddenly finds itself in possession of a great homogeneous mixture of gold and sand. If the gold could be separated from the sand it would prove a great deal more valuable to the inhabitants. The wise men of the city diligently search for a method of separation. By so doing they not only vastly increase their insight into the nature of gold, sand, homogeneous mixtures, etc., but also produce a series of increasingly potent methods of separating the chaff from the gold, the meaningless from the significant.”

Waiting for the right opportunity to pounce

He waits until someone is so stretched out and in need of a deal that he can come in and buy under the most favorable terms.

From the PPM/pitchbook for Icahn’s first fund:

It is our opinion that the elements in today’s economic environment have combined in a unique way to create large profit-making opportunities with relatively little risk. Our nation’s huge need for energy has resulted in a massive flow of dollars abroad. This, coupled with huge deficit spending and decreasing productivity, has caused a high inflation rate and a sharply declining dollar. As a result, the value of gold and goods in general has skyrocketed. An obvious corollary to this is that the real or liquidating value of many American companies has increased markedly in the last few years; however, interestingly, this has not at all been reflected in the market value of their common stocks. Thus we are faced with a unique set of circumstances that, if dealt with correctly, can lead to large profits…

Non linear thinking

Like most great investors, Icahn is a non-linear thinker.

In part, his success is based on an intellectual skill that enables him to plot dozens of moves in advance. While his adversaries are thinking in linear fashion—”If I can get from A to B, then I’ll proceed to C”—Icahn sees dozens of possibilities on a single screen. The mental agility that enables him to zigzag from C to F to Z and back to R, leaves his opponents so thoroughly confused and frustrated they are on the verge of shorting out. “In trying to beat Carl, and failing to do so, people come away baffled,” said Brain Freeman. “But I can tell them why they fail. Because they think they know what Carl’s goal is when in fact he has no fixed goal.

Expanding options

Presented with an ultimatum in which he is told to choose between evil A or lesser evil B, Icahn moves into intellectual overdrive, expanding the range of options. In this way, he turns the tables on his adversaries, who find themselves facing a more ominous threat than they hurled at the raider.

Limitations of Icahn’s approach

Icahn was a great liquidator, a great investor in asset intensive businesses, but sticking too closely to his methods would cause a modern investor to miss great opportunities to invest in rapidly growing businesses. Additionally, based on the performance of IEP, its possible that he has failed to adapt to recent technological disruption, and the age of asset lite businesses.

Carl is a smart Neanderthal,” said Marty Whitman. “He’s a Neanderthal because he doesn’t listen. He has fixed ideas. He doesn’t see that you can’t make money by investing in a business. He only wants to cash out—to get cash flow. He doesn’t understand that most of the great businesses built in this country were cash consumers. They used public markets and consumed cash to build fabulous wealth for their owners. But Carl just wants the cash-out approach.

As with most corporate titans, sometimes his ego gets the best of him. He nearly went bankrupt messing around with airlines, for example. Nonetheless his story is valuable and entertaining, and he wrote the playbook for many situations faced by investors today.

See also:

The Next Level of Shareholder Activism

Beyond headline numbers

Everybody has access to Bloomberg and Google. Every global macro investor closely follows macro data out of every country. To gain an an edge, one must look beyond headline numbers, and find underutilized datasets.

This applies when finding countries, industries, and individual companies in which to invest. Any time you want to combine top down and bottom up insights, you need to get creative with finding the right data.

Schumpeter and Perez

Joseph Schumpeter pointed out that aggregate figures “conceal more than they reveal”.

Relations between aggregates are

“entirely inadequate to teach us anything about the nature of the processes which shape their variations, aggregative theories of the business cycle must be inadequate too…”

In Technological Revolutions and Financial Capital, ( Carlota Perez emphasizes that new technological paradigms can only be analyzed by looking closely at inner workings of an economy. Within the same country, or industry some subsectors will grow at astonishingly high rates, while others decline. Perez’s framework is valuable to analyzing times of great technological change, which is basically anytime. Examples she uses include the first British Industrial Revolution( the age of Steam and Railways, the Age of steel, electricity, and heavy engineering, age of oil, automobile and mass production.

Top line numbers such as GDP or earnings could deceive an analyst, especially when looking at a new market.

Valuation and pricing

“People living through the period of paradigm transition experience real uncertainty as to the ‘right’ price of things(including that of stocks, of course).”

Extreme jumps in productivity change relative price structures in the economy. “The change in relative price structure is radical and centrifugal. Money buying electronics and telecommunications today does not have the same value as money buying furniture or automobiles.” Therefore, looking at inflation or deflation in aggregate is deceptive. Many years after Perez’ book, this now exacerbated by the Amazon effect. To some effect this may impact valuation in some industries.

Research methods

Long term aggregate data, spanning multiple periods of technological change are senseless. This goes for GDP, corporate earnings etc. Yet disaggregated stats are rarely available(except during more stable phases), as Perez points out.

The internet has provided more opportunities to find disaggregated, unique, underutilized datasets. Often this means poking around on weird regulatory websites, and following up on footnotes to academic papers.

This process might be about to get a lot easier.

Google launched a new dataset search engine. I’m excited to see how its impact snowballs as more datasets are added. Although intended for journalists, it is likely to be a valuable tool for investors seeking differentiated alpha.

Of course that means today’s edge, will be tomorrow’s table stakes.

See also: The hard thing about finding easy things

The future of non-traded REITs

“All under heaven is in utter chaos. The situation is excellent.”

Mao Zedong (1)

Non-traded REITs, in most incarnations, have been reprehensible financial products sold by the unscrupulous to the naive. Nevertheless, they persisted. The 7% commission was just irresistible to brokers while it lasted.

Now the mess of legacy products is left for vulture investors to cleanup. Technologically advanced secondary markets will make the process a little smoother than last time. While the traditional group of Sponsors and brokers struggle to raise capital, institutional players such as Blackstone and Oaktree are launching new non-traded REITs, and finding no shortage of demand. The next generation of non-traded REITs are a major improvement over the previous generation,although the bar isn’t exactly that high.

New entrants distributing newly improved product to new distribution channels will define the future of non-traded REITs. Several large “brand name” asset managers have recently launched non-traded REITs. They are selling via wirehouses, which have generally avoided non-traded REITs for over 20 years. They’re also selling via registered investment advisers, who, as fiduciaries, previously avoided non-traded REITs. Furthermore several well known real estate firms are launching non-traded REITs or other products and selling directly to investors online, a phenomenon completely unheard of a decade ago.

Legacy non-traded REITs and secondary market

There is a massive overhang of legacy product that is preventing sales of new non-traded REITs via the independent broker dealer(IBD) channel. Post financial crisis, non-traded REIT Sponsors tried to take non-traded REITs full cycle(either via merger or IPO) after 2-4 years. This allowed financial advisers to collect the 7% commissions over and over again. Constant recycling became a critical source of income for IBDs, and an absolute bonanza for Sponsors However, after the AR Global scandal, fiduciary standard, and FINRA 15-02, the pace of new product slowed down suddenly.